Retirement Benefits In India 2026 | Employee Pension, EPF, NPS Explained

Introduction: Retirement Benefits In India

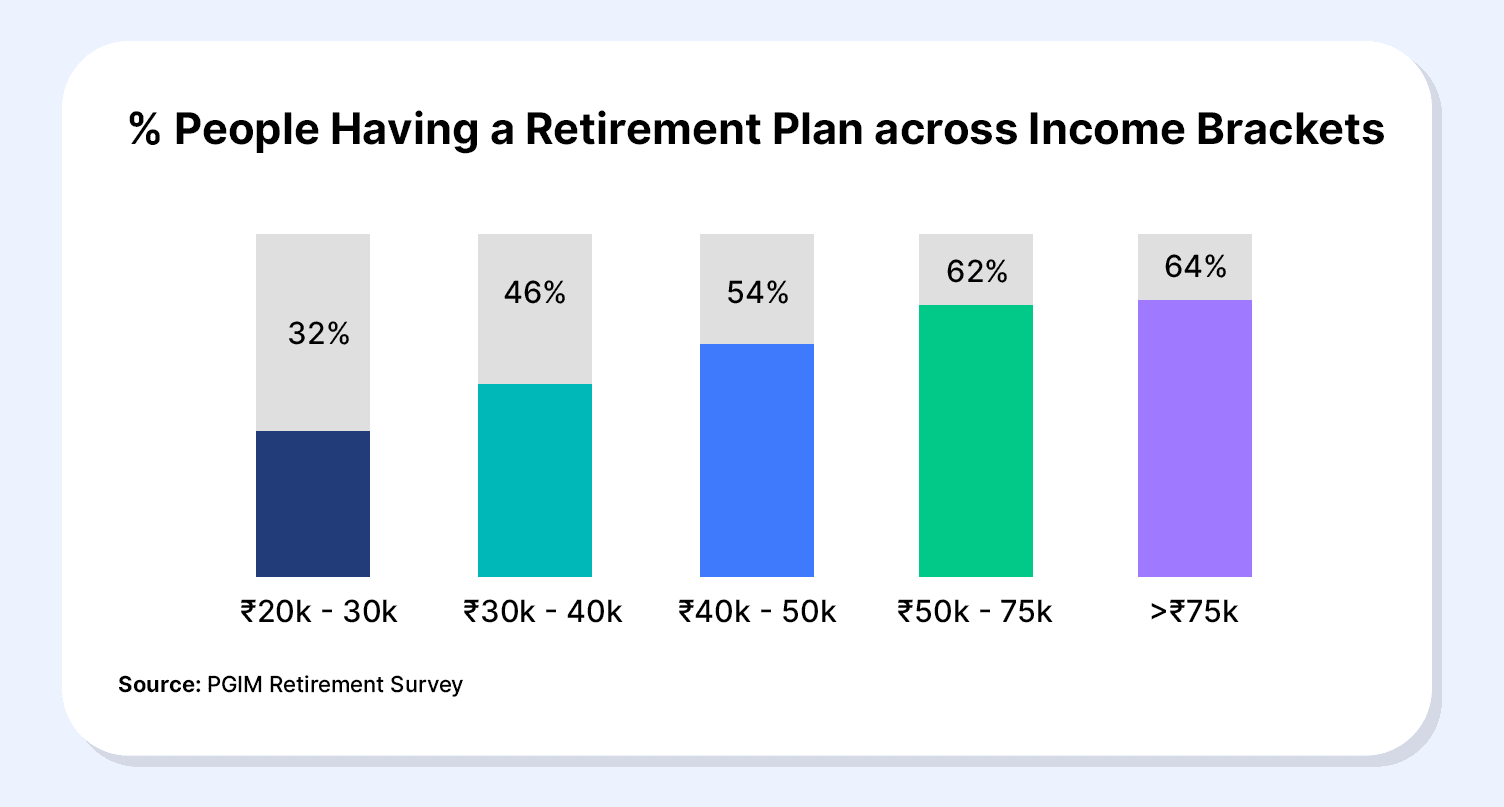

Retirement planning in India is no longer optional—it is a financial necessity. With people living longer and career paths becoming less predictable, employees must take charge of their future security. By 2026, understanding the range of retirement options available is crucial to building lasting financial stability.

