Best Corporate Bonds In India (2026): Compare Yields, Ratings And Investment Options

In 2026, investors are moving beyond fixed deposits and mutual funds in favour of corporate bonds. A corporate bond is a type of debt that a business issues to raise capital. Subject to the issuer's capacity to repay, the investor receives interest in exchange and receives the principal back at maturity.

Yields on AAA-rated corporate bonds in India with two to five-year maturities surpassed 8% in May 2026, marking the highest level since early 2019. The amount raised for corporate bonds in April and May of 2026 was around INR 1.07 trillion, which is the lowest amount since 2022 for the first two months of a fiscal year.

This shows a market where bond returns in India have become more relevant, but so have risk checks.

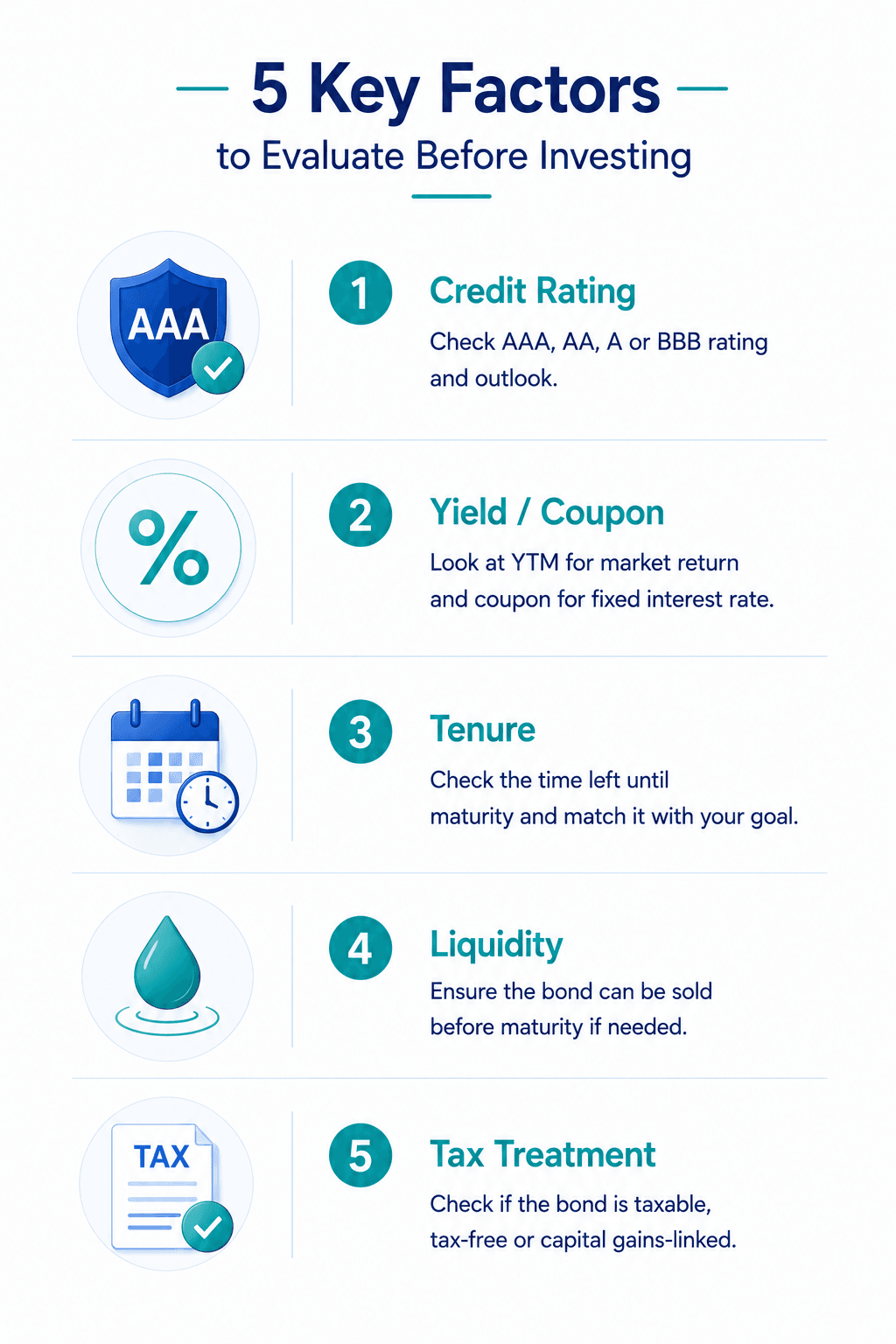

Before looking at individual bonds, investors should check five factors:

