A Complete Guide On How To Start Investing In 2026

Inflation is detrimental to the purchasing power of money. It makes commodities more expensive as the face value of a currency remains constant. Investing in securities and other financial assets through the optimum utilisation of the golden rules of investing allows investors to combat the diminishing effect of inflation.

However, there are several myths when it comes to marketplace investments. Some of the most common among them are:

- Investing is complicated and meant for the rich.

- Investment requires predicting and timing the market.

- Investors know everything and are smarter than most people.

This blog aims to debunk some of these myths while providing the ultimate beginner’s guide to investing. The objective is to aid investors with the only investment guide they need for all their queries.

Understanding Your Financial Goals

An optimal investing strategy does not start with hunting for the right financial tool. It starts with setting the financial goals of the investors. A golden rule of investment states that the right investment medium cannot be chosen without establishing proper financial objectives.

Long-term goals, short-term goals and an emergency fund are the three major aspects of financial goals. This section explores each of them in detail.

Short-Term vs Long-Term Goals

The table below provides a comparative analysis of the two major classifications of financial goals.

| Parameter | Long-Term Goals |

| Definition | Goals set to be achieved after a long period of time, usually spanning several years, are called long-term goals. |

| Timeframe | It is usually set to be achieved after several years. |

| Flexibility | Investors get ample time to adjust their investing strategy to changing market situations. |

| Feedback | It takes several years to receive the benefits of an investment. |

| Examples | Marriage, education and other integral commitments like a house can be categorised as long-term goals. |

Emergency Fund

A fiscal reserve set aside to meet sudden and unplanned expenses culminating in a financial emergency is called an emergency fund.

Emergencies do not come with a warning bell. Therefore, fiscal prudence demands preparedness for sudden and unexpected need for money. A very important golden rule of investment is the importance of setting up an emergency fund.

In the absence of such a fund, if any unforeseen situation occurs, it not only disrupts the short-term and long-term goals but also life in general. The emergency fund is often invested in very secure and highly liquid instruments to meet the unexpected nature of the expense itself.

Allocation of funds among short-term goals, long-term goals, and emergency funds requires optimum budgeting. The next section explains the meaning and process of budgeting in detail.

Basics Of Budgeting

A detailed plan that outlines the optimum allocation of income into expenses and savings, after optimum consideration of financial goals and needs, is called a budget. The process of budget creation is called budgeting.

This section of the guide to investing in India explores the steps to optimum budgeting.

1. Create a detailed breakdown of income and expenses.

2. Establish long-term and short-term financial goals.

3. Derive an approximate value of the emergency fund required. It must be based on the income and necessary expenses.

4. After deducting the expense from the income, investors must derive the amount of savings.

5. Distribute these savings among investment mediums meant to achieve the goals and create the emergency fund.

6. Monitor the performance of the budget created across the five steps periodically.

7. Ensure strict adherence to the budget. Patience and discipline might be the key to success in budgeting.

Also Read: What Is City Compensatory Allowance: Are You Eligible?

Beginner’s Guide To Investing Basics

Before getting into the actual investment strategies and the process of investment, it is essential to clarify certain basic investment concepts. Therefore, let’s understand them in detail because this is the only investment guide a beginner might need.

