EPF vs PPF: Meaning, Differences, Returns & Which Is Better In 2026

In India, when people hear long-term safety nets, EPF vs PPF are the two things that come to their minds. Both these government saving schemes are highly sought after for both salaried and non-salaried workers.

Employees' Provident Fund (EPF) is a mandatory retirement savings scheme for formal sector workers. Alternatively, a PPF account (Public Provident Fund) is the best option for anyone, including freelancers, self-employed professionals, or homemakers, to start saving for their retirement using a government scheme.

Both EPF and PPF are popular because of the features like tax benefits, principal protection, and guaranteed returns. Many Indians depend largely on such fixed-income instruments compared to riskier equity-linked investments for retirement savings.

When the equity markets are volatile, the value of the fixed-income securities has grown. These investors seek stability instead of volatile, high returns. Fixed income provides stable returns, reduced volatility, and capital preservation.

So, EPF vs PPF, which one is better? Keep reading to find out which is more suitable for your financial goals.

What Is EPF (Employees' Provident Fund)?

EPF, which stands for the Employees' Provident Fund, is an obligatory retirement-backed savings program. It applies to salaried employees in organisations with 20 or more employees under the EPF Act.

- Staff with a basic salary plus dearness allowance (DA) not exceeding INR 15,000 per month are covered automatically.

- In case your basic + DA is more than INR 15,000, it is an optional contribution. You can join voluntarily, provided that you and your employer mutually agree and apply an option under Para 26(6) within a period of six months from the date of joining.

Participation starts from the day you join work. You and your employer each deposit 12% of your basic + DA in your EPF account. This accumulates your retirement corpus over the years, making it the most dependable long-term investment in India available for employees in the formal sector.

What Is PPF (Public Provident Fund)?

The Public Provident Fund, also known as PPF, is a voluntary government plan available to everyone. A PPF account can be opened by any Indian resident.

PPF accounts are also available for minors, as long as the parent or lawful guardian runs the account in the name of the minor.

HUFs and joint accounts are excluded.

Non-residents are not allowed to open new PPF accounts. But anyone who has opened one while being a resident may continue to operate it till maturity and cannot extend it beyond the initial period of 15 years.

PPF schemes are governed by the Public Provident Fund Act, 1968. You can open a PPF account through post offices or banks. PPF accounts have a lock-in period of 15 years, after which they can be extended in 5-year blocks. PPF allows investments from INR 500 to INR 1.5 lakh in a financial year. Investments can be made either as a lump sum or in up to 12 instalments, within the set limits1.

Recommended Reading: Step-by-Step Guide of EPF Withdrawal Online

Key Differences: EPF Vs PPF

Some of the main differences between EPF and PPF are:

| Feature | EPF (Employees' Provident Fund) | PPF (Public Provident Fund) |

| Type of Scheme | Mandatory for salaried employees under the EPF Act | Voluntary scheme open to all resident Indians |

| Eligibility | Salaried individuals in establishments with ? 20 employees | All Indian citizens, minors via guardians, (NRIs cannot open new accounts, but can maintain existing ones opened when they were in India |

| Contribution | 12% of basic salary + DA, contributed by both employee and employer | Minimum INR 500, maximum INR 1.5 lakh per year; only by the account holder (or guardian) |

| Interest Rate (2025) | Approx 8.25% p.a. for FY 2024-25 | Around 7.1% p.a., revised quarterly |

| Interest Revision Frequency | Annual declaration by EPFO | Quarterly, by the Ministry of Finance |

| Lock-in & Withdrawal | Withdrawable at retirement (typically age 58) or under specified conditions like unemployment, housing, medical; taxable if < 5 years | Lock-in for 15 years; partial withdrawals allowed after 7 years; premature closure in special cases |

| Tax Treatment (Section 80C & EEE) | Contributions (up to INR 1.5 lakh per annum) are deductible under Section 80C. If service ? 5 years, maturity including interest is tax-free. Withdrawals before 5 years are taxable

| Fully under EEE: contributions (up to INR 1.5 lakh), interest, and maturity amount are all tax-exempt

|

| Employer Contribution | Yes, matched by the employer | No employer contribution |

| Management | Managed by EPFO (a statutory body) | Administered by the government via authorised banks & post offices |

EPF vs PPF: Returns, Liquidity, Safety

Both schemes vary in terms of returns, liquidity, and safety.

