Bank Of Baroda FD Rates 2026: Updated Interest Rates, Tenure Options, And Smarter Alternatives

Fixed Deposits make an integral part of an individual’s portfolio. Besides giving a low-risk, consistent return, fixed deposits add diversification and balance to a portfolio. Hence, if you are looking to attain a long-term financial goal or have an emergency fund, using a fixed deposit as an investment asset would be an excellent idea. There are numerous public and private sector banks offering fixed deposit options for different age groups (of customers) and tenures of fixed deposits.

Bank of Baroda also offers fixed deposits to its customers. As one of the largest public sector banks, BOB currently manages total deposits (including Fs) of approximately INR 14.90 lakh crores across the country. If you are looking forward to opening an FD with Bank of Baroda, let us walk you through the updated interest rates (after the RBI repo rate changes), different tenure options for customers, and what other alternatives you can explore in place of conventional fixed deposits from Bank of Baroda.

Bank Of Baroda FD Rates (2025-26 Update)

The latest bob fd interest rates today provide a mix of short-term and long-term options, catering to both regular depositors and retirees. There has been a recent update in the rate of deposits, due to the monetary policy changes as introduced by the RBI in September 2025. Here are the FD interest rates for deposits under INR 3 crore for different categories of customers and tenures:

Tenor | Residents / General Public | Resident Indian Senior Citizen | Resident Super Senior Citizen |