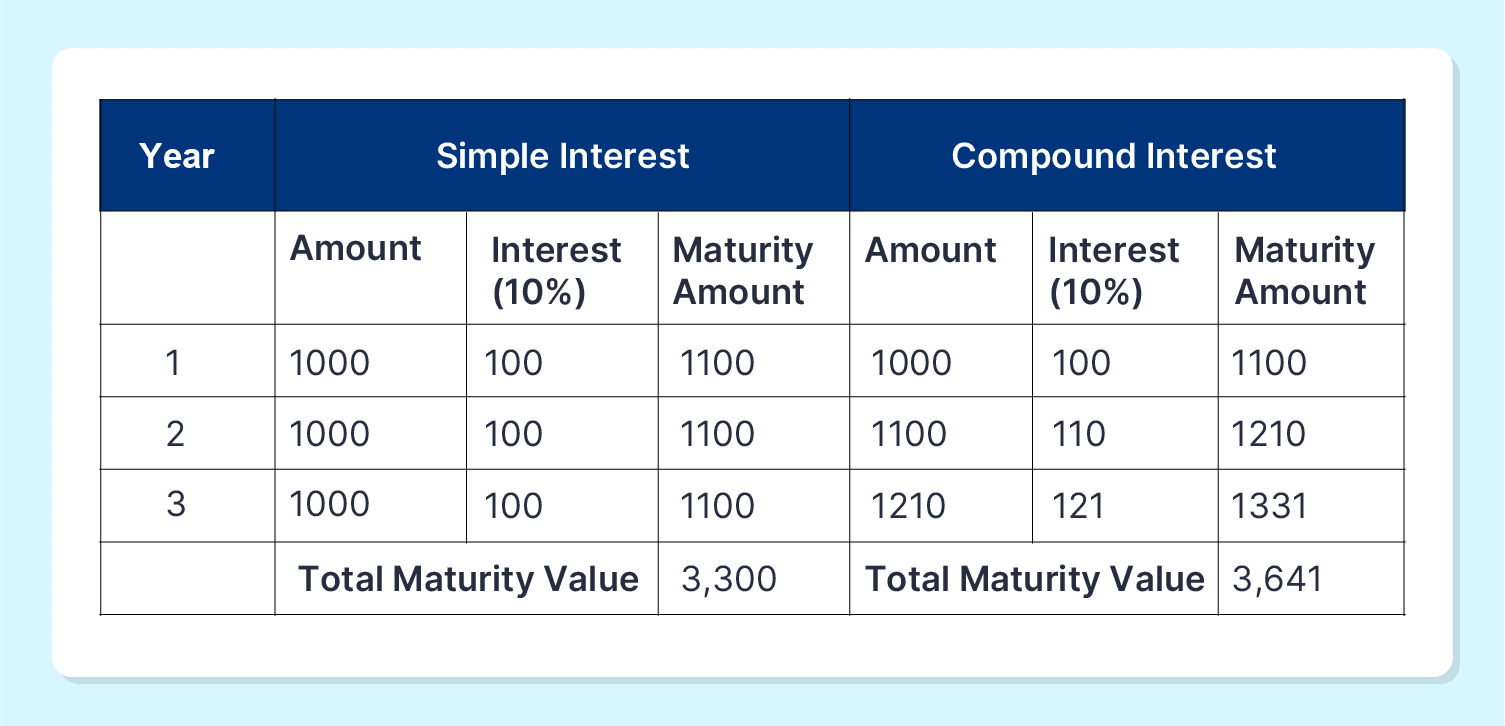

Compounding

In its essence, the process of compounding is quite simple. It is the process of earning interest on both principal and accumulated returns. Therefore, if interest is accumulated, the growth of investment is no longer linear but exponential. Take the table below as example:

Notice how the total amount on maturity is more in the case of compounded interest, even though the principal and rate of interest remain constant. This is because, in the case of compound interest, the interest is levied on both the principal and accumulated return from the second year onward.

Therefore, compounding helps to achieve exponential growth on investment and not just linear growth.

Risk vs Return

The one thing that scares almost every investor during the initial phase of their investment journey is risk. However, risk is nothing but the cost of return. There is a direct relationship between the two. The golden rule of investment is that a rise in return is a result of an increase in risk. The opposite holds for low returns as well.

The key to successful investing lies in maintaining an optimum balance between risk and return based on investor needs and temperament. It is not based on forecasting or timing the market, but a thoughtful analysis of the terms of investment and individual needs, whilst maintaining the rules of investing.

Asset Allocation and Diversification

One of the most prominent methods of reducing investment risk is asset allocation and diversification.

Asset allocation refers to the assignment of a portion of your total investment amount to a particular asset. Portfolio diversification refers to the process of investing in different asset classes.

Although both carry different meanings, they are interrelated. The objective is the reduction of risk through diversification. If one instrument performs poorly, another might perform well enough to mitigate the loss.

What Are Investment Mediums?

Now that the basic concepts and preliminary steps of the investing process are covered, let's move on to the crux of investment.

Investment medium refers to the particular instrument, securities or assets which act as the vehicle of turning savings into investment. For instance, stocks, mutual funds, fixed deposits, etc., can be categorised as investment mediums.

Step-by-Step Guide To Investing In India

Listed below are the steps to start the process of making investments based on the rules-based investment strategies.

Step 1: Choosing the right platform

Investment in securities is usually done through a middleman. The choice of the middleman is necessary because it determines investor comfort. Various banks, brokerage firms and digital brokerage companies act as intermediaries.

Step 2: KYC and Setting Up A Demat account

Customer verification is necessary to start the investment process. It is done through KYC or Know Your Customer. The KYC process usually requires the following documents.

- Identity proof in the form of Aadhaar, PAN, etc.

- Address proof through documents like the utility bills.

- Signatures, biometrics, passport-size photos, etc.

The bank or brokerage firm does the KYC and sets up the demat account. The Demat account, also known as a dematerialised account, stores securities digitally. Just like money is kept in a bank account, securities are kept in a demat account.