Factor | What to check |

Credit rating | AAA, AA, A or BBB rating and outlook |

Yield or coupon | YTM for market return, coupon for fixed interest rate |

Tenure | Time left until maturity |

Liquidity | Whether the bond can be sold before maturity |

Tax treatment | Taxable, tax-free or capital gains-linked treatment |

A simple way to read this market is to avoid asking, “Which bond gives the highest return?” The better question is, “Which bond fits my risk level, time horizon and tax position?”

The bonds featured in this guide were shortlisted using publicly available market data as of 29 June 2026. Rather than ranking bonds purely by returns, we grouped them based on different investor objectives, such as higher yield, stronger credit quality, shorter maturity and tax efficiency.

For each category, we considered factors such as available Yield to Maturity (YTM), credit rating, remaining maturity, issuer information and bond availability. Since market prices and yields change regularly, investors should verify the latest details before investing.

Best Corporate Bonds Available In India

The best corporate bond depends on what an investor wants from the investment. Some investors may look for higher bond returns in India. Others may prefer AAA-rated issuers, shorter maturity, regular income or tax-efficient cash flow.

For this section, the bonds have been grouped by purpose instead of ranking them in one list. This makes the comparison easier. A high-yield bond and an AAA-rated bond solve different needs, so they should not be judged only by the coupon or yield.

The tables below are based on publicly available bond listings as of 29 June 2026. Before making an investment, investors should verify the most recent yield, price, rating, maturity, and liquidity because bond information is always changing.

1. High yield

These bond investments in India were shortlisted based on visible Yield to Maturity (YTM), credit rating and future maturity date. This table focuses on high-yield corporate bonds in India along with issuer risk, liquidity and repayment profile.

Issuer | Rating | YTM | Tenure | Starts at |

Unifinz Capital | BBB minus | 14.25% | 23 months | INR 9,930 |

Best Capital | BBB | 14% | 33 months | INR 9,123 |

Akara | BBB | 13.75% | 16 months | INR 9,858 |

Since their YTM is greater than many AAA-rated bonds, these bonds fall into the high-yield category. However, there is typically more credit or liquidity risk associated with a greater YTM. Before investing, investors should review the most recent rating reason, security cover, trading price, and issuer financials.

2. AAA-rated corporate bonds

These bonds were selected based on AAA credit rating, visible coupon or YTM and future maturity date. This category is more suitable for investors who prioritise credit quality over the highest return.1

Issuer | Rating | ISIN | Issue size | Maturity | Coupon |

Poonawalla Fincorp Limited | CARE AAA | INE511C07714 | INR 2.03 crore | 06 May 2029 | 10.75% |

IOT Utkal Energy Services Limited | IND AAA | INE310L07AB7 | INR 365.00 crore | 20 Jul 2028 | 10.63% |

ICICI Lombard Gen Insurance Co Ltd

| ICRA AAA | INE513L08024 | INR 35.00 crore | 29 Apr 2029 | 10.5% |

AAA rating can reduce credit risk, but it does not remove price or liquidity risk. Investors should still check the latest yield and traded price.

