Section 80D Of The Income Tax Act: Health Insurance Tax Benefits Explained

Over the last 10 years, the cost of healthcare in India has risen sharply, making health insurance essential for most people to protect their finances. Healthcare inflation has easily surpassed the general inflation rate, and hence any simple medical emergency can eat away a majority of your savings and push you towards bankruptcy.

The governments understand this and also wish to ensure that the public has access to state-of-the-art healthcare.

This is why the Indian Government has provided tax breaks under Section 80D of Income Tax Act. Taxpayers must understand how to claim tax deductions for health insurance premiums, which can reduce their total outstanding tax and provide financial security.

If you are looking to maximize your health insurance tax benefit India, you need to understand how Section 80D can plan your medical insurance tax exemption FY 2026 and onwards.

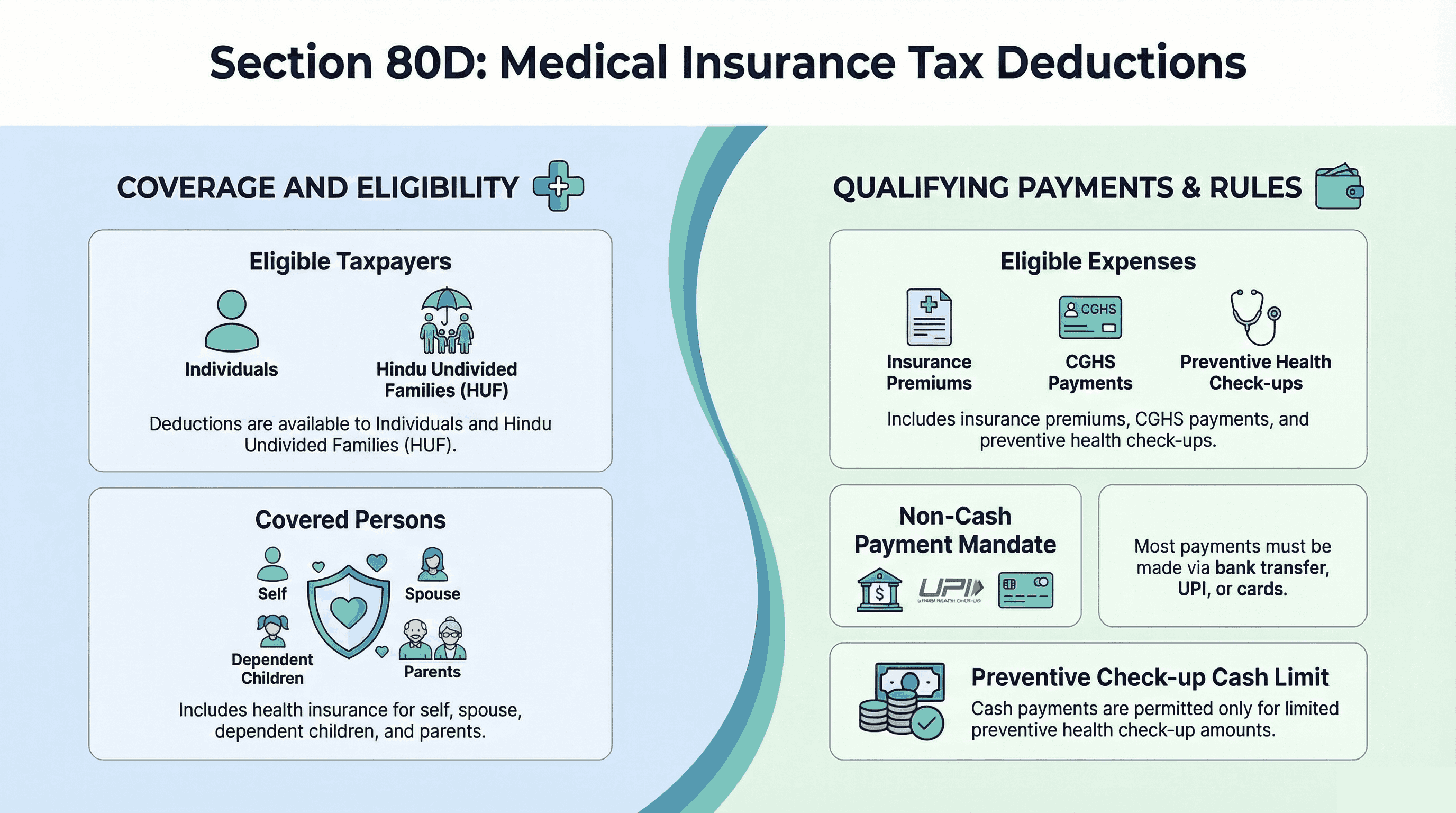

What Is Section 80D?