Government-backed schemes like the Employees’ Provident Fund (EPF) and Employees’ Pension Scheme (EPS) continue to form the core of retirement savings, while newer initiatives such as the Unified Pension Scheme (UPS) and the National Pension System (NPS) offer flexible, market-linked alternatives1.

Together, these schemes create a well-rounded safety net designed to adapt to modern financial needs. Yet, relying solely on statutory benefits is not enough—strategic investments in mutual funds, fixed deposits, and annuity plans can further enhance post-retirement income. Balancing these tools smartly ensures not just financial security, but the peace of mind that comes with a truly comfortable retirement.

The next section explores the key retirement benefits in India that help build this foundation.

Key Retirement Benefits In India

1. Employees’ Provident Fund (EPF)

EPF remains the backbone of retirement planning for salaried workers. Both employees and employers contribute 12% of the basic salary plus dearness allowance monthly. As of 2026, EPF offers an attractive interest rate of approximately 8.5% annually, with compounding that helps build a substantial corpus over time.

The fund is locked in until retirement or resignation after five years of continuous service, providing a lump sum along with interest. It is ideal for employees seeking a low-risk, government-backed retirement corpus.

Also Read: EPFO 3.0Navigating The Withdrawal Rules

2. National Pension System (NPS)

NPS is a voluntary, market-linked pension scheme introduced to provide employees flexibility and potentially higher returns, averaging around 9-10% owing to its equity and debt exposure. Contributions are flexible, and partial withdrawals before retirement are permitted under specific conditions. Post-retirement, roughly 40% of the corpus can be withdrawn as a lump sum, while 60% must purchase an annuity that provides a monthly pension. NPS also offers additional tax benefits under Section 80CCD(1B), allowing deductions up to INR 50,000 above the standard 80C limit3.

3. Gratuity

Gratuity is a lump sum payment from an employer to an employee who has completed a minimum of five years with the company. The amount is usually calculated using the formula: 15 days' salary for every year of service, subject to a ceiling of INR 20 lakh as per the latest gratuity rules of 2025. This payment is tax-exempt up to the ceiling and serves as a crucial financial cushion at retirement.

4. Employees’ Pension Scheme (EPS)

Linked with EPF, EPS offers employees who contribute to EPF for at least 10 years a guaranteed monthly pension post-retirement. The pension amount depends on the number of contribution years and the average salary. EPS provides a steady and reliable source of monthly income, though it is taxable. Additionally, family members receive a 60% pension in case of the employee’s death.

5. Unified Pension Scheme (UPS)

The UPS, a new government initiative launched in 2025, aims to streamline different pension schemes into one simplified vehicle. It promises a minimum monthly pension of INR 10,000 for employees with at least 10 years of service and up to 50% of the last drawn salary for those with 25+ years4. Family pension benefits and inflation adjustments through Dearness Relief are integral features, enhancing post-retirement financial security.

Retirement-Focused Insurance

Insurance policies tailored for retirement provide options like annuities and lump sums, safeguarding against longevity risk and ensuring steady income flow. These should complement government schemes for holistic security.

Comparative Chart Of Returns And Lock-In Periods

| Benefit | Returns (%) | Lock-in Period | Payout Type | Tax Treatment |

| EPF | ~8.5 | Until retirement/resignation (after 5 years) | Lump sum + interest | Tax-exempt if served >5 years |

| NPS | 9-10 (market) | Until retirement | Lump sum + annuity | Tax benefits under 80CCD(1B), lump sum partially taxable |

| Gratuity | N/A | Minimum 5 years | Lump sum | Tax-free up to INR 20 lakh |

| EPS | Varies | Minimum 10 years | Monthly pension | Taxable as income |

| UPS 2025 | Fixed % | Minimum 10 years | Monthly pension + lump sum | Pension taxable, lump sum tax-free up to limits |

| Insurance | Varies | Varies | Lump sum/Annuity | Tax treatment varies based on product |

Source: ET Money5

Since each option comes with different returns, lock-in rules, and payout types, it is important to know how they are taxed. The next section breaks down the tax implications of various retirement benefits to help you plan smarter.

