Loss Aversion In Investing In India: Why The Fear Of Loss Holds Investors Back

The fear of risk did not just make us trade our passion for a secure 9-to-5; it continues to quietly stop us from building real wealth. Like a monster under the bed, the fear of “what if” makes a loss of INR 10,000 more painful than the joy of gaining INR 10,000.

Thanks to the fear of loss investing, safe investments like traditional FDs feel emotionally comforting, even when they quietly lose to inflation. If you think it is just bad maths, you might be wrong.

Therefore, as our guitars or paint brushes collect dust because they were “too risky” for a career, let us decode how Loss Aversion in Investing India stops us from choosing assets for sustained growth.

What Is Loss Aversion In Investing In India

Investors often act like DDLJ gone wrong, a parallel universe where Babuji never said Ja Simran Ja because the fear of losing what we already have is more than a prospect of something better.

This is Loss Aversion in action. Let me explain.

- Meaning of Loss Aversion: Investor Psychology India

According to Behavioural Finance India, loss aversion in investing refers to a psychological phenomenon where the pain of losing money feels more intense than the happiness of gaining the same amount of money.

For instance, Mr A lost INR 15,000 in a equity market dip, but he gained INR 15,000 from debt funds. According to loss aversion, the emotional impact of the loss will be more than the happiness of the gain.

However, this is not us being melodramatic; loss aversion stems from actual evolutionary reasons.

- Loss vs Gain Psychology: Why Loss Feels More Intense?

During the course of evolution, our ancestors prioritised avoiding threats over getting rewards. It was a simple survival instinct in a scarce environment. This genetic trait is passed down from early humans to modern men.

Even today, brain imaging shows how losses activate pain centres of the brain, like the amygdala, more intensely1. Therefore, the pain of loss feels more intense than happiness caused by the gain of the same amount, i.e. loss aversion. However, while this was useful when people hunted for food, in the era of Blinkit and Zomato, this makes little sense.

Loss aversion becomes an acute problem in investing. A primary study in India revealed how 33.3% of the sample investors prefer to reduce their equity holdings after a loss2. Loss aversion is more typical of Indian investors due to the safe investment mindset.

Let us now decode why investors avoid risk, especially in India.

Risk Aversion Indian Investors: How Loss Aversion Shows Up In Indian Portfolios

Indian investors often run away from growth assets faster than your latest interest ghosting you. This shows up in several key investment trends. Some of them are discussed below.

- Too Committed to Fixed-Income Investments: While portfolio security is important to maintain a strong foundation on which growth can be earned, their excess presence can reduce prospective returns. Indian investors often over-commit to assets like traditional FDs.

- Treating Markets Like a Red Flag: Every investment has a degree of risk. However, rather than diversifying assets, some investors tend to cut off market exposure altogether.

- Savings are Not Equal to Investment: Investors often miss that unless savings are invested into assets that beat inflation, they cannot be considered an investment. The purchasing power of INR 100 in 10 years would be less than what it is today. Therefore, setting aside money for the future is not enough; investing it to maintain its real value is key.

- Emotional Investing India: We all have that one uncle who suggests FDs for everyone, all the time, irrespective of your income, goals, risk capacity, etc. Rather than data-driven financial planning, investors choose assets based on how good they feel about them. Thus, psychological and other biases heavily influence decision-making.

These attitudes stem from the fact that Indians would choose a safe loss over a risky gain due to their loss aversion.

“Safe” Losses Vs “Risky” Gains

There lies a world of difference between risk and calculated risk. Often in a bid to avoid risk, investors end up creating an affinity towards safe losses, resulting in a lack of growth. Absence of calculated risk to optimise gain creates more damage than good over time.

