SBI Auto Sweep Interest Rate: Features, Benefits And How It Works

Managing idle money in a savings account that can be challenging. While keeping funds accessible is essential, leaving large balances untouched often means earning relatively low returns. This is where the SBI Auto Sweep Facility becomes useful.

The SBI Auto Sweep Facility assists the account holders just to earn higher returns on surplus funds while maintaining the flexibility of a regular savings account. By automatically transferring excess funds into a fixed-deposit-like instrument, the facility allows consumers to optimize their savings without compromising liquidity.

In this paper, we explain the SBI Auto Sweep Interest Rate, how the facility works, its benefits or advantages, and whether it is suitable for your financial goals.

What Is SBI Auto Sweep Facility?

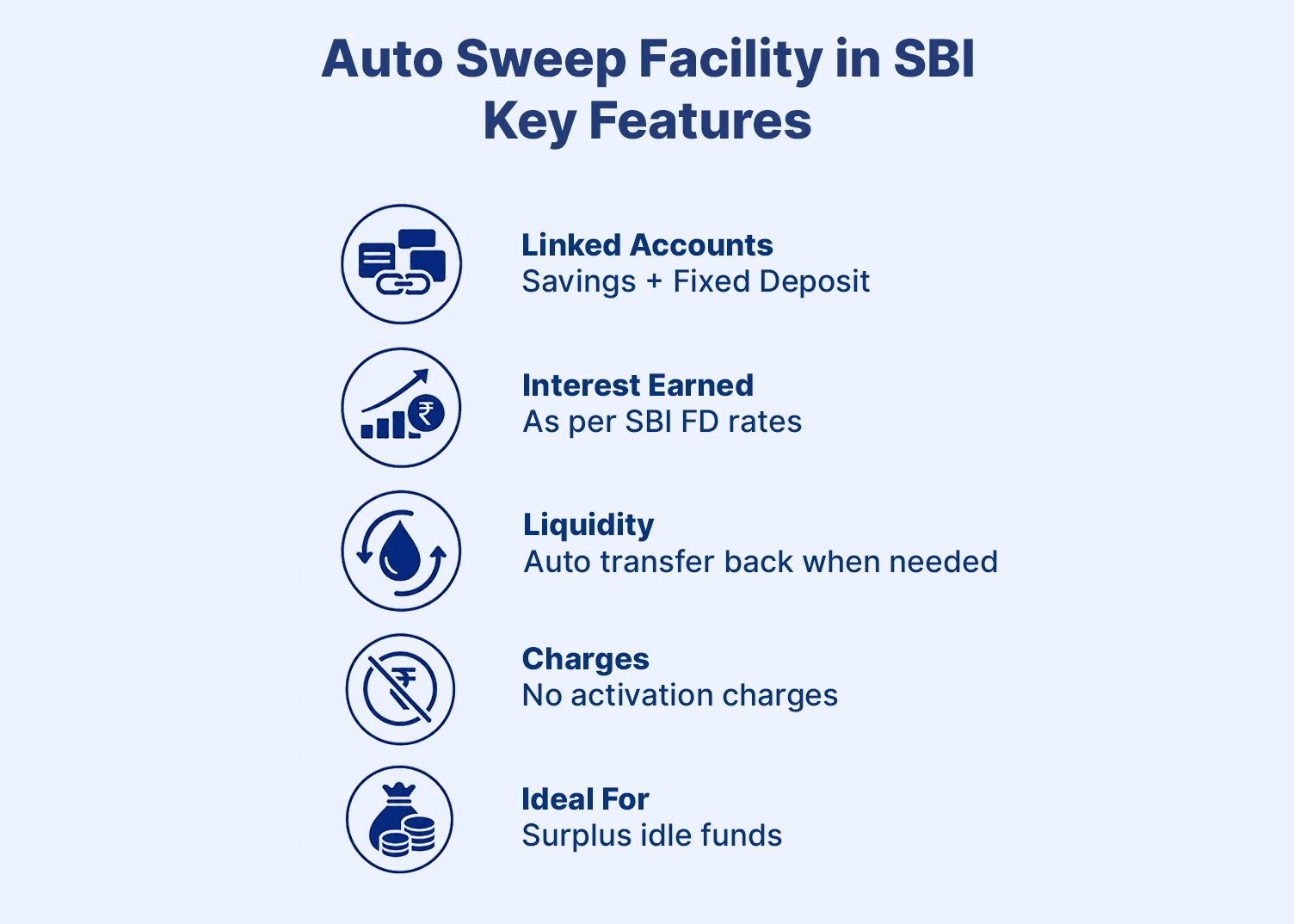

The SBI Auto Sweep Facility is a banking feature that automatically transfers that surplus funds from a savings account into a linked deposit account when the balance exceeds a predefined threshold.1

Instead of keeping excess money idle in a savings account earning standard savings interest, the surplus amount is moved into a deposit that earns a higher interest rate.