The Income Tax Act provides for a deduction for certain insurance premiums paid under section 80D for medical insurance. The individual/Hindu Undivided Family will be able to claim a deduction for premiums paid for a healthcare plan covering the following persons: self, spouse, dependent children, and parents.

Any payments made for medical insurance premiums, CGHS, and for preventive health check-ups are eligible for deduction under 80D. The health insurance premium deduction can be claimed only when the payment is made via non-cash methods such as bank transfer, UPI, or debit/credit cards, except for preventive health check-ups, which allow a limited amount of cash payment.

Deduction Limits

The 80D deduction limit is heavily based on the ages of the individual insured members and whether the policy provides coverage for yourself/family or your parents. The limits are subject to periodic revisions, but the current limits are summarised below.

1. Self, Spouse, and Children

An individual can take advantage of a maximum deduction amounting to INR 25,000 for premiums paid for themselves, their spouse, and any dependent children for the entire financial year. If the individual taxpayer is a senior citizen, e.g., aged 60 and over, the maximum deduction is increased to INR 50,000.

2. Parents

The health insurance of the parent or parents can be included in the additional deduction. If the parents are less than 60 years of age, the limit is INR 25,000. If one or both parents are over 60 years of age, the limit would be raised to INR 50,000 under the Senior Citizen Rule in Section 80D of the Income Tax Act.

3. Senior Citizens Without Insurance

Medical expenses up to INR 50,000 can be deemed as a deduction for the Section 80D senior citizen limit if there is no premium paid for them.

4. Deduction Limits by Age Category

| Category | Deduction for Self & Family | Deduction for Parents | Maximum Deduction |

Self & Family (below 60 years) | INR 25,000

| - | INR 25,000 |

Self & Family + Parents (all of them below 60 years) | INR 25,000

| INR 25,000

| INR 50,000 |

Self & Family (below 60 years) + Parents (above 60 years) | 25,000 | 50,000 | INR 75,000 |

Self & Family + Parents (above 60 years) | INR 50,000

| INR 50,000

| INR 1,00,000 |

| Preventive health checkup (included in above) | - | - | INR 5,000 |

Source: ClearTax1

Preventive Health Checkup Benefit

The section 80D preventive health checkup allows you to receive a tax deduction of up to INR 5,000 per year for preventive health checkups.

The amount of INR 5,000 is not an additional deduction under Section 80D; it is included under the overall limit of Section 80D.

The benefit is that you can pay for your preventive health checkups in cash rather than only through health insurance.

Preventive health checkups may include routine blood tests, diabetes screening, cholesterol screening, and annual health packages. Many health insurance carriers also bundle preventive health services into their policies to help maximize your tax benefits.

Section 80D For Parents And HUF

The provision provided by Section 80D for parents is especially valuable in the Indian context of an aging demographic. Given that medical inflation rates are approximately 12-14% per annum, insuring parents can have a profound effect on the amount of tax relief you can achieve.

Also, the tax-saving benefit from the Section 80D HUF claim can be obtained by deducting premiums paid on behalf of the HUF members. The deduction limits available to HUFs correspond with those available to individuals.

