Pradhan Mantri Jan Dhan Yojana: Benefits, Eligibility, Features And Impact

The banking industry in India is opening up to thousands of people due to the Pradhan Mantri Jan Dhan Yojana. This innovative programme creates a gateway for individuals to have access to financial services and increase their chances of obtaining funds.

Easy funding accessibility is one of the most important ways we can grow our tremendously diverse country. In fact, prior to this initiative, many households in India did not have a bank account.

With the introduction of this scheme, banking has become easily accessible to both urban and rural poor. This scheme also encourages consumers to build their own savings and become active participants in the economy.

What Is Pradhan Mantri Jan Dhan Yojana

Pradhan Mantri Jan Dhan Yojana seeks to give every household access to a bank account. The initiative was introduced in 2014 and was aimed at delivering services for families who have little connection with financial institutions.

By doing so, the ultimate goal of the programme is to encourage families in India to save money and gain access to credit through the use of a bank account.

Jan Dhan account eligibility is for anyone who is at least 10 years old and that too with no minimum balance requirement to be maintained on any account. Only people who do not already have a bank account are eligible to apply for a Jan Dhan account, although all members of a household can open an individual account.

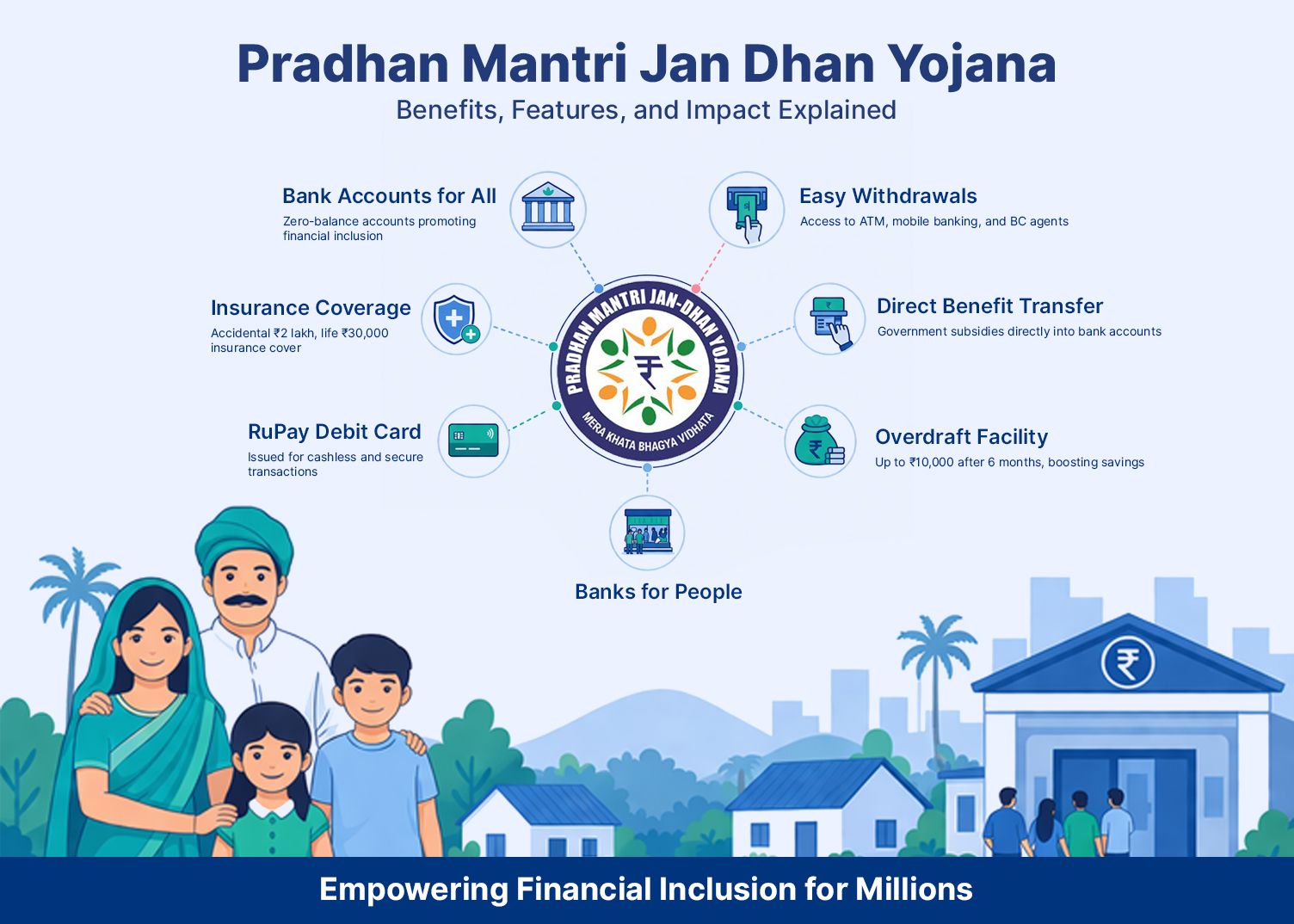

Key Features Of Pradhan Mantri Jan Dhan Yojana

The definition of a zero-balance account in India is based on the features a Jan-Dhan account has.This flexibility caters perfectly to our daily wage earners.