The facility is just linked to SBI's Multi Option Deposit (MOD) Scheme, which combines the benefits of a savings account and a fixed deposit.

How the Facility Works?

- A customer maintains a savings account with SBI.

- A threshold balance is defined.

- Any amount exceeding the threshold is automatically transferred to an MOD account.

- The transferred funds earn deposit-based interest.

- If funds are needed later, the required amount is automatically withdrawn from the MOD account.

SBI Auto Sweep Interest Rate

The SBI auto sweep interest rate is usually just linked to the interest rates that are applicable under the SBI Multi Option Deposit Scheme (MODS).

Since MOD deposits function similarly to fixed deposits, the interest earned is significantly higher than the standard SBI savings account interest rate.2

Current Interest Structure

The exact rate varies depending on:

- Deposit tenure

- RBI policy changes

- SBI's prevailing deposit rates

- Customer category (general/senior citizen)

Generally, MOD deposits earn interest comparable to SBI term deposits of similar tenure.

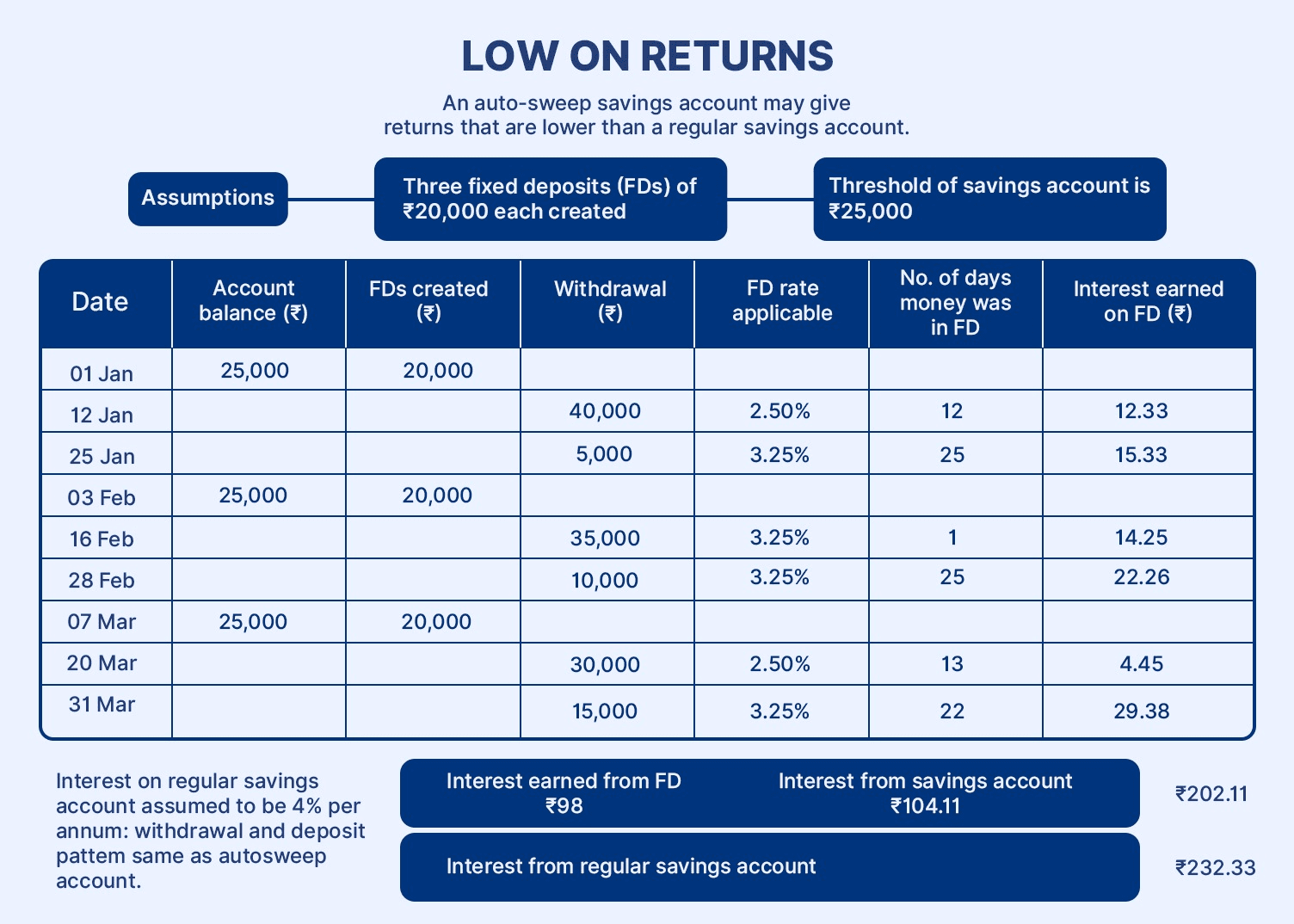

How Returns Differ From A Savings Account?

Feature | SBI Savings Account | SBI Auto Sweep (MOD) |

Liquidity | High | High |

Interest Rate | Standard savings rate | FD-linked rate |

Automatic Management | No | Yes |

Returns Potential | Lower | Higher

|

How SBI Auto Sweep Works

Understanding the sweep-in and sweep-out process is essential before using the facility.

Threshold Balance

A minimum balance threshold is set when activating the facility.

For example:

- Threshold: INR 50,000

- Account Balance: INR 90,000

- Amount Swept: INR 40,000

The excess INR 40,000 automatically moves into the MOD deposit.

Sweep-In Mechanism

When your savings account balance falls below the required amount for a transaction, SBI automatically withdraws funds from the MOD deposit.3

This process is known as sweep-in.

Sweep-Out Mechanism

Whenever surplus funds accumulate above the threshold limit, SBI automatically transfers the excess amount into the MOD deposit.

This process is known as sweep-out.

Partial Withdrawals

One of the biggest advantages of the SBI sweep in the facility is that withdrawals occur only for the amount required.

Unlike traditional fixed deposits that often require breaking the entire FD, MOD deposits support partial withdrawals.

Example

Suppose:

- MOD Deposit: INR 1,00,000

- Required Amount: INR 20,000

Only INR 20,000 is withdrawn while the remaining INR 80,000 continues earning interest.

Benefits of SBI Auto Sweep

1. Higher Returns

