Section 24B Of Income Tax Act: Home Loan Interest Deduction Explained

Buying a home is one of the most significant financial decisions an Indian taxpayer will ever make. With rising property prices, most homebuyers rely on home loans to fund their purchase. The good news is that the Income Tax Act, 1961 offers meaningful relief in this regard. Section 24B of the Income Tax Act allows taxpayers to claim a deduction on the interest paid on a home loan, reducing their overall tax liability.

Whether you own a property you live in or one that you have rented out, Section 24B has specific provisions for both scenarios. Understanding how this deduction works, what the limits are, and the conditions attached can help you plan your taxes more effectively and ensure you are not leaving money on the table during ITR filing.

What Is Section 24B?

Section 24B falls under the head "Income from House Property" in the Income Tax Act. It specifically deals with deductions that can be claimed against the income earned from a property, or in the case of a self-occupied property, against the notional value.

The section permits deductions under two categories.

The first is a standard deduction of 30% of the Net Annual Value (NAV) of the property, applicable primarily to let-out properties. The second, and more commonly known provision, is the deduction on interest payable on a loan taken for the purpose of purchasing, constructing, repairing, or reconstructing a house property.

This interest deduction under Section 24B is separate and distinct from the principal repayment deduction available under Section 80C. It is also important to note that Section 24B covers only interest, not the principal component of the EMI.

Deduction Limits Under Section 24B

The deduction amount depends on whether the property is self-occupied or let-out.

1. Self-Occupied Property

For a property that the taxpayer occupies for their own residential use (self-occupied property), the maximum deduction on home loan interest allowed under Section 24B is INR 2,00,000 per financial year.

However, this limit applies only if the loan was taken on or after April 1, 1999, and the construction or acquisition of the property is completed within 5 years from the end of the financial year in which the loan was taken. If these conditions are not met, the deduction is restricted to just INR 30,000 per year.

For a self-occupied property, the Net Annual Value is considered to be NIL. Therefore, claiming the interest deduction can result in a loss under the head "Income from House Property," which can be set off against other income heads such as salary, up to INR 2,00,000 in a year.

2. Let-Out Property

For a property that is rented out (let-out property), there is no upper cap on the interest deduction that can be claimed under Section 24B. The entire interest paid on the home loan for a let-out property is eligible for deduction. This is one of the most significant benefits available to property investors.

However, from the Assessment Year 2018-19 onwards, the loss from house property that can be set off against other income in the same year is capped at INR 2,00,000. Any excess loss must be carried forward for up to 8 assessment years and set off only against income from house property in subsequent years.