- Every Jan-Dhan account owner will receive a PMJDY RuPay debit card, which can be used for withdrawal from ATMs and as a point-of-sale payment method throughout the country.

- Every account owner can use Jan Dhan overdraft facility of up to Rs. 10,000 after the initial six months of opening an account. Once regular deposits are made in an account, access to this overdraft facility will be automatically available to you.

- The PMJDY scheme also includes accident insurance in the amount of up to INR 2 lakhs for every PMJDY cardholder. This benefit is automatically activated over time through transactions completed using your PMJDY card and protects you while you perform transactions.

The PMJDY Program 2026 is reinforcing the initiatives in the Jan-Dhan Program in the digital age.

Benefits For Individuals

The basic banking service is the starting point of PMJDY benefits for those who have been unbanked until now. The subsidy scheme is transferring money immediately from the government directly to the consumer without any delays.

The introduction of zero balance accounts for the lower-income households will enable this unbanked segment to access banking services free of charge (PMJDY).

For instance, a farmer in a rural village can now open an account where he receives money for a crop subsidy payment right into his account. He may also use his PMJDY RuPay debit card at the local grocery store to make purchases and develop good financial habits.

Women and youth were the primary emphasis of the Pradhan Mantri Jan Dhan Yojana (PMJDY). As a result, women now hold more than 55 percent of the accounts opened with PMJDY and are increasingly financially independent.

Additional benefits under this scheme include scholarships and insurance that connect seamlessly to the national PMJDY infrastructure.

