National Pension System Deduction In New Tax Regime Explained

The Indian income tax system has been evolving, aligning itself with the newer corporate requirements and environment. The system has faced several major changes, including lower tax rates. However, the new tax regime has also eliminated several previously offered traditional deductions.

One such major shift has been in the reduction of NPS deduction in the new tax regime.

What was previously considered one of the stronger tax-saving advantages might not work the same way under the new regime. Therefore, it is crucial to understand what your taxes and overall finances will look like before you make the switch to the new regime.

Can You Claim NPS In A New Tax Regime?

Before getting to NPS deduction in new tax regime, let’s first understand some basics. NPS offers two account types:

1. Tier 1 is the primary retirement account. It has withdrawal restrictions and is linked to tax benefits.

2. Tier 2 is a flexible savings account. It allows you to make easy withdrawals from the account. However, it usually does not provide tax deductions.

The tax treatment of these contributions depends on who makes the contribution, which is defined under Section 80CCD deduction.

- Changes at a glance

Now getting back to the NPS tax benefit new regime, and what has changed. Under the old tax regime, you could claim deductions on your own NPS contributions, along with deductions on employer contributions. However, under the new tax regime, there are no deductions for the contribution made by you.

What has not changed is that your employer's contributions to your NPS account continue to remain available even after opting for the new regime.

- Employer contribution benefit under 80CCD(2)

Now that only employer contributions qualify for tax deduction under the new regime, there will be no tax savings if the employer NPS contribution is significant. From a pure tax-saving point of view, your personal contributions mean nothing under the new regime.

Let us understand this with the help of an example:

If Rahul earns a salary of INR 10 lakh per year and opts for the new tax regime. If Rahul personally invests INR 50,000 in NPS, he will not receive any tax deduction on this amount. His taxable income will still remain INR 10 lakh. On the other hand, if he receives an employer NPS contribution of INR 1 lakh to his NPS account as part of his salary structure. This amount qualifies for deduction, reducing his taxable income to INR 9 lakh.

- Limits and conditions

The deduction on employer contribution under Section 80CCD(2) is available subject to the following conditions:

1. The tax deduction applies only when the contribution is made by the employer on behalf of the employee and deposited directly into the employee’s NPS account.

2. Employer contribution benefits are linked to the Tier 1 retirement account, as tax deductions are available only under this account type.

3. Employer contributions qualify for deduction up to the permitted percentage of an employee’s salary under Section 80CCD(2)

