National Savings Certificate (NSC): Interest Rate, Eligibility And Tax Benefits

The Indian investment landscape is witnessing dynamic growth. Between March 2020 and February 2025, the National Stock Exchange added 11.2 crore new investors1. However, it is also worth noting that it took NSE, which was established in 1994, 14 years to achieve the one crore investor mark.

A primary reason for this is the heterogeneous nature of the Indian population, which has given rise to unique investor needs. Therefore, while a particular investor craves growth, another might focus more on safety and stability. But, does low risk mean poor return?

The Government of India is set to maintain a 7.7% National Savings Certificate or NSC interest rate from 1 April 2023 to 30 September 2025, which is quite competitive compared to several FD rates2. But before getting into the NSC interest rate, investors must first ask what NSC is and how to invest in it.

What Is A National Savings Certificate?

The Indian government started the National Savings Certificate in 1989. This low-risk scheme allows you to grow your capital with a fixed return and the added benefit of tax savings.

It is a bond scheme, an ideal savings and investment plan for small—to mid-level investors. It is easily accessible to citizens through every post office in India.

Features And Benefits Of NSC

Features Of NSC

The following are the features of the NSC certificate:

1. Interest: The government decides to revise the interest in the NSC savings scheme quarterly. As of 1 August 2025, the NSC provides an interest rate of 7.7% p.a.. Moreover, it has remained unchanged for the 1st quarter of 2025-26, according to the latest notification3.

2. Minimum Deposit: The minimum investment amount under NSC is as low as INR 1,000, with no maximum limit.

3. Lock-in Period And Premature Closure: The lock-in period for NSC is five years. It can be closed only for the following exceptions:

- If the account holder or all the account holders in a joint account dies

- If a Gazetted Officer forfeits it

4. Transfer Of NSC account: The NSC savings scheme can only be transferred under the following conditions

- It can be transferred to legal heirs or nominees of the deceased account holder

- It can also be passed to a joint account holder in case of the account holder's death.

- When the account is pledged to a specific authority.

Benefits Of NSC

NSC is an income investment where pre-determined interest is updated quarterly. Some other benefits of investing in NSC are:

1. Accessibility: NSC savings schemes are easily accessible as they are available through post offices located in every city and village throughout the country.

2. Safe And Secured Investment: National Savings Certificates are backed by the government, and the interest rate on the scheme is decided by the government, making them safe and secured.

3. Low Initial Investment: They do not require a significant investment and can be opened with just INR 1,000.

While NSC has several key benefits, it is necessary to establish a synergy between its characteristics and investor temperament to ensure an optimal incorporation of NSC interest rate into financial planning.

Who Should Invest In NSC?

Investors seeking safe and predictable passive income with moderate interest rates and tax benefits can consider investing in an NSC.

The following people can apply for National Savings Certificate:

- A single adult

- Joint Account (for at most three adults)

- A minor above ten years in their name

- A guardian on behalf of a minor or someone of unsound mind

Apart from investor suitability, another key consideration before undertaking any investment is the applicable tax structure.

Tax Benefit Of NSC Investment

The tax rates applicable to an investment medium diminish the actual return that can be generated. Therefore, to explore the effectiveness of the NSC interest rate, the points below explain the taxability of NSC.

- The amount invested in NSC qualifies for tax deduction under Section 80C. The maximum deduction allowed under this scheme is INR 1.5 lakh per financial year.

- Interest earned under NSC is not entirely tax-free. However, it is not taxed annually but rather on maturity at the investor's applicable slab rate, allowing investors to defer the tax liability on the interest until the maturity of the NSC.

Considerations To Keep In Mind When Investing In NSC

Key considerations to keep in mind when investing in the National Savings Certificate (NSC) are:

- Interest Rate: The NSC offers a fixed interest rate, which the Ministry of Finance reviews quarterly.

- Investment Tenure: NSC has a lock-in period of 5 years.

- Eligibility: Only resident Indians can invest in NSC. Hindu Undivided Families, Trusts, Non-resident Indians, and Public and Private limited companies cannot.

Finally, after all the above considerations, if an investor decides to choose NSC as an investment medium, they must explore the ultimate guide given below.

Step-by-Step Guide On NSC Account Opening

Investment in NSC must be done through a Post Office. However, before taking a look at the steps involved in investing to get the NSC interest rate, we must keep some documents handy.

Documents Required to Get NSC Interest Rate

Listed below are the documents required for NSC investment.

