Systematic Deposit Plan (SDP): A Smarter Way To Build Savings In 2026

With significant economic growth, the investment landscape in India is maturing effectively. Although the modern and high-growth investment assets are rising in popularity, secure investments like fixed deposits still maintain a strong hold amid the Indian investor class. However, fixed deposits often lack flexibility, with stringent investment, withdrawal and other norms.

A Systematic Deposit Plan is a unique solution to the flexibility constraints of a fixed deposit, as it creates a hybrid of SIPs and FDs. This blog aims to decode the SDP meaning so that investors can choose the best SDP providers in India.

What Is a Systematic Deposit Plan (SDP)?

A Systematic Deposit Plan combines the features of various key investment avenues, such as FDs, recurring deposits, and SIPs. In the case of an SDP, an investor invests a fixed sum monthly into the asset, similar to a recurring deposit and an SIP. However, unlike a recurring deposit, each monthly instalment creates a fresh FD at the prevailing rate.

The comprehensive SDP Eligibility Criteria India and its features discussed below can crystallise the understanding of the SDP definition.

- Instalments: Investors invest in monthly instalments, unlike the lump-sum investment requirements of FDs.

- Fixed Deposit: Each instalment does not feed into the same funds but creates fresh FDs at prevailing rates.

- Lock-In: Each deposit functions like a unique and new FD that has its own lock-in and maturity.

Understanding the working method of the best systematic deposit plan in India can enhance the understanding of this asset, resulting in informed investing.

How Does SDP Work in India?

There are two popular categories of systematic deposit plan. These categories differ primarily based on their maturity.

1. Monthly Maturity Scheme: Each FD matures after its own unique tenure at a distinct maturity date. Suppose Mr A picked a tenure of 1 year for 5 SDP instalments. Beginning from 1 March 2025, the table below shows his maturity timeline.

| Instalment | Tenure (Years) | Instalment Payment Date | Deposit Maturity Date |

| SDP 1 | 1 | 1 March 2025 | 1 March 2026 |

| SDP 2 | 1 | 1 April 2025 | 1 April 2026 |

| SDP 3 | 1 | 1 May 2025 | 1 May 2026 |

| SDP 4 | 1 | 1 June 2025 | 1 June 2026 |

| SDP 5 | 1 | 1 July 2025 | 1 July 2026 |

2. Single Maturity Scheme: Under this scheme, each FD matures at the same maturity date, resulting in a differentiating tenure. For instance, if Mr A had invested in a Single Maturity Scheme SDP for a period of 1 year, starting on 1 March 2025, the table below shows his timeline.

| Instalment | Tenure | Instalment Payment Date | Deposit Maturity Date |

| SDP 1 | 1 Year | 1 March 2025 | 1 March 2026 |

| SDP 2 | 11 Months | 1 April 2025 | 1 March 2026 |

| SDP 3 | 10 Months | 1 May 2025 | 1 March 2026 |

| SDP 4 | 9 Months | 1 June 2025 | 1 March 2026 |

| SDP 5 | 8 Months | 1 July 2025 | 1 March 2026 |

Now, based on this information, let us take another illustrative scenario to understand how SDPs work. This can aid in comparatively analysing the advantages of SDP over FD, whilst clarifying the SDP vs recurring deposit differences.

Imagine Mr A chose to invest in a Monthly Maturity Scheme SDP, while his brother Mr K chose a regular FD. The table below shows some details of their investment.

Mr A | Mr K | ||

| SDP instalment | INR 10,000 | Principal | INR 50,000 |

| Tenure | 1 Year | Tenure | 1 Year |

| Total Investment Amount | INR 50,000 | ||

| Number of SDPs | 5 | ||

| Therefore, total investment in both cases remains the same at INR 50,000. | |||

Now, as the interest rate fluctuates, the FD rates of Mr A will differ for each SDP FD. However, Mr K will have a consistent FD rate. The table below shows an assumed interest rate table for 12 months.