Economic Impact Of PMJDY

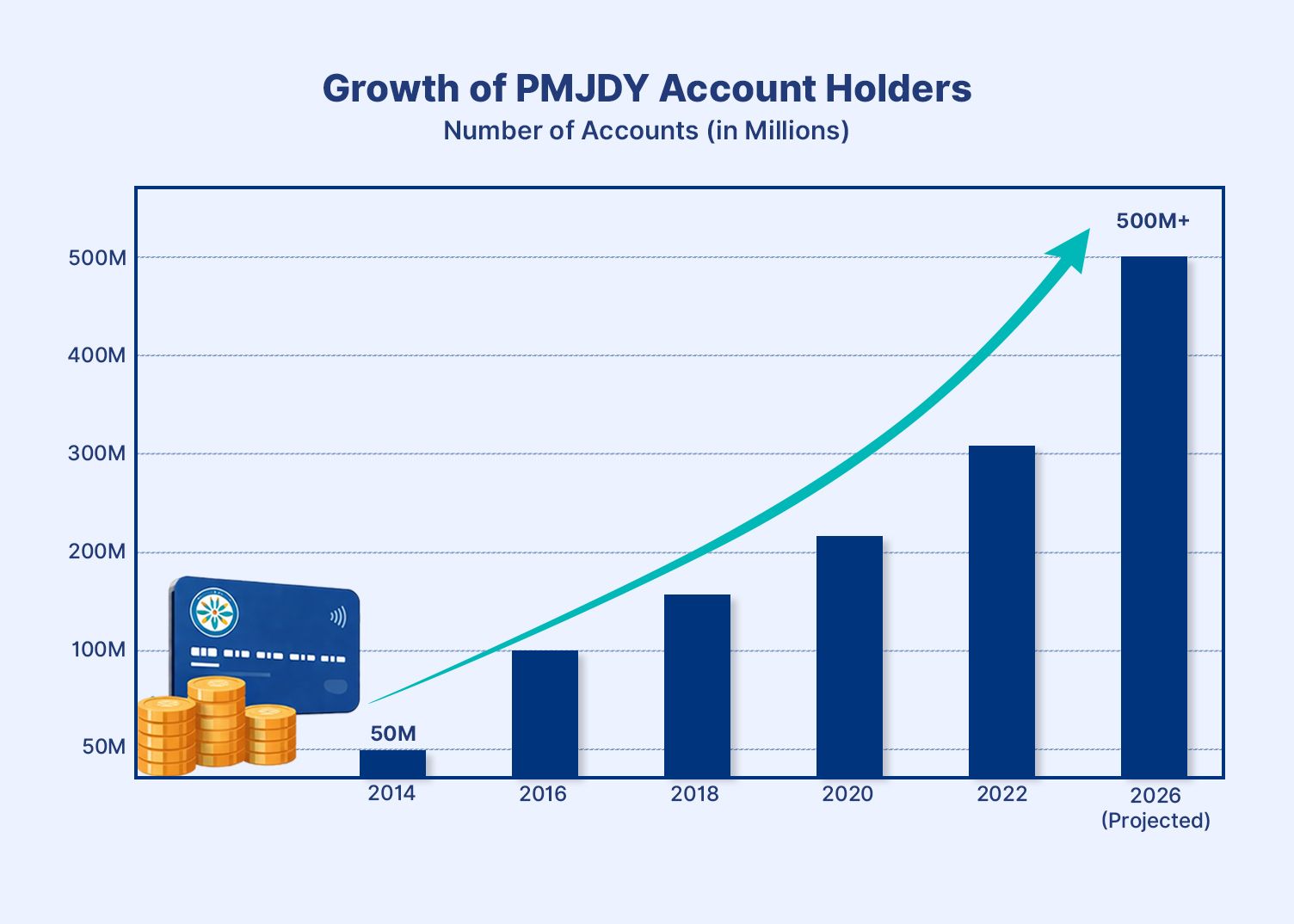

Consequently, the Pradhan Mantri Jan Dhan Yojana (PMJDY) is having a substantial impact on the economy through financial inclusion India solutions. By 2026, there will be over 530 million accounts opened that will link millions of individuals to a formal banking system and decrease the dependence on cash while limiting the flow of black money.

In addition, the Pradhan Mantri Jan Dhan Yojana (PMJDY) is helping promote the digital economy through the use of Aadhaar linking with mobile banking. The number of mobile banking transactions is expected to continue to increase yearly as more people use mobile banking for their day-to-day purchases by 2026. The use of UPI payments in rural areas has expanded dramatically as well.

For Example:

A small business owner may use an overdraft to purchase stock for resale. If the owner relies on his/her business sales to pay back the overdraft, this will have a significant financial impact on everyone involved in producing that product. This result in creating opportunities for jobs and increased economic activity across the country.

What This Means For Investors

To help you clarify differences between Jan Dhan accounts and Savings accounts:

1. The PMJDY is an entry-level banking product, whereas a Savings account has a higher interest rate on your funds. However, the Pradhan Mantri Jan Dhan Yojana will be used as a pathway to wealth.

2. If you have no balance in a bank account in India, you can open an account. Once your PMJDY account opening is done, you may want to invest the money you have deposited into your account.