Tax Implications: Understanding How Retirement Benefits Are Taxed

Taxation plays a key role in helping retirees make the most of their savings. Understanding how each benefit is taxed ensures you do not lose out on hard-earned returns at the time of withdrawal.

1. EPF: Contributions up to INR 1.5 lakh under Section 80C are tax-exempt. Interest earned and withdrawals are also tax-free if the employee completes a continuous service of five years or more.

2. NPS: Offers additional deduction of INR 50,000 under Section 80CCD(1B). At maturity, 60% of corpus used for annuity is taxable as pension income, while 40% lump sum withdrawal is tax-free.

3. Gratuity: Tax-exempt up to INR 20 lakh; any excess is taxable.

4. EPS: Monthly pension is taxable as income.

5. UPS: Pension is taxable, but lump sum benefits are generally tax-free within specified limits6

6. Insurance: Tax benefits vary depending on policy; annuities typically attract income tax on payments received.

Hypothetical example: An employee retiring with INR 40 lakh EPF corpus and INR 10 lakh NPS corpus can expect the EPF lump sum to be tax-free, partial lump sum withdrawal from NPS tax-free, but pension income from the annuity taxable per income slabs. With tax awareness in place, the next section explores how to strengthen retirement planning beyond government benefits for a more robust financial future.

How To Strengthen Retirement Planning Beyond Government Benefits

Government-backed benefits lay the groundwork for retirement security, but relying solely on them can limit long-term growth and inflation protection. To build a stronger, more sustainable retirement plan, employees should complement these schemes with a mix of diverse investments that balance safety, returns, and liquidity.

- Fixed Deposits and Recurring Deposits: Safe instruments offering fixed returns to supplement retirement funds.

- Mutual Funds and SIPs: Equities and balanced funds can build wealth over the long term, suitable for younger employees.

- Grip and Other Structured Products: Tools that provide stable monthly income streams, balancing risk and return.

- Insurance Plans: For longevity risk and financial protection of family.

For instance, a retiree relying only on EPF and EPS may struggle with inflation over time, but combining them with market-linked or income-based investments ensures both growth and financial flexibility throughout retirement.

Conclusion

A secure and comfortable retirement depends on informed financial decisions made early and managed wisely. Traditional schemes like the Employees’ Provident Fund (EPF), Employees’ Pension Scheme (EPS), and Gratuity build a solid base, while flexible options such as the National Pension System (NPS) and Unified Pension Scheme (UPS) 2025 add growth potential. Beyond these, diversifying through fixed deposits, mutual funds, and modern income platforms like Grip can significantly enhance post-retirement security.

Grip investments offer access to alternative, asset-backed opportunities that aim to generate stable monthly income—making them an excellent complement to long-term government savings. By blending safety, returns, and liquidity through such platforms, retirees can achieve financial freedom with confidence. Ultimately, the best retirement plan is one that grows with time, balances risk, and supports a worry-free lifestyle—and Grip Invest provides a reliable way to make that decision smarter and more rewarding.

FAQ’s On Retirement Benefits In India

1. How much should I invest monthly for retirement?

Aim for 20–25% of your income across EPF, NPS, and personal investments. Start early to let compounding work.

2. Are EPF and EPS enough for retirement?

Usually not. They offer stability but may not beat inflation. Combine them with NPS or mutual funds for a stronger income plan.

3. When is the best age to start NPS?

Earlier is better. Starting in your 20s or 30s gives the equity portion more time to grow

References:

1. PFRDA, accessed from: https://www.pfrda.org.in/web/pfrda/schemes/national-pension-system/unified-pension-scheme

2. Money Control,accessed from: https://www.moneycontrol.com/news/business/personal-finance/pgim-retirement-survey-half-of-india-isnt-prepared-financially-for-life-after-work-7688851.html

3. Bajaj Finance, accessed from: https://www.bajajfinserv.in/investments/epfo-minimum-pension-hike

4. Protean Tech, accessed from: https://proteantech.in/articles/unified-pension-scheme-guide-em0142025/

5. ET Money, accessed from: https://www.etmoney.com/learn/nps/epf-vs-nps/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001