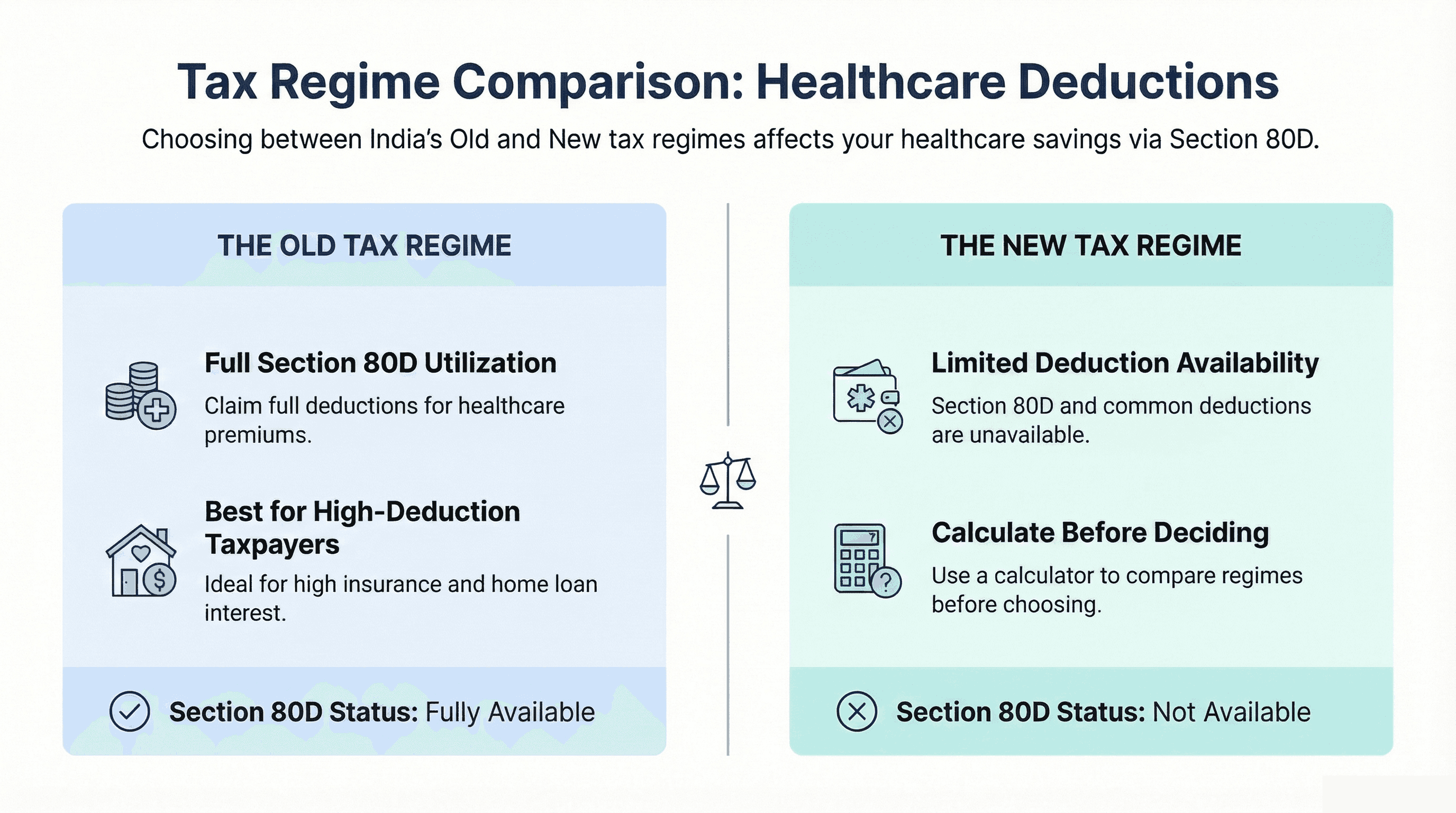

Old Vs New Tax Regime Impact

Today, the application of Section 80D new tax regime is critical for taxpayers to understand. Under the old tax regime, all taxpayers were able to use the full amount under Section 80D. However, under the new tax regime introduced in recent years, most deductions, including Section 80D, are not available.

Regime choices are key variables in tax planning. All financial planners generally suggest comparing both regimes with a health insurance tax saving calculator before making the choice. Generally, taxpayers with high insurance premiums, home loan interest, and other deductions tend to benefit more from the previous tax regime.

Section 80D Vs 80DDB Difference

Most taxpayers are confused about the differences between sections 80D and 80DDB of the tax regulations. Section 80D applies to deductions for health insurance premiums and preventive check-ups, while Section 80DDB provides deductions for treatment of certain specified critical illnesses such as cancer, chronic kidney failure, and Parkinson's Disease.

Being aware of this 80D vs 80DDB difference can help ensure that taxpayers do not miss out on legitimate tax deductions available to them.

Payment Rules And Compliance

You may be wondering, how 80D cash payment allowed? The law states that only insurance premiums that were paid non-cash qualify under this rule. Only considered for cash payment within the INR 5,000 limit of preventive health check-up contributions. All taxpayers should keep premium receipts, policy documents, and proof of payment because, to provide evidence during an income tax audit, all three are necessary.

FAQs

1. What is the 80D deduction limit?

Under Section 80D, the maximum deduction is between INR 25,000 and INR 50,000, depending on your age, but you can also receive an additional deduction for your parents' insurance premiums.

2. Can I claim parents' insurance?

Yes, premiums paid for your parents' insurance qualify for a separate deduction under Section 80D even if your parent does not financially depend on you.

3. Is a preventive checkup included?

Yes, the portion of the Section 80D limit that is allocated to preventive check-ups excludes your overall deduction of INR 5,000 for preventive check-ups, and can be paid in cash.

Reference:

1. ClearTax, accessed from: https://cleartax.in/s/medical-insurance

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001