Step 3: SIPs vs Lump-sum Investing

Investment in most securities, like mutual funds or ETF, can be done either through a SIP or lump-sum. A Systematic Investment Plan, or SIP, is the process of investing in instalments. It can be chosen based on the revenue flow and the fund availability of the investor.

Step 4: Tracking your investments

It is essential to periodically monitor the performance of the assets to gauge their profitability. Based on their performance over a period, investors can take corrective measures to cover unnecessary losses.

Best Rules-Based Investment Strategies In India (2026)

1. LeaseX

This emerging investment option in India involves investing in an asset that can generate income when leased. Some companies like Grip Invest offer online, hassle-free leasing, enhancing the investment experience.

Returns: With the right platform, investors can potentially earn significant returns with a 15%+ IRR.

Risk Factor: This medium has a low to moderate risk depending on the deal’s credit rating. It is generally less risky than stock markets due to its non-market-linked nature.

2. Equity Market

This traditional investment avenue allows individuals to invest in listed companies directly through stock exchanges (e.g., NSE, BSE) or via equity mutual funds managed by professional fund managers. For those seeking the best way to invest the money in potentially high-yield assets, the equity market remains a top investment option.

Returns: The market's bull phase may garner high returns. Conversely, significant losses are possible in bear markets.

Risk Factor: This platform is risky due to its susceptibility to unpredictable and volatile market forces.

3. Debt Mutual Funds

These funds are invested in government and private debt securities, ensuring a stable and risk-free return on investment without being influenced by market forces.

Returns: They are less volatile and can yield a maximum return of up to 9-11% in 3 years.

Risk Factor: These mutual funds carry a low to medium risk and are suitable for investors with a low-risk appetite.

4. Corporate Bonds

Corporate bonds are debt instruments companies issue to access additional capital for expansion and operations. Corporate bonds are one of the top investment options among investors looking for higher returns than fixed deposits (FDs) through periodic (monthly/quarterly/annual) interest payments.

They offer periodic interest payments and have shown strong performance in India over the past 30 years, especially investment-grade bonds (rated BBB or higher).

Credit Rating | Description |

AAA | Highest safety with the lowest credit risk. |

AA | High safety and timely management of obligations. |

A | Adequate safety levels. |

BBB | Medium credit quality. |

BB | Moderate quality and default risk. |

B | Significant default risk. |

C | High default risk. |

D | Expected to default soon. Lowest safety. |

Source: CRISIL1

Returns: They typically yield an interest rate of 9-12%, making them a better investment plan for those seeking reliable returns.

Risk: Lower risk than stocks but higher than government bonds. Risk varies based on the issuing company's creditworthiness

5. InvoiceX

InvoiceX, offered by Grip Invest, is a top investment option in a credit-rated, diversified form of invoice discounting. It allows companies to borrow against their outstanding invoices. This fixed-income instrument operates under an established RBI framework, providing investors with regular interest payouts and return of principal at maturity. Reputed agencies like India Ratings rate this instrument, making it a good investment option for those seeking stable returns.

Returns: It provides hefty returns of up to 13% IRR, making it a better investment plan for those looking for fixed-income instruments.

Risk: This medium has a low to moderate risk depending upon the credit rating of the deal. It is less risky than the stock market as it is non-market linked.

Read more on Invoice Discounting: What Is It And How Does It Work?

6. Real Estate

Real estate investment involves investing in land and property. It's a relatively stable income source as land values typically increase, keeping pace with inflation. However, investing in real estate requires significant capital and due diligence. Fractional commercial real estate (CRE) has emerged as a convenient alternative for investors seeking high-yielding fixed-income investments without the need for large capital outlays.

Read more on Fractional Investment: A New Era Of Accessible Investments.

Returns: The returns increase as the value of fixed assets like land appreciates, except in extreme circumstances such as war or natural disasters.

Risk Factor: While risks are generally lower than the stock market, investors may face liquidity, market, and interest rate risks.

7. Fixed Deposit

Fixed Deposit (FD) is one of India's most popular investment mediums, particularly favoured by those with a low-risk capability. It offers a fixed interest rate, making it suitable for retirees or those seeking a stable passive income. Modern options also include online FDs and high-yield corporate FDs, providing more flexibility and potentially higher returns. FD is one of the best investment plans for conservative investors.

Returns: FD rates fluctuate based on the repo rate. Currently, they offer approximately 6-7% returns, with some corporate FDs offering slightly higher rates.

Risk Factor: FDs are considered a low-risk investment avenue, especially those offered by established banks and financial institutions.

