Non-Performing Assets (NPA): Meaning, Causes, Examples And Impact On Economy

The flow of money in an economy should mimic that of blood in a human body, with banks and NBFCs being the heart of the entire system. These financial structures lend capital so that individuals and businesses can grow.

The system of lending also comes with risks. When borrowers do not repay on time, and this happens on a major scale, it creates serious pressure on the financial system.

You may ask what the role of non-performing assets is in this system. Well, NPAs by definition are loans that stop generating income for the lender due to repayment overdues.

The IMF has also linked NPA stress to not only bank issues but also as a worldwide economic concern1. This reduces bank profits while also increasing the cost of credit for everyone. Let’s read through to understand the concept in detail.

Non-Performing Assets: Meaning And Definition

You must understand one crucial risk metric before you evaluate any Banks, NBFCs, or bond issues.

1. Defining Non-Performing Assets

The non-performing assets are advances or loans given by lenders that stop producing any income. This happens because the repayment of the amount has not been received over time.

The lender can no longer treat the loan as income when the borrower fails to pay interest, and hence, NPAs are referred to as ‘bad loans’. As per RBI norms, this tenure of overdue is more than 90 days. This helps analysts and retail investors to track the true health of the credit system.

2. Examples of Non-Performing Assets

The beginning of an NPA can happen with an issued EMI, which later develops into a serious delayed repayment issue. They are considered bad loans as they cause a problem in income generation for lenders such as banks and NBFCs.

A strong NBFC is disciplined underwriting with consistent collections. Let's take Bajaj Finance, for example2. It has reported a typically low gross NPA ratio compared to other lenders. This reflects strong loan monitoring and risk controls. The company highlights asset quality, including metrics and Gross NPA, annually.

Another contradicting example is that of NBFCs that are heavily exposed to risky borrower segments and aggressive unsecured lending3. This shows higher stress in repayment. According to RBI reports, NBFC asset quality trends highlight how GNPA ratios rise under severe stress conditions.

Major Causes Of NPAs In India

The rise of NPA is not due to a single event; it builds over time. This leads to aggressive expansion, weak credit checks, and a slowing of the economy. In India, non-performing assets are linked to lender-specific issues as well as systemic issues. Understanding the underlying reasons can help you judge the strength of a lender’s loan book.

1. Corporate defaults

The large corporate defaults are one of the biggest reasons for the rise of NPAs. This is because when businesses borrow money but later struggle with cash flow, it delays interest payments and stops the repayment of principal completely.

They are more damaging due to the large ticket size. Consequently, this affects investor confidence, especially in listed banks and NBFCs.

2. Economic slowdown

An economic slowdown affects the system. This happens when the borrower's income weakens, and repayments are affected, leading to a rise in non-performing assets.

3. Poor credit assessment

Poor credit assessments cause the rise of NPAs even without a major slowdown. If a loan is approved without proper verification of income stability, repayment capacity, and borrower credit, it can lead to NPAs over time.

Impact Of NPAs

The NPAs' impact on the economy extends beyond bank loans. The non-performing assets weaken credit growth and force leaders to set aside capital.

1. On banks

Usually, for banks, a loan is known to generate an income. This is held stagnant due to non-performing assets and income stops. Consequently, the bank must provide for potential losses. This also reduces the net profit, capital efficiency, and appetite to lend further.

