Best Short-Term Investment Plans For 3 Months In India

Where To Park Money For Just 3 Months

A financial objective does not necessarily require a long-term commitment. You may have extra money that you would like to invest for a very short term of only three months (or even less). A typical example is money that you have saved in preparation for future spending, or maybe you received an extra income that you are not going to use immediately.

In such cases, the intentions are not aimed at wealth accumulation. Instead, capital protection, liquidity, and guaranteed returns become prominent. In comparison to long-term investments, short term investment plans for 3 months must avoid risks in the market while ensuring your funds are easily retrievable when required.

Other short term investment plans for 3 months that investors can choose from in India include government-backed options. Additionally, with the platform Grip, investors can access investments which were previously inaccessible to them. This includes assets like short-term corporate bonds and T-Bills.

What To Look For In A 3 Month Investment

Before making a selection from the different safe 3 month investment options India, it is essential that one appreciates what really matters with regard to such a short period.

Capital Protection

Given the short three-month period available, there is little scope to absorb any volatility. The priority is the protection of the principal. Any instruments that are susceptible to equity market volatilities or long-term interest rate volatilities are not suitable.

Easy Exit and Liquidity

Your investment should allow quick redemption of the funds with no charges to the investor. This is especially the case when emergencies arise and the short term safe investments have to be redeemed within specific timelines.

Reliable Returns

For smaller periods, the effect of compounding is negligible. Therefore, stability over returns is more preferable.

For instance, assume that Riya has INR 2,00,000, which she wants to invest as a down payment for a house in the next three months. Instead of keeping it in a savings account, which may offer a return of approximately 2.5 to 3% per annum, she needs to find a low-risk investment that might provide a slightly higher return without tying up the capital.

Most Popular Short-Term Investment Avenues In India

1. Corporate Bonds with 3 Months or Less Tenure (Available on Grip Marketplace)

The short-term bonds issued by high-quality companies are a very attractive investment option for those seeking higher returns than conventional savings accounts.

- Tenure: As low as 60-90 days

- Risk Profile: Less than equities but sensitive to credit risk

A case in point would be platforms like Grip Marketplace, where such relationships are carefully curated to include information on the issuers, maturities, and expected yields of the bonds. Since the remaining maturity of these bonds is short, the risk of interest rate variability does not have a significant effect

For example, an investment of INR 1,00,000 in a 90-day corporate bond bearing an annualized rate of 9% could fetch around INR 2,200-2,300.

2. Government Bonds and T-Bills (Treasury Bills) – Available on GRIP

Treasury Bills are one of the safest short-term investment options in India, guaranteed by the Government of India, and are issued for 3 months.

- Tenure: 91 days, 182 days, & 364 days

- Returns: Typically in line with the prevailing rate of interest (approximating 6.5%—7.2% in recent

- Liquidity: High, with predictable maturity payouts

For conservative investors who value safety over returns, T-Bills are the best option. Such investments through platforms like Grip make it easy to invest in T-Bills through auctions conducted by the RBI.

3. Saving Accounts & Sweep Fixed Deposits

Conventional savings accounts are the most fluid investment, but the yield rates are low.

- Returns: 2.5-4

- Liquidity: Immediate Access

- Best suited for: Emergency funds where same-day liquidity is required.

Sweep-in/Flexi FDs: This is a system in which any excess amount is systematically swept into a Fixed Deposit while maintaining liquidity. Although the interest rates increase by a little, maybe around 6 to 7%, early withdrawals might affect the rates

4. Liquid Mutual Funds

Liquidity funds have a maturity period of up to 91 days and invest in money market instruments. They are also one of the very liquid investment options.

- Returns: Historically 5-7

- Risk: Low, but not zero

- Liquidity: T+1 redemption (Next Business Day)

Based on the trend in AMFI, liquid funds have delivered stable returns with very low volatility compared to equity and debt funds with a higher tenure.

5. Ultra Short Duration Instruments

Ultra Short Duration Funds & Instruments invest in slightly longer maturity debt than Liquid Funds.

- Returns: Slightly higher than a liquid fund

- Risk: Moderate interest rate and credit risk

- Applicability: More suited for investment time frames ranging from 3-6 months, as opposed to

However, these funding arrangements might not be the best options if high capital certainty on a certain date is a prime consideration.