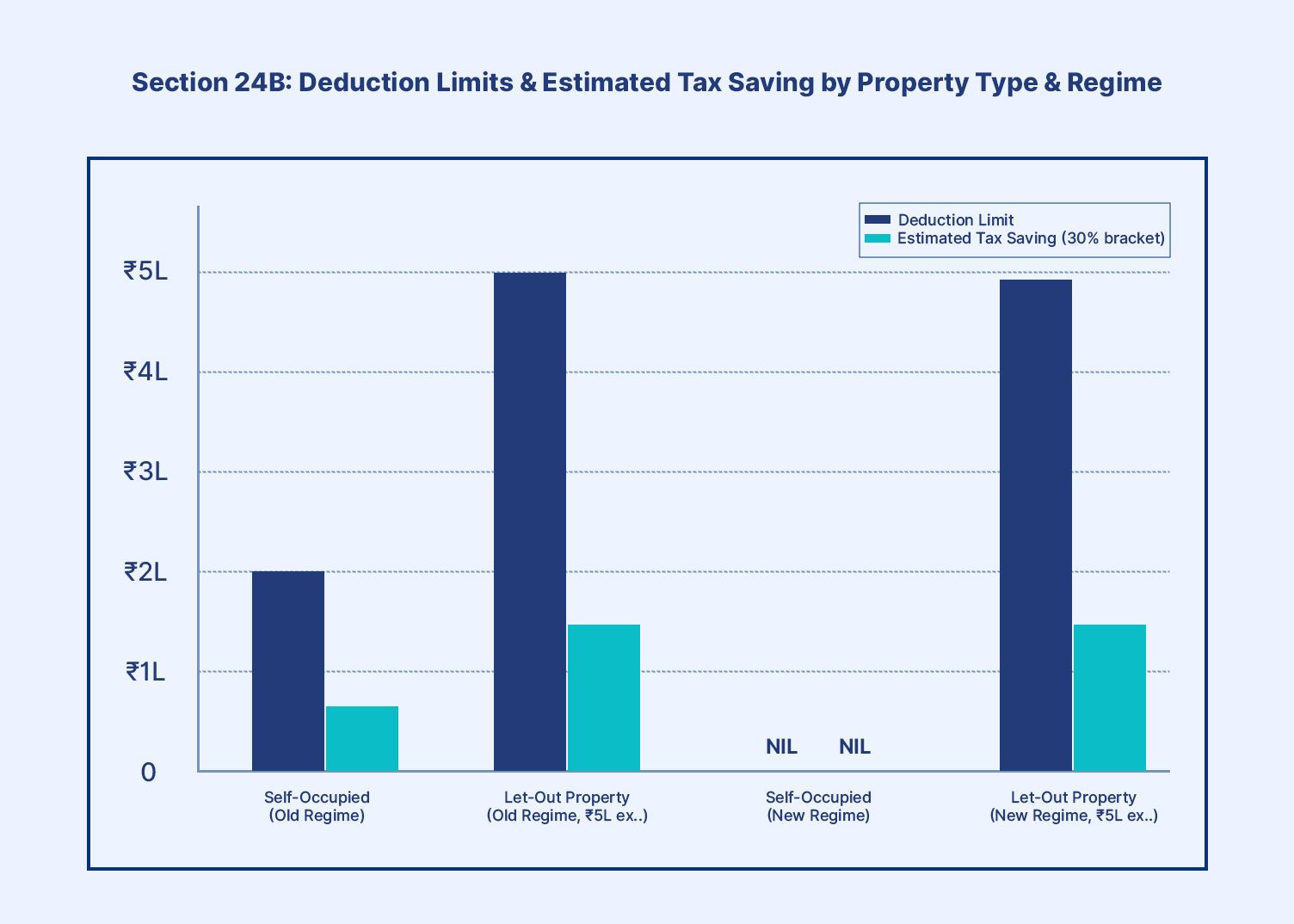

3. Deduction Limits & Tax Savings at a Glance

Figure 1: Section 24B deduction limits and estimated tax savings across property types and tax regimes (tax saving at 30% bracket; let-out based on INR 5L interest example)

Comparison Table: Self-Occupied vs. Let-Out Property

| Parameter | Self-Occupied Property | Let-Out Property |

| Deduction Limit on Interest | Up to INR 2,00,000/year | No upper limit (full interest) |

| Net Annual Value (NAV) | NIL | Actual rent received |

| Standard Deduction (30%) | Not applicable | Applicable on NAV |

| Loss Set-Off Limit | INR 2,00,000/year against other income | INR 2,00,000/year; excess carried forward |

| Pre-Construction Interest | Claimable in 5 equal instalments | Claimable in 5 equal instalments |

| New Tax Regime Eligibility | Not available | Available (no cap) |

Conditions to Claim Deduction Under Section 24B

Not every home loan borrower automatically qualifies for the maximum deduction. The following conditions must be satisfied:

1. Loan Purpose: The loan must have been taken specifically for purchasing, constructing, repairing, renewing, or reconstructing a house property.

2. Completion Timeline: For self-occupied properties, construction must be completed within 5 years from the end of the financial year in which the loan was sanctioned. Failure to meet this deadline reduces the deduction limit from INR 2,00,000 to INR 30,000.

3. Certificate Requirement: You must obtain a home loan interest certificate from your lender. This document specifying the interest and principal paid during the financial year is mandatory during ITR filing.

4. Loan from Recognized Sources: The loan should ideally be from a bank, housing finance company, or other recognized financial institution. Loans from family members may be eligible, but the lender must provide a certificate confirming the interest payment.

5. Property Ownership: The deduction can only be claimed by the owner. If you are a co-owner on a joint home loan, you can each claim the deduction proportional to your share in the loan.

6. Pre-Construction Interest: Interest paid from the date of loan disbursal up to March 31 before the year of possession is eligible for deduction in five equal annual instalments beginning from the year of possession.

Section 24B And The New Tax Regime

With the introduction of the New Tax Regime under Section 115BAC, which has been the default regime since Assessment Year 2024-25, taxpayers must carefully evaluate how their regime choice affects their Section 24B deductions.

Under the New Tax Regime, the deduction under Section 24B for a self-occupied property is not available. Taxpayers who opt for the new regime cannot claim the INR 2,00,000 interest deduction on their self-occupied home loan.

However, there is an important exception for let-out properties. Even under the New Tax Regime, taxpayers can claim the interest deduction on loans taken for a rented-out property. This is because the rental income is taxable under the new regime as well, and the deduction is treated as a computation adjustment. The same 30% standard deduction on NAV and full interest deduction rules continue to apply for let-out properties.

If you have a self-occupied home and a significant home loan, opting for the old tax regime may result in greater tax savings due to the availability of the Section 24B deduction combined with other exemptions such as HRA and Section 80C benefits.

Conclusion

Section 24B of the Income Tax Act, 1961 helps home loan borrowers reduce tax liability by allowing interest deductions — up to INR 2,00,000 for self-occupied properties and unlimited interest for let-out properties (subject to set-off rules). Your tax savings depend on property type, completion timeline, and whether you choose the old or new tax regime. Proper planning ensures you maximise benefits. Alongside real estate tax savings, diversifying into structured income options through platforms like Grip Invest can further strengthen your overall financial strategy.

FAQs

1. What is the limit under Section 24B?

The deduction limit under Section 24B depends on the type of property. For a self-occupied property, the maximum interest deduction is INR 2,00,000 per financial year. If the construction is not completed within 5 years of the loan being taken, this limit drops to INR 30,000. For a let-out (rented) property, there is no upper limit — the entire interest paid on the home loan is deductible.

2. Can I claim pre-construction interest under Section 24B?

Yes, pre-construction interest is eligible for deduction under Section 24B. The total interest paid from the date of the first loan disbursement until March 31 of the year immediately preceding the year of possession can be deducted in five equal annual instalments starting from the year the property is ready. This deduction is available for both self-occupied and let-out properties.

3. Is Section 24B available under the new tax regime?

Section 24B is partially available under the new tax regime. Taxpayers cannot claim the INR 2,00,000 deduction on a self-occupied property if they have opted for the new regime. However, for a let-out property, the interest deduction continues to be available without any ceiling, as it is treated as a computation against taxable rental income

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001