There will be easy access to your PMJDY Account through various means, like using your PMJDY Account to purchase investment products.

3. A secondary component of integrating your investments into a PMJDY account involves transferring funds from your PMJDY Account to an investment platform of your choice. If you would like to see how well your investments are doing, you can use beginner-type investment apps.

Account Opening Process

Through the account opening process of a PMJDY, you can go to any branch of any bank or business correspondent, as long as you have your Aadhaar, Voter ID, or Ration Card for identity verification. After filling out the required application form, you will receive your passbook right away.

There are no identification or documentation requirements to open an account for a child, as long as an adult guardian is completing the process. As soon as you provide your mobile phone number to your bank, you will get a notification via text message about your accounts. Many banks also provide the option for customers to complete the application process for a PMJDY account online through their banking app.

Emergency Support: Overdraft And Insurance Cover

To qualify for an overdraft with a Jan Dhan account, you must have three months' worth of banking activity. If you have a qualifying amount (overdraft) and have a need for funds beyond your account balance, you can access your account in times of emergency, without having to worry about providing collateral.

If you have been involved in an accident, you get a claim through the accident insurance policy provided with your PMJDY account. This means your family can file the claim for a benefit of up to Rs 2 lakh. This type of safety net allows families to build trust in the formal banking system.

Comparison With Other Schemes

PMJDY acts as the foundational account through which account holders can directly access a web of social security, insurance, pension, and credit schemes, making it a single-window gateway to India's financial inclusion ecosystem

| Linked Scheme | How It Connects | Key Benefit to Account Holder |

| Atal Pension Yojana (APY) | Jan Dhan account holders can directly enroll in APY using their existing account | Guaranteed monthly pension of INR 1,000-INR 5,000 post-retirement; government co-contributes 50% or INR 1,000 (whichever is lower) for eligible subscribers |

| PM Jeevan Jyoti Bima Yojana (PMJJBY) | Auto-debit of annual premium (?436/year) directly from the Jan Dhan account | Life insurance cover of INR 2 lakh on death due to any cause; cumulative enrolment has crossed 23.12 crore |

| PM Suraksha Bima Yojana (PMSBY) | Linked via Jan Dhan account with auto-debit of INR 12/year | Accident insurance cover of INR 2 lakh for accidental death or permanent disability |

| Direct Benefit Transfer (DBT) | PMJDY account serves as the designated account for government subsidy credits | Subsidies from 14 ministries across 57 national programmes credited directly, eliminating intermediaries; INR 6.9 lakh crore transferred in FY 2024–25 alone |

| PM-KISAN | Farmers link their Jan Dhan account on the PM-KISAN portal via Aadhaar seeding | INR 6,000/year (in 3 instalments) credited directly to 11+ crore farmer beneficiaries |

| MUDRA Scheme (PMMY) | Jan Dhan account activity and history supports micro-credit eligibility assessment | Access to collateral-free business loans from INR 50,000 up to INR 20 lakh for micro-entrepreneurs |

| JAM Trinity (Jan Dhan–Aadhaar–Mobile) | PMJDY is the core banking layer of the JAM infrastructure | Single account enables unified KYC, UPI-based premium/pension payments, and seamless data portability across all linked schemes |

Conclusion

The Pradhan Mantri Jan Dhan Yojana has played a transformative role in expanding financial access across India by bringing millions into the formal banking system. With features like zero-balance accounts, overdraft facilities, RuPay debit cards, and insurance coverage, PMJDY has created a strong foundation for financial inclusion, especially for underserved communities.

Beyond just access to banking, the scheme encourages savings habits, enables direct benefit transfers, and promotes participation in the digital economy. Over time, it also acts as a stepping stone for individuals to explore broader financial opportunities, including investments and wealth creation.

As individuals progress from basic banking to building wealth, diversifying into structured investment options can help generate more stable and predictable returns. Platforms like Grip Invest offer access to curated fixed-income opportunities, enabling investors to take the next step beyond savings and work towards long-term financial growth.

FAQs On PMJDY

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001