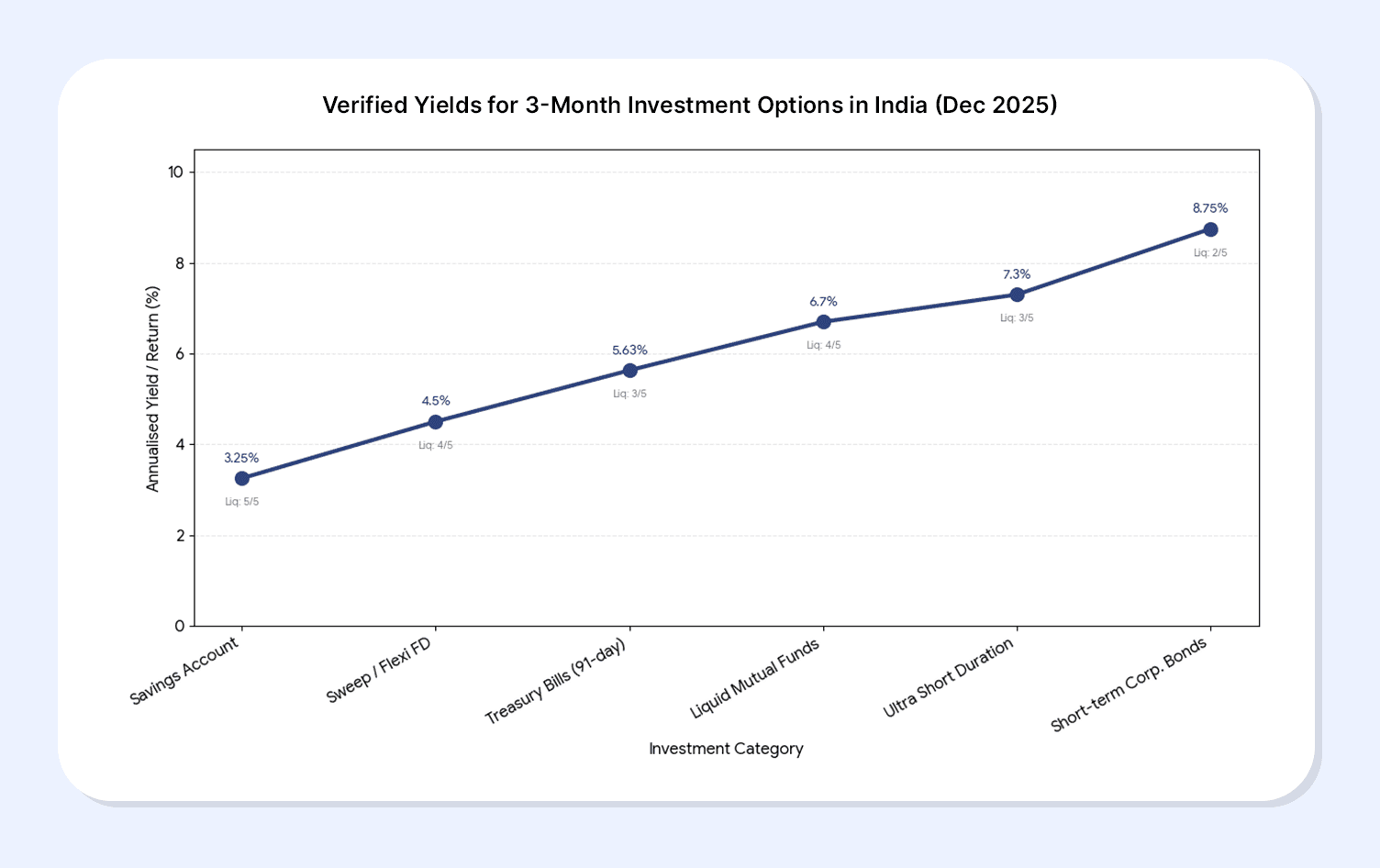

Figure 1.0: Yields for 3-Month Investments in India (Self-Generated)

Source: ET money1

Selecting The Appropriate Option Depending On Your Objective

1. Parking Temporary Surplus

If you are temporarily holding surplus funds (say, while waiting for the next investment), corporate short-term bonds or liquid funds may be utilized to maximize profits.

2. Planned Expenses in 3 Months

In cases where expenses are certain, such as payment of taxes, rent, or education expenses, T-Bills or bonds with short tenures are an investment option

3. Emergency Buffer

In emergency savings, liquidity comes first. Mixing savings accounts and liquid funds provides fast access with some yield improvement.

Key Principle: Refrain from taking unwanted risks over short time horizons. The strategy of pursuing higher yields with lower-rated stocks or equities may prove counterproductive over shorter time horizons.

Conclusion

When the investment horizon is as short as three months, the goal is simple: protect your capital, keep liquidity intact, and earn a reasonable return without unnecessary risk. Chasing high yields or market-linked products rarely makes sense over such a brief period. Instead, instruments like Treasury Bills, short-term corporate bonds, liquid funds, and savings-based options align better with short-term needs such as planned expenses or temporary surplus parking.

Platforms like Grip Invest make this process easier by offering access to carefully curated short-term bonds and government-backed instruments, helping investors move beyond idle savings while still staying within a low-risk framework. The key is to match the product with your purpose and timeline, not the headline return.

FAQs

1. Which investment would be good for 3 months?

The choice between them is dependent on your priorities. For your security, T-Bills would be the best. For more risk-averse returns, corporate bonds through Grip's services would be ideal. For liquidity, a savings account would work.

2. Are short term bonds safe for 3 months?

High-grade, short-term bonds have lower risk than long-term bonds. Yet they do have a specific credit risk associated with the issuer, which is why due diligence is necessary for the platform.

3. Can I lose money in short-term investments?

Yes, but in very rare cases. Smaller fluctuations in the NAV are expected in debt mutual funds, and there may be default risk associated with low-rated instruments.

References:

1. SBI, accessed from: https://sbi.co.in/web/interest-rates/savings-bank-deposits

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001