1. Returns

EPF and PPF schemes provide fixed returns depending on the interest rates fixed by the government. EPF schemes usually have a higher interest rate, but can be opened only by salaried employees.

2. Liquidity

EPF provides liquidity at reasonable terms under certain conditions. You can withdraw a portion of the corpus for housing, medical expenses, or unemployment (up to 75% for one month and 100% for 2 months of unemployment).

Complete withdrawal upon retirement (after 58 years) is allowed. A portion of the EPS corpus will be reserved to be paid as pension, and this pension is taxable. However, withdrawals are taxable if you withdraw within 5 years of account opening.2

PPF, on the other hand, has a longer lock-in period: 15 years. Partial withdrawals are permitted only after the 5th year (or 7th year in some banks), and only up to 50% of the previous year's balance can be withdrawn.

PPF withdrawals are not taxable. At the end of 15 years, you can withdraw the entire amount or extend it in 5-year blocks. During the extension period, you can optionally make contributions.

3. Safety

Government statutory backing offers safety for both EPF and PPF investments. EPF offers higher returns, but with equity exposure, which comes with certain risks.

15% of the fresh money collected by the EPF statutory body EPFO is invested in equities to earn better returns. The remaining funds are invested in government bonds.

Also Read: List of Tax Saving Investment Options

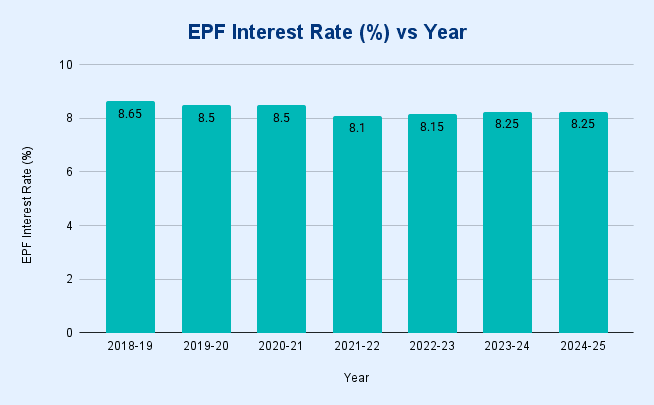

Historical Returns Trend of EPF and PPF

The EPF interest rate has seen minor fluctuations over the years, staying largely above 8% and ensuring stable returns for salaried employees. This consistency makes EPF a reliable long-term savings option backed by government security.

EPF Interest Rate (Recent Years)

| Financial Year | EPF Interest Rate (%) |

| 2018-19 | 8.65 |

| 2019-20 | 8.5 |

| 2020-21 | 8.5 |

| 2021-22 | 8.1 |

| 2022-23 | 8.15 |

| 2023-24 | 8.25 |

| 2024-25 | 8.25 |

Source: EPF India3

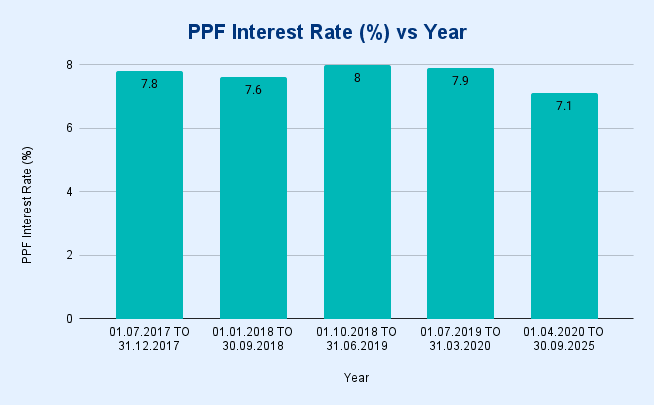

PPF Interest Rate (Recent Years)

The PPF interest rate has varied slightly in recent years, typically ranging between 7% and 8%. Its government backing and tax benefits make it a safe and dependable choice for long-term savers.

| Financial Year | PPF Interest Rate (%) |

| 2012-13 | 8.8 |

| 2013-16 | 8.7 |

| 2016-17 | 8.1-8.0 |

| 2017-18 | 7.80 – 7.90 |

| 2018-19 | 7.60 -8.00 |

| 2020-21 to 2024-25 | 7.1 |

Source : NSI India4

Also Read: What Are VPF Tax Benefits?