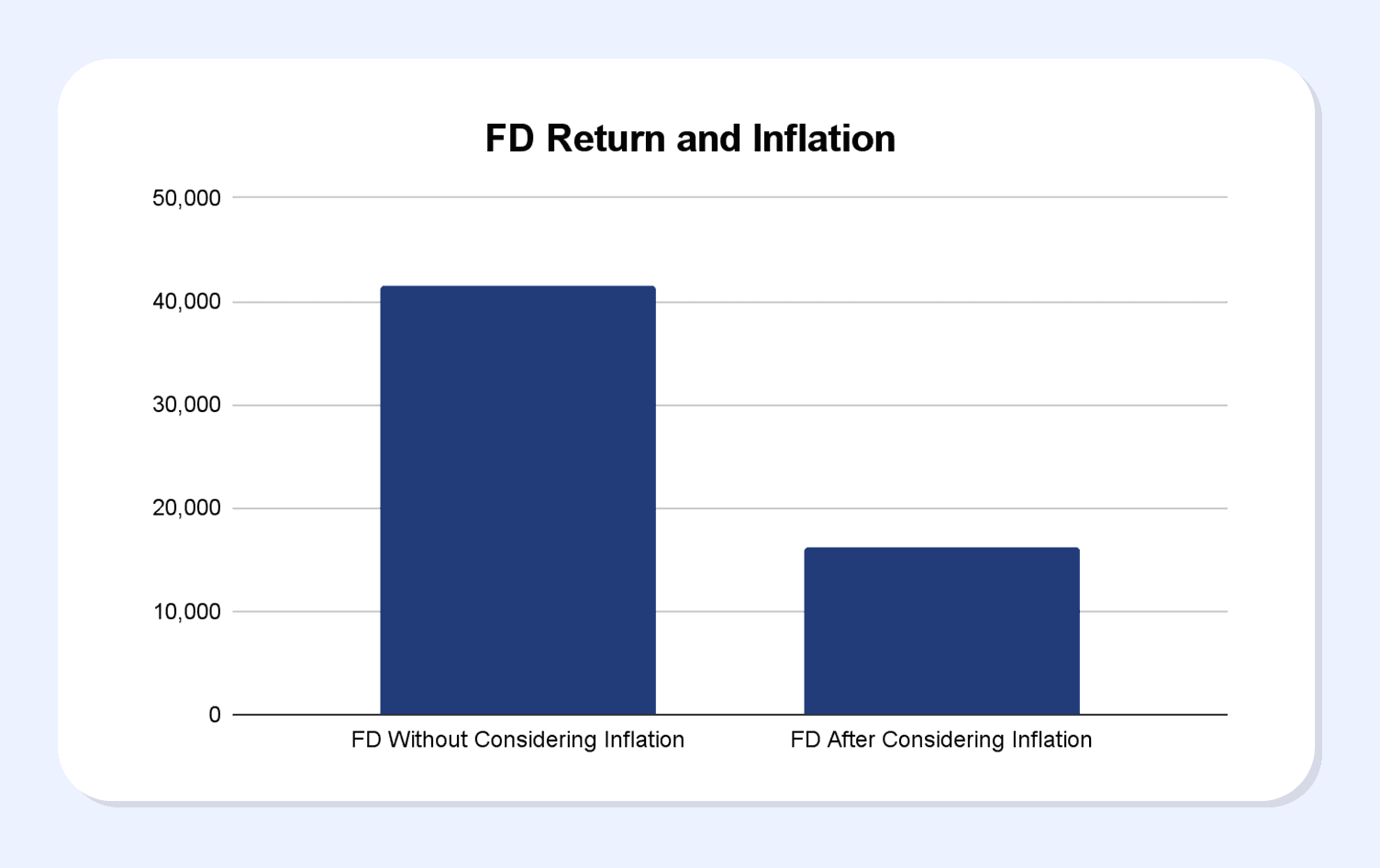

Imagine this. Mr K invests INR 1,00,000 in a traditional FD that gives about 7% returns. After 5 years, he gets INR 41,478 as interest. Now, if the rate of inflation is assumed at 4%, then his real interest drops to 3% from 7%, making the return INR 16,118.

Therefore, although Mr K received guaranteed returns from his FD, it was just emotional safety because inflation was the hidden cost that he had to bear for being “too safe”.

However, what could Mr K have done differently? Let us analyse.