- Passport Size Photo

- Aadhaar Card

- PAN Card

- Proof of Age (like Birth Certificate)

- Passport

- Driver’s License

- Voter ID Card

- If the investor is an NREGA (National Rural Employment Guarantee Act) beneficiary, then the investment might require their job card, which is signed by the State Government.

Source: My Scheme4

Once the documents are streamlined, the investor can visit the post office and start their NSC investment process to get the NSC interest rate.

Step 1: Visit the Post Office and ask for the NSC application form. You can also download Form 1 from the official website5.

Step 2: Fill out the required form and attach the relevant documents.

Step 3: Investors also need to sign a declaration and provide nominee information.

Step 4: Once the form process is complete, submit it along with the investment amount.

Step 5: Once the onboarding process is complete and the NSC investment is initiated, an official confirmation will be sent to the official email or phone number.

However, investors can also invest in NSC online.

Get NSC Interest Rate In 5 Online Steps

Investment in National Savings Certificates can also be done online, provided you have a savings account with any post office. Discussed below are the steps involved in online NSC investment6.

Step 1: Log in to the Department of Posts Net Banking website. Investors would be able to access this and invest to get the NSC interest rate only if they have a savings account with net banking enabled.

Step 2: Select Service Requests from the General Services option.

Step 3: Click on New Requests and then choose the NSC new account opening option.

Step 4: Enter the amount you wish to invest, along with the account details of the Post Office deposit account. Ensure that the account has sufficient funds so that the amount can be credited.

Step 5: Once the password or OTP is entered, along with consent to the terms and conditions, a deposit receipt appears, confirming the NSC investment.

Since we understand how NSC investment is done, let us take a keen look at the method of compounding that makes the NSC interest rate lucrative to investors.

NSC Interest Rate: How NSC Compounding Works

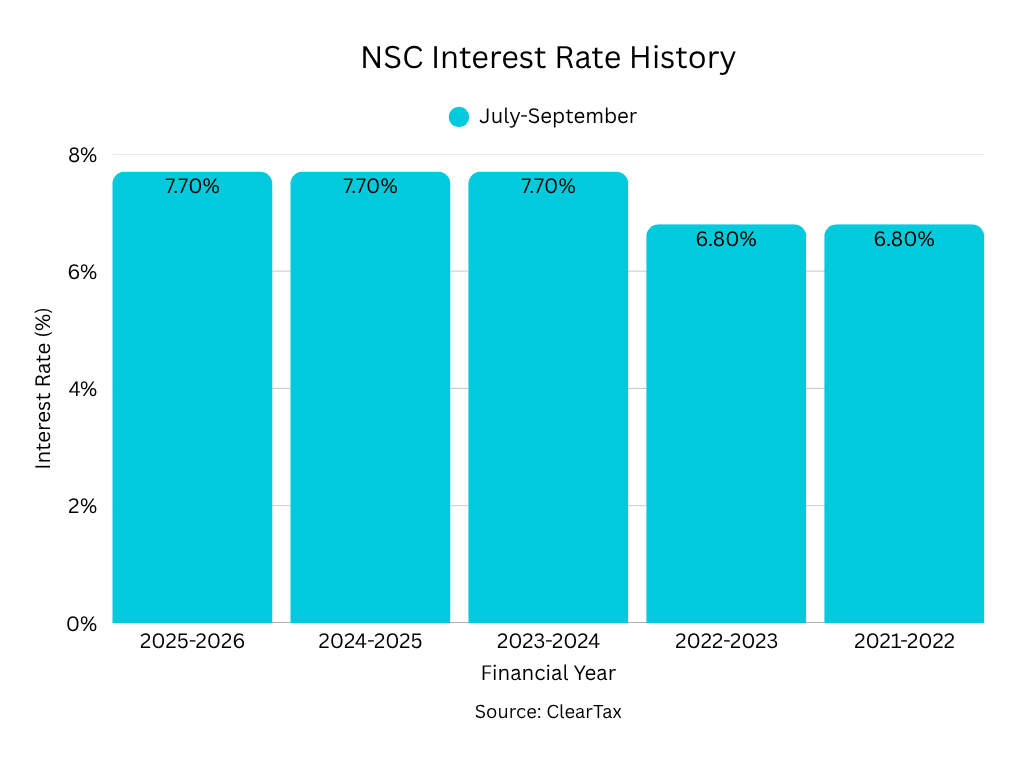

The NSC interest rate is compounded annually. Before understanding how the compounding works, let us first take a look at the interest rate applicable for the last 5 years.