EPF vs PPF: Which One To Choose?

Depending on your preference, you can choose to invest in EPF, PPF, or both.

Salaried Employees Vs. Self-Employed

If you are a salaried employee in a company where EPF is mandatory (with over 20 employees), then EPF provides automatic retirement savings. Your employer matches your contribution, which may give a significant boost to your corpus. Hence, EPF can be a strong foundation for retirement savings in India, offering good liquidity and higher interest rates than most fixed-income options.

The self-employed professional, freelancer, artisan, or entrepreneur is not entitled to EPF benefits. PPF fits your needs. The Public Provident Fund is a government-backed savings scheme for Indian residents, offering fixed, tax-free returns and granting you a systematic way to build a retirement corpus.

Even if salaried, mixing EPF and PPF may make sense. You maintain that automatic input from your employer and include voluntary savings. You can also open a PPF account to diversify and strengthen your long-term plan.

Role Of Diversification

Diversification balances safety, liquidity, and returns. The functioning of EPF and PPF is similar: both are safe and guarantee returns backed by the Government.

But there are dissatisfactions with both. The EPF does not suit those who don't work in the formal sector; the PPF takes locks in your money for 15 long years with uncomfortable withdrawal conditions.

Adding the following would be a good addition to your retirement plan in addition to EPF and PPF:

1. Government bonds/tax-free bonds/SDIs (Systematic Deposit Investments): These can give a higher effective yield with moderate risk. They can also enhance liquidity and returns while offering fixed-income safety.

2. NPS (National Pension System): This is a market-linked instrument with a portion in equity, which may give better returns in the long run, at moderate risk. This option is particularly useful if you are younger and have a high-risk appetite.

Also Read: What Is City Compensatory Allowance: Are You Eligible?

Conclusion

Both EPF and PPF are among the most reliable government-backed savings schemes in India, offering safety, guaranteed returns, and tax benefits. EPF is ideal for salaried employees, as it comes with employer contributions and higher average interest rates, while PPF provides universal access to all residents with complete flexibility and tax-free maturity.

For most investors, combining EPF and PPF can strike the right balance between stability, discipline, and diversification. However, for those seeking higher returns, enhanced liquidity, and more flexible fixed-income opportunities, exploring alternatives such as government bonds, SDIs, or the National Pension System (NPS) is worthwhile.

Along with EPF and PPF, investors can explore modern fixed-income platforms such as Grip Invest, which offer regulated, transparent, and accessible opportunities starting from INR 1,000

FAQs On EPF vs PPF

1. Which is safer: EPF or PPF?

Both are safe since both are backed by the Government of India. The EPF has limited exposure to equity (about 15% of the new deposits) and entails a little bit of market risk. PPF offers fully guaranteed interest.

2. Can I invest in both EPF and PPF?

Yes, you can invest in both EPF and PPF. You are automatically subscribed to EPF if you are a salaried employee. Besides, you can have a PPF account to add to your retirement corpus and claim additional tax benefits.

3. What is the lock-in period of PPF?

PPF lock-in period is 15 years. After that, the entire amount can be withdrawn. You can also extend in blocks of 5 years. Partial withdrawals, subject to conditions, are available from year 7.

4. Does EPF give better returns than PPF?

Generally, yes; EPF has given higher returns in recent times compared to PPF. For the FY 2024-25, EPF return is approximately 8.25%, while PPF is at 7.1%. Remember that EPF's better return is with a little bit of equity exposure, which makes it more volatile than PPF. PPF returns are guaranteed and fixed.

References:

1. Axis Bank, accessed from: https://www.axisbank.com/progress-with-us-articles/investment/ppf-nps/difference-between-ppf-and-epf

2. Paisa Bazar, accessed from: https://www.paisabazaar.com/saving-schemes/difference-between-epf-and-ppf/

3. EPF India, accessed from: https://www.epfindia.gov.in/site_docs/PDFs/EPFO_PRESS_RELEASES/Interest_Rate_Press_Release_10-02-2024%20.pdf

4. NSI India, accessed from: https://www.nsiindia.gov.in/(S(pjkwzeftocyrnq45p3zz1155))/InternalPage.aspx?Id_Pk=178

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001