8. Gold

Investing in gold is considered a safe haven as the demand for this asset increases when the stock market goes down. Gold has an appreciating value and remains one of the most popular investment mediums in the country.

Modern gold investment options include online gold investments, offering returns similar to physical gold without storage concerns, and Sovereign Gold Bonds (SGBs), which provide an additional 2.5% tax-free interest per annum on top of gold price appreciation.

Returns: While not fixed, gold has historically yielded an 11.2% CAGR over the past 20 years. Returns can vary based on global economic conditions and market sentiment.

Risk Factor: It carries relatively less risk than other investment mediums, but global economic factors and currency fluctuations can influence its value.

9. Tax-Free Bonds

These bonds are particularly beneficial for high-income individuals. They offer better returns compared to fixed deposits and taxable bonds, especially after considering tax implications. Tax-free bonds are typically issued by government entities for infrastructure development.

Returns: The interest rate generally ranges from 5.50% to 6.50%.

Risk Factor: The risk factor is relatively low in this avenue.

10. National Pension Scheme (NPS)

NPS is a government-sponsored retirement savings scheme open to all citizens. It allows regular contributions and offers a combination of lump-sum withdrawal and annuity payments upon retirement. The scheme provides flexibility in investment choices and tax benefits.

Read more on National Pension Scheme: Ultimate Guide For Better Retirement Planning.

Returns: The average interest rate is approximately 8-9% for five years, and the risk is very low due to government sponsorship and regulatory oversight.

Risk Factor: It has a lock-in period and allows only limited premature withdrawals.

Common Mistakes To Avoid

Exploration of certain common hurdles in the process of investing through this beginner’s guide to investing might aid new investors. Awareness of the impending or usual roadblocks helps to build caution and thus boosts confidence.

1. Following the crowd

Making an investment decision only influenced by popular sentiment might lead to drastic actions. Investment decisions must be influenced by quantitative analysis of an instrument’s performance.

2. Ignoring inflation and fees

This guide to investing in India began by exploring how inflation eats up the actual value of money. Therefore, if the rate of inflation is more than the return generated by the asset, the depreciation will persist.

Moreover, there are different fees related to investment, for example, fees paid to brokers. If these auxiliary costs are higher than returns, the investment will yield no real value.

3. Over-diversifying or under-diversifying

Diversification has to be done to the optimum extent. Both extremes of overdiversifying or underdiversifying will cause a negative impact on inflation. Just like underdiversifying increases risk, overdiversifying might reduce returns by reducing the invested amount in a particular asset.

4. Lack of patience

In reality, no one can predict the sudden fluctuations in the markets. Therefore, patience is key. Market volatility eases over time. For instance, from 2000 to 2014, the average monthly volatility was around 6.31%, with relatively rare spikes. This shows that while daily price movements can be sharp, volatility generally eases over time as markets stabilize2.

Conclusion

Investment through due diligence and optimum diversification is necessary to achieve financial goals and secure the future. Given the rate of inflation and its impact on the world economy, it is necessary for investors to choose the right investment medium after considering the golden rules of investment.

Understanding and selecting the right investment medium is important for attaining your financial objectives. Whether you're looking for stable returns or a good investment option for diversifying your portfolio, the key lies in strategic decision-making and staying informed about market changes. Choose your investment option according to your needs. Whether you prioritise stability, high returns, or tax benefits, a suitable investment medium awaits you!

Explore Grip Invest and stay updated on all relevant and best investment opportunities.

Frequently Asked Questions On Investment Guide

1. What is the 120 rule in investing?

Based on an investor's age, the 120 rule is a guideline for figuring out the optimal proportion of equities and bonds or fixed-income assets in the portfolio. This guideline states that the investors must deduct their age from 120 to figure out the portion of the fund to be invested in equity. The remaining portion of the portfolio can be invested in fixed-income generating assets like bonds.

2. What is the 10/5/3 rule of investment?

The 10/5/3 rule is used to derive the optimum portfolio expectation for different assets. A 10% annual yield might be derived from investments like stocks, while 5% annual returns might be generated through debt instruments like bonds. The remaining 3% may be derived in the form of cash or cash equivalents, like a savings bank account, to meet the liquidity requirement of an individual.

3. What are some high-return investment options in India?

There are multiple high-return investment options in India, like stocks, mutual funds, ETF, etc. Among mutual funds, small-cap funds seem to provide the highest return. However, it might be important to note that there is a direct relationship between risk and return. High returns will be characterised by high risk. Therefore, a balance between the two is necessary for successful investment.

References:

1. https://www.crisilratings.com/en/home/our-business/ratings/credit-ratings-scale.html

2. http://yojana.gov.in/public-account_2016march.asp

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001