Mr A | Mr K | ||

| SDP 1 | 7% | FD | 7% |

| SDP 2 | 6.5% | ||

| SDP 3 | 7% | ||

| SDP 4 | 7.5% | ||

| SDP 5 | 8% | ||

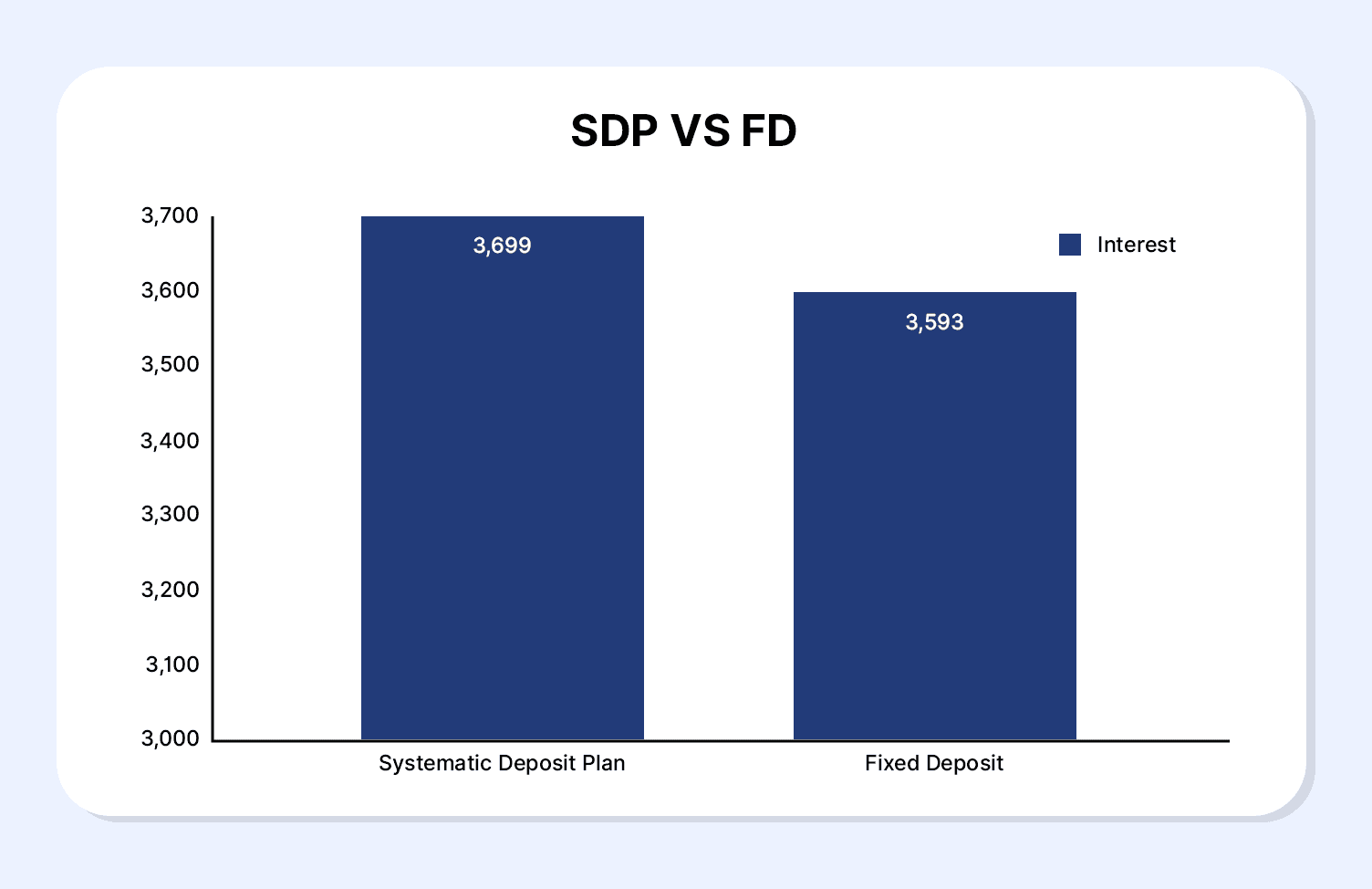

Now, based on the information, Mr A will earn an interest of INR 3,699 after the maturity of his entire SDP investment, while Mr K will earn INR 3,593. The graph below shows the SDP vs FD return comparison of Mr K and Mr A.

The systematic deposit plan calculator can help analyse the returns of different SDP plans and choose the one that best suits our needs. However, not only the return, but also several other advantages of the asset make it effective.

Systematic Deposit Plan Benefits

Several SDP schemes are making their debut in the investment landscape. The Systematic Deposit Plan Bajaj Finance, Bank of Baroda SDP, etc., are some of them. Discussed below are the features that give rise to the advantages of SDPs.

1. Flexibility: An investor no longer requires a lump-sum investment to benefit from consistent, stable returns of fixed deposits. Investors can start investing with limited funds.

2. Liquidity and Tenure: Moreover, in the case of MMS SDP, investors can benefit from varying withdrawal dates. This increases the liquidity of SDP investment.

3. SDP Interest Rates 2025: The interest rate of SDP combines the interest benefit of both FDs and SIPs. On one hand, each SDP FD incurs fixed interest, devoid of market fluctuations. However, on the other hand, each new FD created is created at the prevalent interest rate. Therefore, an investor can benefit from rising FD rates as well.

4. SDP VS SIP Comparison: Unlike mutual funds, the SDP are not a market-linked asset. Therefore, it is suitable for conservative, risk-averse investors who require capital preservation.

Along with these benefits, the SDP has certain limitations too.

Limitations Of SDPs

Discussed below are the limitations of the Systematic Deposit Plan.

1. Adverse Interest Rate Fluctuations: In case the FD interest rate falls, the new FD created under SDP will have the current diminished interest rate.

2. Withdrawal: While distinct maturity improves liquidity, the withdrawal of an FD created remains restricted.

3. Penal Interest: Some providers might levy a penalty on late payment of an instalment.

4. Inflation: The rising inflation may restrict the efficiency of the conservative fixed FD rates.

Therefore, to benefit from SDP advantages, whilst mitigating its limitations, an investor can opt for diversification into FD alternatives in India.

Adding Fixed Income for Better Yield

The fixed deposit rates of SDPs can lose their efficiency due to inflation. For instance, a 3% inflation can reduce the real interest rate of a 7% FD to 4%. Therefore, diversification into other assets is important to maintain portfolio growth.

Grip offers various high-yield FDs with 8% to 10% return. Moreover, the corporate bonds on the platform give access to fixed income and inflation cover with up to 14% YTM.

Explore the diverse range of assets with the SEBI-approved platform Grip.

Visit Grip Today!

FAQs On SDP

1. What is an SDP and how does it work?

A Systematic Deposit Plan allows investors to invest a fixed instalment monthly over a period of time. Each instalment creates a new FD with its unique tenure and interest.

2. Is SDP better than FD?

SDP can be better than an FD if the concerned investor prioritises taking advantage of FD rate fluctuations over a fixed FD rate.

3. Who should choose an SDP?

It is suitable for investors who want fixed returns like fixed deposits but aspire for greater flexibility.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001