4. This deduction remains available even when a taxpayer opts for the new tax regime.

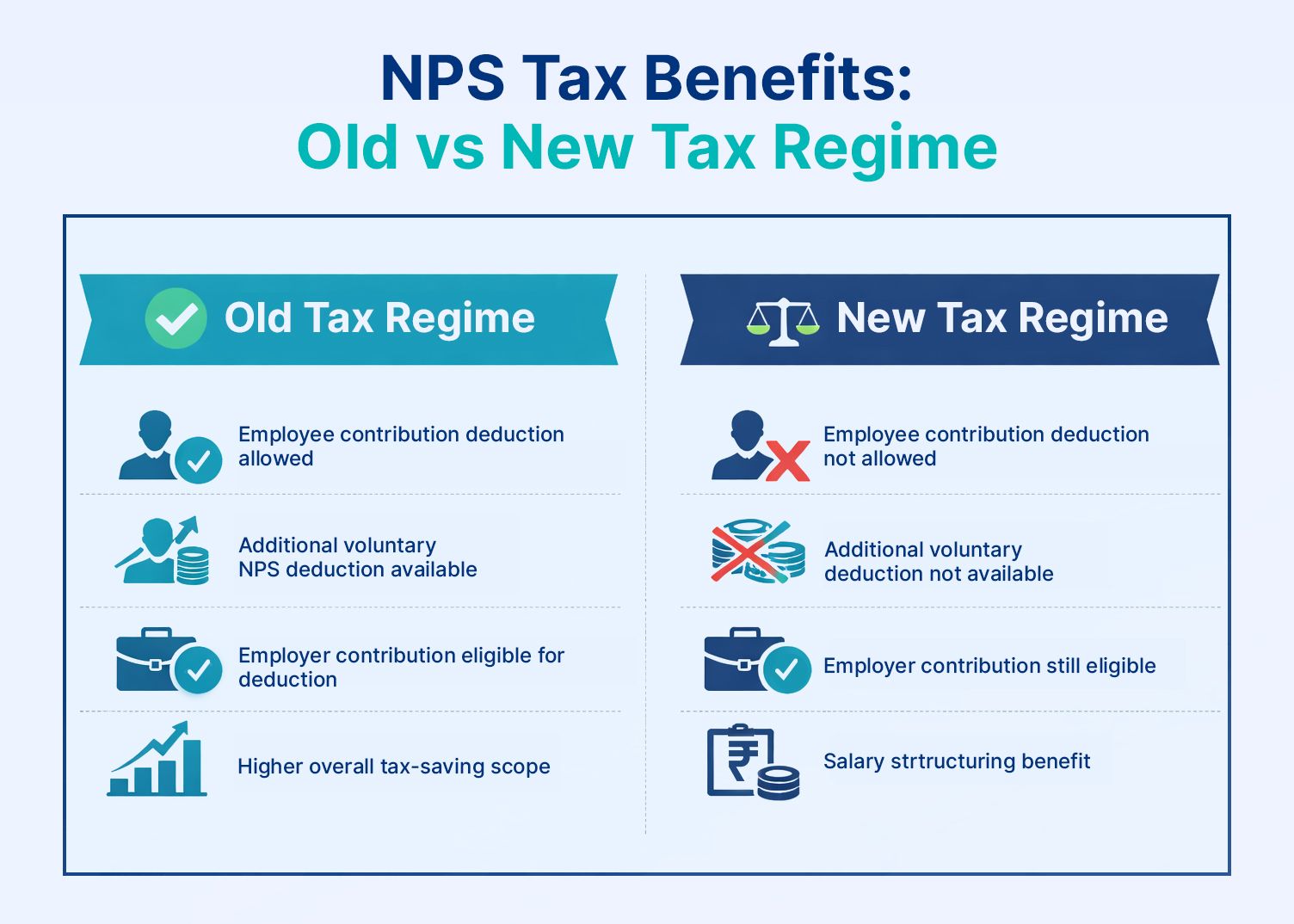

- Old vs New regime NPS deduction comparison

Feature | Old Tax Regime | New Tax Regime |

| Employee NPS contribution | Allowed | Not allowed |

| Additional voluntary contribution | Allowed | Not allowed |

| Employer contribution | Allowed | Allowed |

| Overall tax-saving scope | Higher | Limited |

| Best suited for | Deduction-based planning | Salary structuring |

How Much Tax Can You Save?

Tax savings under the new tax regime mainly depend on employer participation in NPS contributions. Since personal investments do not qualify for a deduction, tax benefits arise only when employers contribute to an employee’s NPS account. Employer contributions are eligible for deduction up to 10% of salary (Basic Salary plus Dearness Allowance) for non-government employees and up to 14% for Central Government employees.

This deduction reduces taxable income while continuing to support long-term retirement savings, making it relevant for salaried NPS tax saving 2026 planning.

NPS Withdrawal Taxation

Taxation under NPS applies mainly at the withdrawal stage after retirement. Understanding the NPS withdrawal tax new regime treatment is important, as taxation shifts from contribution-based benefits to post-retirement income. Upon maturity, a subscriber may withdraw up to 60% of the accumulated corpus as a lump sum, which is treated as tax-free income.

The remaining minimum of 40% of the corpus must be used to purchase an annuity plan that provides regular pension payments after retirement. While the annuity purchase itself is not taxed, the pension income received from the annuity is taxable according to the applicable income tax slab in the year it is received.

Should You Invest in NPS Under New Regime?

If you are wondering whether you should continue investing in NPS deduction in new tax regime, the answer largely depends on why you started contributing in the first place. If your primary goal was tax savings, the new regime may reduce its immediate advantage since personal contributions no longer qualify for deductions.

However, if your objective was to build a reliable retirement safety net, NPS still remains a disciplined long-term option.

The decision also depends on how much your employer contributes, as employer NPS contributions continue to qualify for deductions within the prescribed limits. With proper financial planning or expert guidance, NPS can still be aligned with long-term retirement goals even under the new system.

Conclusion

The NPS deduction in new tax regime has clearly shifted from being a personal tax-saving tool to a salary-structuring advantage. While individual contributions no longer reduce taxable income, employer contributions under Section 80CCD(2) continue to offer meaningful tax efficiency. What this really means is that NPS now works best when it is aligned with your compensation structure and long-term retirement planning, not just short-term tax reduction.

If your employer contributes within the permitted limits, the new regime can still deliver tax benefits while helping you build a disciplined retirement corpus. And even without personal deduction benefits, NPS remains a structured, low-cost retirement vehicle designed for long-term wealth accumulation.

When planning retirement, it’s important to look beyond just deductions and evaluate the broader fixed-income mix in your portfolio. Platforms like Grip Invest can help investors explore diversified fixed-income opportunities alongside retirement-focused instruments, allowing you to build a balanced strategy that aligns tax efficiency with long-term financial security.

FAQs

1. Is NPS allowed in the new tax regime?

Yes, NPS investment is allowed under the new tax regime. However, only employer contributions made to an employee’s account remain eligible for tax deduction under the NPS Tier 1 deduction new tax rules. Deductions on an individual’s own NPS contributions are not available after opting for the new regime.

2. How much can the employer contribute?

Employer contributions to NPS qualify for deduction under Section 80CCD(2). The deduction is allowed up to 14% of salary for Central Government employees and 10% for other employees, making it an important opportunity for salaried NPS tax saving 2026 under the new tax regime.

3. Is NPS maturity taxable?

At retirement, a subscriber can withdraw up to 60% of the accumulated corpus as a lump sum, which is tax-free. The remaining 40% must be used to purchase an annuity that provides pension income. Under NPS withdrawal tax new regime rules, the pension received from the annuity is treated as taxable income in the year it is received.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001