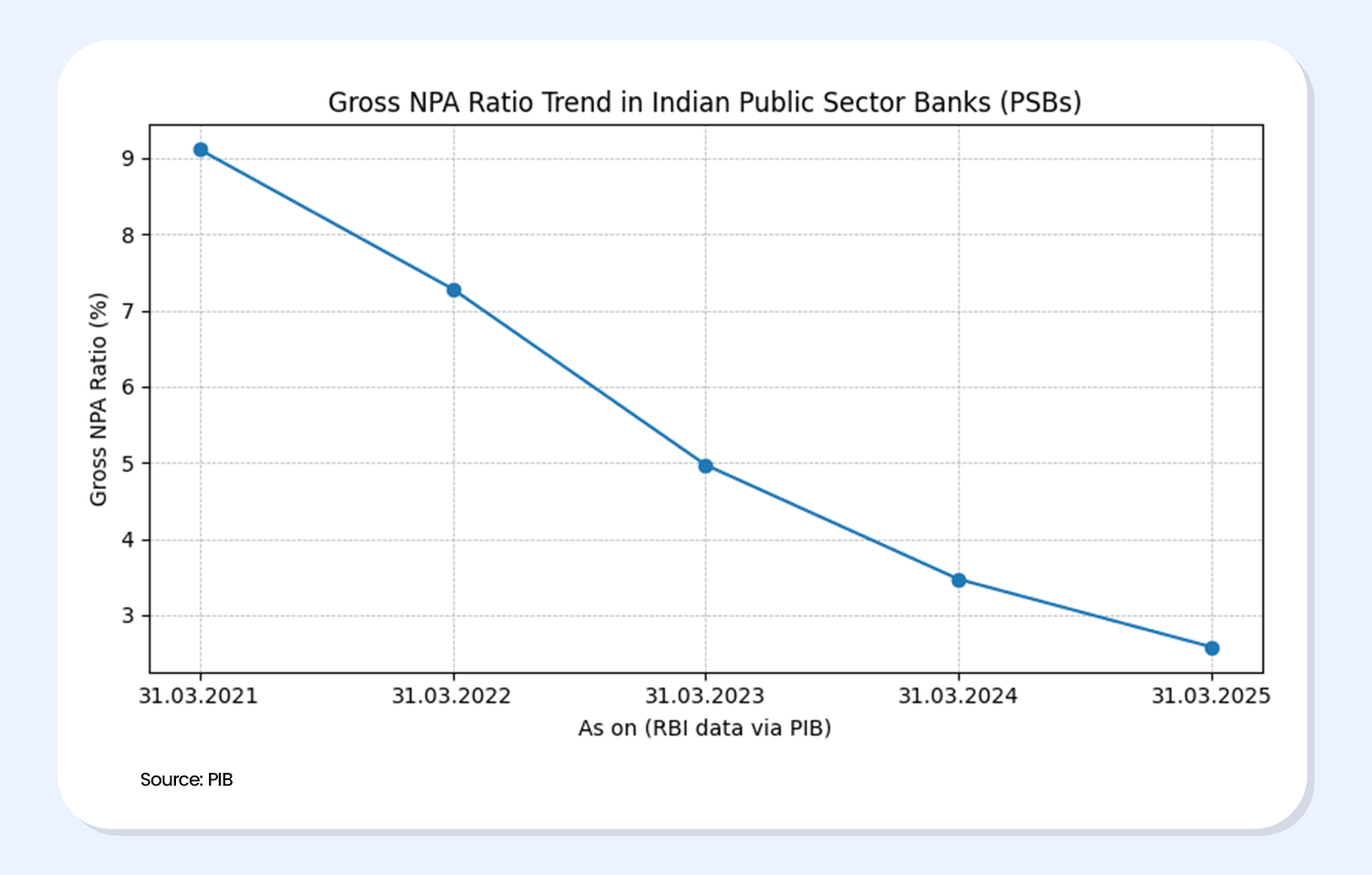

Over the last few years, the asset quality has improved in India. Citing RBI data shows that the public sector banks have seen a decline in Gross NPAs over FY21-FY25, increasing credit qualities and recoveries4.

2. On investors

Higher NPAs usually mean lower profit for investors due to provisioning. It also reduces growth potential and creates higher volatility in stock prices. NPAs are a direct credit risk for fixed-income investors. They cause a higher chance of cashflow stress and increase the probability of delayed coupon payments or weak repayment ability.

3. On the economy

Lenders become conservative when faced with high non-performing assets. They eventually tighten borrower eligibility, approvals, and increase interest rates to cover risks. This reduced the consumption-driven growth and also slowed down business expansion.

4. NPA ratio trend in Indian banking

What NPAs Mean Or Retail Investors

Understanding the effects of NPAs on your investments is crucial. This helps you compare the impact across fixed-income and equity products. The table discusses a basic comparison of equity vs fixed-income investor views based on certain factors.

| Factors | Equity Investor View | Fixed-Income Investor View |

| NPA indications | Bank profitability and quality of the loan book | Strength and credit risks of issues’ repayments. |

| Risk | Lower Earnings | Increased probability of delayed coupons |

| Impact | Valuation pressure and volatility of stock prices | Higher default probability |

| Tips for investors | Seek lenders that have improved asset quality and a stable NPA trend | Seek bonds that include strict due diligence. |

Conclusion

The lender’s loan book health is reflected by the non-performing asset ratio. If NPAs rise, they reduce bank profitability, tighten lending, and increase overall credit risk. This is how NPA affects the economy significantly.

Tracking NPAs can help retail investors assess an issuer’s quality before investing in equity or fixed-income products. Focusing on credit quality and asset health can reduce long-term risks instead of chasing returns blindly.

Platforms such as Grip Invest provide curated options in fixed-income opportunities with strong issue screening. They provide options where issuer evaluation includes credit quality checks and due diligence before listing.

Explore your investment option backed by due diligence and credit quality checks with Grip Invest.

FAQs On NPAs In India

1. What is meant by non-performing assets?

A loan or advance in which the interest or the principal is overdue beyond a time period is known as a non-performing asset. It stops generating income from the lender.

2. When does a loan become an NPA?

A loan is considered an NPA when the repayment is overdue over a definite time period, which is usually more than 90 days, as stated per RBI norms.

3. Why are NPAs bad for banks?

NPAs are considered disadvantageous for banks because they reduce earnings and require provisioning, tighten lending, and weaken credit growth. They also reduce investor confidence and increase financial system risks.

References:

1. IMF, accessed from: https://www.imf.org/en/publications/wp/issues/2019/12/06/the-dynamics-of-non-performing-loans-during-banking-crises-a-new-database-48839?utm_

2. Bajaj finserv, accessed from: https://www.bajajfinserv.in/finance-digital-annual-report-fy24/index.html?utm_

3. FIDCI, accessed from:https://www.fidcindia.org.in/wp-content/uploads/2019/06/RBI_FSR_JUNE_2024_27_06_24.pdf?utm_

4. PIB, accessed from: https://pib.gov.in/PressReleasePage.aspx?PRID=2146819&utm_

5. PIB, accessed from: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2146819&utm_

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001