The biggest advantage is the opportunity to earn FD-like returns on idle funds without actively creating fixed deposits.4

2. High Liquidity

Funds remain readily available whenever needed.

Unlike conventional investments that may involve lock-in periods, the SBI auto sweep account offers easy access to money.

3. Convenience

The entire process is automated.

There is no need to manually transfer money between savings and fixed deposits.

4. Better Cash Management

The facility helps optimize idle cash while maintaining financial flexibility.

This makes it particularly useful for:

- Salaried professionals

- Freelancers

- Small business owners

- Retirees

5. No Need for Active Monitoring

Customers do not have to constantly track balances and move funds manually.

The bank handles fund allocation automatically.

SBI Auto Sweep vs Fixed Deposit

Although both options help earn higher returns, there are important differences.

Feature | SBI Auto Sweep | Traditional Fixed Deposit |

| Accessibility | Very High | Limited |

| Automatic Transfers | Yes | No |

| Partial Withdrawal | Available | May require FD breakage |

| Returns | FD-linked | FD-linked |

| Liquidity | High | Moderate |

| Convenience | Automated | Manual

|

Source: Razorpay, 5

Which One Is Better?

If you want:

- Easy access to money

- Higher returns than savings accounts

- Automatic fund management

Then the SBI FD linked savings account can be a suitable option.

However, if you are certain you won't need the money for a fixed period, a traditional FD may provide more disciplined long-term savings.

Who Should Invest In SBI Auto Sweep?

The facility is ideal for individuals who maintain large balances in their savings accounts and want to improve returns without sacrificing liquidity.6

Suitable for:

Salaried Employees- Those receiving monthly salaries and maintaining emergency funds.

Business Owners- Individuals managing fluctuating cash flows.

Freelancers-Professionals with irregular income streams.

Senior Citizens-Investors seeking better returns while retaining access to funds.

Emergency Fund Holders-People who want their emergency corpus to remain accessible while earning higher interest.

Things To Consider Before Opting For SBI Auto Sweep

Before activating the facility, keep these points in mind:

- Interest rates may change over time.

- Premature withdrawal rules applicable to MOD deposits may apply.

- Interest earned is taxable according to your income tax slab.

- Threshold limits should be selected carefully based on your cash requirements.

- Compare returns with other investment options before making a decision.

FAQs On SBI Auto Sweep Interest Rate:

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001