Real-Life Scenarios: Loss Aversion At Work

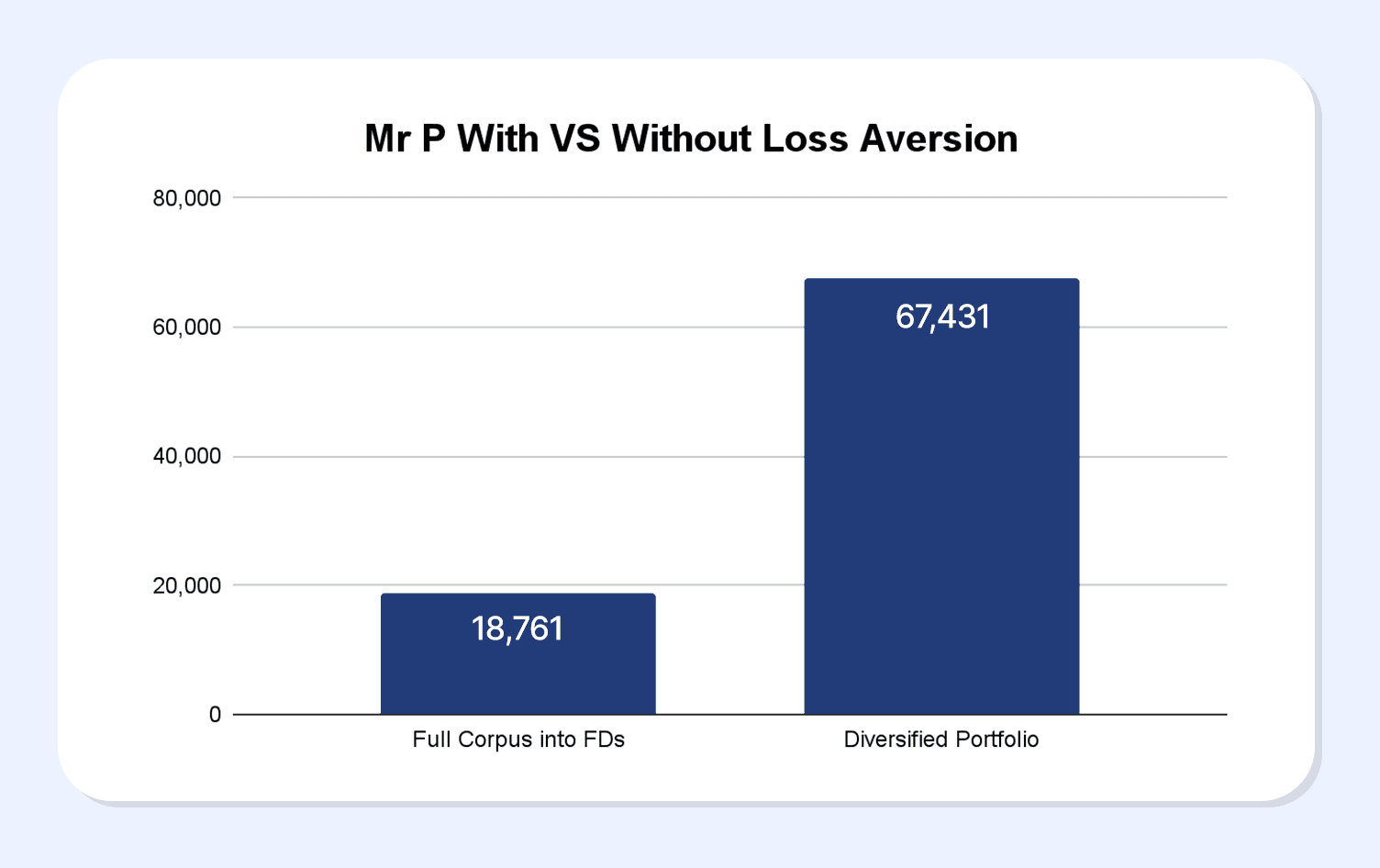

Let us continue with the example of Mr P. Suppose he had a total corpus of INR 2,00,000. Now, let us analyse two scenarios.

- Loss Aversion: Full Corpus into FDs

Due to his loss aversions, Mr P invests the entire corpus into a traditional FD at a 7% interest. After accounting for a 4% inflation, his real return becomes 3%. Therefore, after investing INR 2 lakhs for 3 years, he gets a return of INR 18,761.

Now, what if he planned his investment and diversified across assets to balance risk and return?

- Planned Investing: Diversified Portfolio

Mr P decided to invest 20% into a traditional FD, 30% into High-Yield FDs through Grip and 50% into debt mutual funds. After assuming 4% inflation, the table below shows his returns after 3 years.

| Asset | Principal (INR) | Return (%) | Return after Inflation (%) | Return (INR) |

| Tradition FDs | 40,000 | 7 | 3 | 3,752 |

| High-Yield FDs from Grip | 60,000 | 10 | 6 | 11,737 |

| Debt Mutual Funds | 1,00,000 | 12 | 8 | 51,942 |

| Total | 67,431 | |||

Now, let us visually see the difference between the two scenarios.

Skipping loss aversion does not mean not considering risk at all. Just like in exams, too much stress often makes us forget the answers; loss aversion has to be managed to ensure optimal decision-making.

Bottomline: How Investors Can Manage Loss Aversion

As investors, we must understand the difference between risk and volatility. While volatility is a characteristic of the market, the degree of risk can be controlled through optimal diversification. Just like in the case of Mr P. He did not skip FDs altogether and invest completely in markets; he diversified to balance return and risk. The first step is to set goals and decide your risk tolerance, then diversify across assets that suit you.

Grip offers a range of assets like bonds, high-yield FDs, mutual funds and more, that can offer up to 14% returns.

Visit Grip Invest today!

FAQ’s

1. Is loss aversion always bad for investors?

Not really. Loss aversion becomes a problem only when it stops you from taking calculated risks. Being cautious is healthy; avoiding growth assets completely is what hurts long-term wealth.

2. Why do Indian investors prefer FDs even when returns are low?

Because FDs offer emotional comfort and certainty. For many Indian investors, protecting capital feels more important than beating inflation, even if it means lower real returns over time.

3. How can beginners overcome fear without taking excessive risk?

Start small and diversify. Combining safer instruments like FDs with debt funds or bonds helps investors stay invested while gradually getting comfortable with market-linked returns.

References:

1. Oxford academic, accessed from: https://academic.oup.com/scan/article/15/6/661/5869327?login=false

2. IRJEMS International Research Journal of Economics and Management Studies, accessed from: https://irjems.org/Volume-3-Issue-11/IRJEMS-V3I11P102.pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001