7 days to 14 days | 3.50% | 4.00% | 4.00% |

15 days to 45 days | 3.50% | 4.00% | 4.00% |

46 days to 90 days | 5.00% | 5.50% | 5.50% |

91 days to 180 days | 5.00% | 5.50% | 5.50% |

181 days to 210 days | 5.50% | 6.00% | 6.00% |

211 days to 270 days | 5.75% | 6.25% | 6.25% |

271 days and above and less than 1 year | 6.00% | 6.50% | 6.50% |

1 year | 6.25% | 6.75% | 6.75% |

Above 1 year to 400 days | 6.50% | 7.00% | 7.10% |

Above 400 days and upto 2 years (except 444 days) | 6.50% | 7.00% | 7.10% |

Above 2 years and upto 3 years | 6.50% | 7.00% | 7.10% |

Above 3 years and upto 5 years | 6.40% | 7.00% | 7.10% |

Above 5 years and upto 10 years | 6.00% | 7.00% | 7.00% |

Above 10 years (MACAD only) | 5.50% | 6.00% | 6.00% |

BoB Square Drive Deposit Scheme (444 days) | 6.60% | 7.10% | 7.20% |

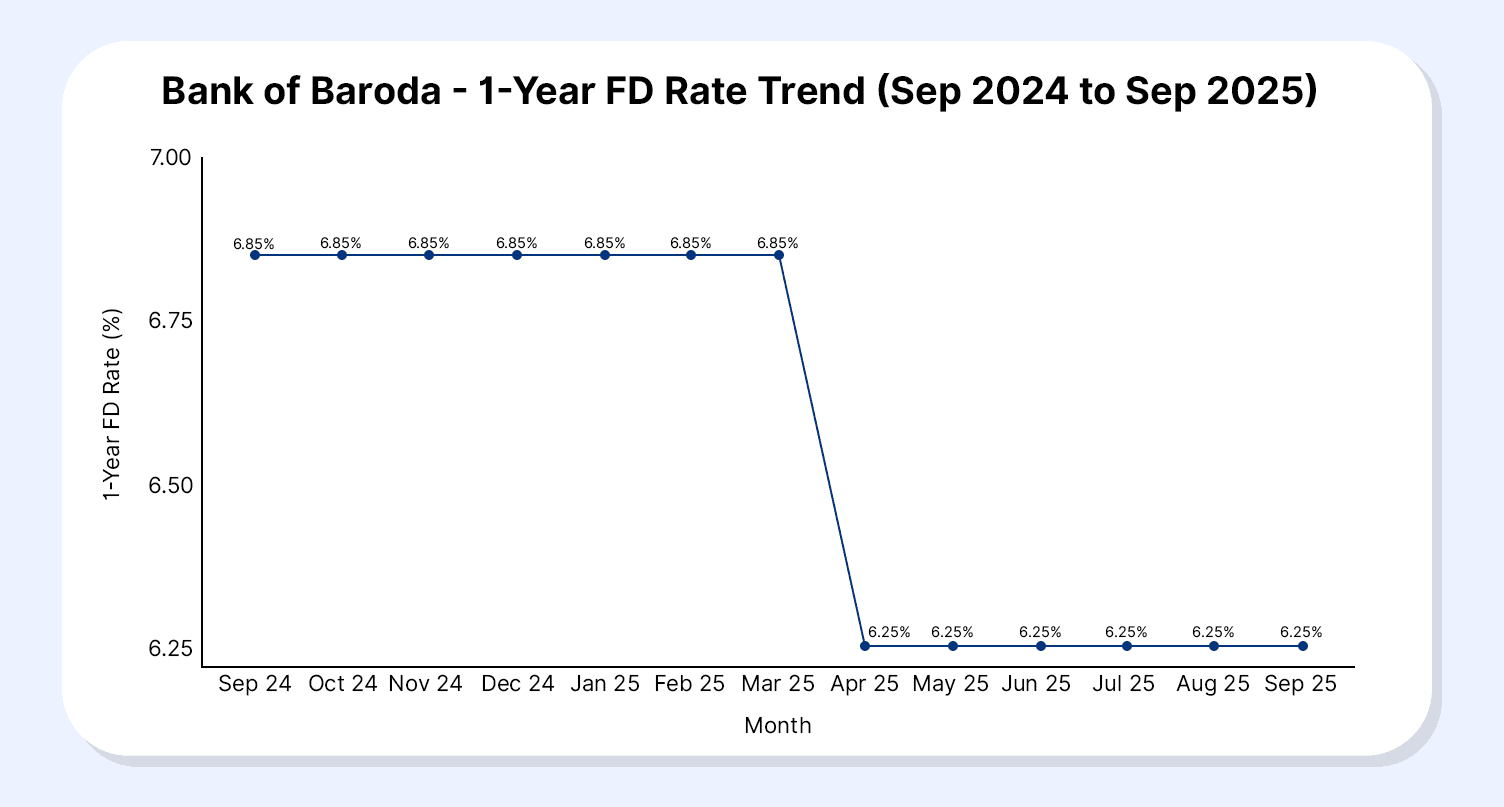

Here is how the rate of interest on FDs has changed in the past twelve months (for general customers, deposits under INR 3 crore).

Figure 1.0: BOB Fixed Interest Rates

The interest rate declined after the RBI’s monetary policy announcement earlier in the year. The bank, however, did not make any changes after the recent RBI repo rate changes.

Also Read: TDS On FD Interest Explained: Rules, Rates, And How To Avoid Excess Tax

Key Features Of Bank Of Baroda FDs

Here are the key features of Bank of Baroda FDs

- Wide tenure choices ranging from 7 days to 10 years, suitable for both short-term and long-term financial goals.

- Flexible Bank of Baroda FD payout options, including monthly, quarterly, semi-annual, and annual interest payments.

- Nomination facility available for all depositors, ensuring smooth transfer of funds.

- Option to avail overdraft/loan against FD for liquidity without breaking the deposit.

- Convenient online opening, monitoring, and tracking through digital banking platforms.

- Hassle-free renewal process supported by competitive bob fd renewal rates when extending the deposit term.

- Premature closure is allowed but subject to applicable bob fd premature withdrawal charges and adjusted interest rates.

- Senior and super-senior citizens receive higher interest benefits across multiple tenures.

Taxation And Real Returns

Interest earned on Bank of Baroda FDs is taxable as per your income slab, with TDS (10%) applicable once annual interest crosses the prescribed limit. Investors opting for long-term tax benefits can explore the 5-year deposit, where BOB tax saver fd rates apply. To estimate post-tax maturity values accurately, the online BOB FD calculator is useful. However, real returns may fall once inflation is accounted for, making it essential to compare nominal gains with actual purchasing power.

Also Read: Post Office 1 Year FD Interest Rate 2026

FD Alternatives For Higher Yield

While Bank of Baroda fixed deposit interest 2026 offers stability and predictable returns, many investors also explore corporate fixed deposits to enhance yield without taking equity market exposure. Corporate FDs are offered by reputed NBFCs and corporates, and they typically provide higher interest rates than traditional bank deposits because the issuer is not a bank and therefore offers an additional return premium for the investor.

Corporate FDs available on platforms like Grip Invest go through a detailed screening and feature issuers with consistent financial performance, strong repayment history, and clear cash flow visibility. These deposits offer flexible tenures, competitive interest payouts, and a straightforward online investment process.

On Grip Invest, investors can access a curated list of high-yield corporate FDs across categories. These options can be suitable for building diversified fixed income portfolios, especially for those seeking better returns than standard bank FDs but with controlled credit risk. The platform also simplifies tracking, documentation, and timely interest payouts, making the process easier for retail investors.

Also Read: Karnataka Bank FD Rates 2026

Conclusion

Fixed Deposits remain an excellent and reliable investment option for investors having low to moderate risk appetite. However, as per the trends analysed, the overall interest rates offered by top banks such as the Bank of Baroda for fixed deposits, has been on a decline. The real interest rates also go down because of the flat taxation applicable.

On the other hand, you can explore the Grip platform and find alternatives to fixed deposits such as bonds which provide high quality fixed income securities that are perfect solution for investors seeking diversification without assuming too many risks.

Visit Grip Invest today!

FAQs On Bank Of Baroda FD Rates

1. What is the FD interest rate at Bank of Baroda for 1 year?

Bank of Baroda offers 6.25% for general customers and 6.75% for senior citizens on a 1-year FD (deposits below INR 3 crore, as per the latest revision).

2. What is the TDS on BOB FD interest?

TDS is deducted at 10% if the total interest across all FDs exceeds INR 40,000 in a financial year (INR 50,000 for senior citizens).

3. Does Bank of Baroda offer higher returns than corporate bonds?

Generally, no. Corporate bonds often provide higher yields than bank FDs, but they also carry higher risk, unlike the stability of a Bank of Baroda FD.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001