| Year | Interest Rate (%) |

| 2025 to 2026 (Q1) | 7.7 |

| 2024 to 2025 | 7.7 |

| 2023 to 2024 | 7.7 |

| 2022 to 2023 | 6.8 (Increased to 7 in the last quarter) |

| 2021 to 2022 | 6.8 |

Now, imagine you invested INR 3000. Assuming an interest rate of 7% for ease of calculation, let’s explore the impact of compounding.

| Year | Principle (INR) | Interest (INR) | Amount (INR) |

| 1 | 3,000 | 210 | 3210 |

| 2 | 3210 | 224.70 | 3434.70 |

| 3 | 3434.70 | 240.42 | 3675.12 |

| 4 | 3675.12 | 257.25 | 3932.37 |

| 5 | 3932.37 | 275.26 | 4,207.63 |

Due to the power of compounding, the yield increases. Reinvestment of small gains can aid in generating a higher return over time. Therefore, while INR 210 might not seem meaningful, a return of approximately INR 1207.63 is quite significant in this case.

Other than these tax-saving investment avenues, some other investments can also seem attractive to risk-averse investors, looking for stability and growth.

NSC vs PPF vs ELSS vs FD: Which One Should You Pick?

The table below compares some popular investment avenues with the National Savings Certificate to understand the effectiveness of the NSC interest rate.

| Parameters | National Savings Certificate (NSC) | Public Provident Fund (PPF) | Equity Linked Savings Scheme (ELSS) | High-Yield Fixed Deposits |

| Meaning | A savings certificate backed by the government with fixed government-notified interest | Tax-saving investment scheme provided by the government for tax-saving retirement investment | Funds that invest in equity or equity-linked investments | Deposits held with a bank for a fixed tenure at a given rate of interest. |

| Maturity | 5 years | 15 years | According to the investor | According to the investor |

| Interest (current) | 7.7% | 7.1% | 21.94% (5 Years Category Average)7 | 10% pre-tax IRR on Grip |

| Minimum Investment | INR 1000 | INR 500 | Depends on the fund house | INR 1,000 |

| Maximum investment | None but investment must be in multiples of 100 | INR 1,50,000 per Fiscal Year | None | None |

However, the NSC interest rate is not the only consideration. Since the investment certificate is an important document, investors must also consider what happens if they lose it.

How To Request A Duplicate National Savings Certificate

You can get a duplicate NSC even if you lose your original NSC certificate through the issuing post office by filing the following information in the Duplicate Savings Certificates form:

- Serial numbers, denominations, NSC issue details, and other certificate information

- Purchase dates of the certificates, the reason for requesting a duplicate certificate, and any additional information

Conclusion

The National Savings Certificate (NSC) Scheme presents a compelling opportunity for a low-risk investment. It is easily accessible as the minimum investment amount can be as low as INR 1,000. With ease of online and offline investment, NSC is a dependable option for those looking to safeguard their financial future while enjoying tax benefits.

Explore Grip Invest- India's one stop destination for fixed income returns and stay updated on all relevant financial planning opportunities.

Frequently Asked Questions On NSC

1. Is there any tax benefit for NSC?

Yes, NSC qualifies for tax deductions of up to INR 1.5 lakh in a financial year under Section 80C of the Income Tax Act, 1961.

2. Is TDS deducted on NSC interest?

No, TDS is not deducted from the interest earned through NSC. However, tax is payable on the interest earned in the last financial year.

3. Is the NSC interest rate fixed for five years?

No. The government revises the interest quarterly, ensuring alignment with prevailing market conditions.

References:

1. Fortune India, accessed from: https://www.fortuneindia.com/markets/strong-retail-participation-is-propelling-the-indian-stock-market-to-a-higher-global-rank-assocham-icra-report/123337

2. NSI India, accessed from: https://www.nsiindia.gov.in/(S(odzghxzxgksy4355rkjfhj45))/InternalPage.aspx?Id_Pk=182

3. NSI India, accessed from: https://www.nsiindia.gov.in/(S(erpt4x55q1u0v155dvr0qia1))/InternalPage.aspx?CircularId=9999

4. My Scheme, accessed from: https://www.myscheme.gov.in/schemes/nscs

5. NSI India, accessed from: https://www.nsiindia.gov.in/(S(lelmawykm1nnkfa215fsco2g))/InternalPage.aspx?Id_Pk=38

6. LiveMint, accessed from: https://www.livemint.com/money/personal-finance/national-savings-certificate-how-to-invest-in-nsc-offline-and-online-heres-a-step-by-step-guide-11705495975176.html

7. Morning Star, accessed from: https://www.morningstar.in/tools/mutual-fund-category-performance.aspx

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001