3. Short-term corporate bonds

These best corporate bonds in India were selected based on maturity within a shorter time frame, visible coupon or YTM and future repayment date. This category may suit investors who do not want to lock money for many years.2

Issuer | Rating | ISIN | Issue size | Maturity | Coupon |

Shivakar Developers Private Limited | ACUITE B minus | INE0AJM07021 | INR 50.00 crore | 05 Dec 2027 | 20.75% |

Shreshta Infra Projects Private Limited | ACUITE B | INE0CKK07045 | INR 350.00 crore | 30 Jun 2027 | 20.05% |

Heritage Max Realtech Private Limited | CARE BB | INE366U08119 | INR 5.85 crore | 06 Oct 2027 | 20.00% |

Due to their shorter maturity, short-term bonds can lower duration risk. However, investors must still evaluate exit liquidity and issuer quality.

4. Long-term corporate bonds

These bond investments in India were selected based on longer maturity, visible coupon or YTM and availability across higher-rated or higher-yielding issuers.3 This category may suit investors who want to lock in income for a longer period.

Issuer | Rating | ISIN | Issue size | Maturity | Coupon |

Alpha Alternatives Financial Services Private Limited | ACUITE BBB+ | INE0L6808029 | INR 16.67 crore | 15 May 2033 | 21.00% |

Dvara Kshetriya Gramin Financial Services Private Limited | CARE BBB+ | INE179P08082 | INR 42.50 crore | 09 May 2035 | 14.50% |

Gayatrishakti Paper and Boards Ltd. | Rating to verify | INE612F07028 | INR 215.00 crore | 01 Apr 2033 | 16.00% |

Long-term bonds need a closer look at interest-rate risk. If market yields rise after purchase, the bond price may fall before maturity.

5. Tax-efficient bonds

These best corporate bonds in India were selected based on tax-free interest status, AAA rating and future maturity date.4 This category may suit investors in higher tax brackets who want tax-efficient fixed income.

Issuer | Rating | ISIN | Issue size | Maturity | Coupon |

Watermarke Estates Private Limited | ICRA BBB+ | INE07J407014 | INR 340.00 crore | 30 Sep 2028 | 17.50% |

Slice Small Finance Bank Limited | CRISIL BBB minus | INE09B308028 | INR 14.00 crore | 25 Nov 2027 | 14.00% |

Shree Renuka Sugars Limited | IND A | INE087H07094 | INR 75.00 crore | 31 Mar 2028 | 11.70% |

Tax-free bonds can improve post-tax return for some investors. However, the effective yield depends on the purchase price in the secondary market. It is important to note that the bonds mentioned above are for educational purposes only.

Why No Single Metric Can Identify the Best Bond

Investors often compare bonds using only one number, such as coupon rate or YTM. However, no single metric can determine whether a bond is suitable.

For example, one bond may offer a 14% YTM because investors demand additional compensation for higher credit risk, while another AAA-rated bond may offer a lower yield but greater repayment confidence. Similarly, a bond with an attractive coupon may still be difficult to sell before maturity if trading volumes are low.

The best corporate bond is therefore one that matches an investor's risk tolerance, investment horizon and income requirements rather than simply offering the highest return.

Corporate Bonds vs Other Fixed-Income Investments

Investors should contrast corporate bonds with alternative fixed-income investing options to ensure effective investing that aligns with investor goals and requirements. The table below draws a comprehensive comparison of corporate debt investments and others.

Option | Return source | Main risk | Liquidity | Tax angle |

Corporate bonds | Coupon or YTM | Credit and liquidity risk | Varies by bond | Interest usually taxed unless tax-free |

Fixed interest | Bank limit and reinvestment risk | Premature withdrawal possible | Interest taxed as per slab | |

Government bonds | Coupon and market price | Interest rate risk | Usually better in large issues | Taxable, except specific cases |

Treasury bills | Discount to face value | Low credit risk | Short tenure | Taxed as per rules |

Portfolio yield and price movement | Market and credit risk | Usually easy exit | Tax depends on holding and fund type |

Although corporate bonds may provide higher rates than deposits, credit risk is a trade-off. While debt mutual funds provide diversity, they do not provide a guaranteed maturity payment like a single bond. On the other hand, government securities have a lower credit risk due to sovereign guarantee.

Which Fixed Income Option Is Suitable For Different Investors?

| Investor Goal | Suitable Option |

| Capital preservation | Government Securities, AAA Bonds |

| Regular income | Corporate Bonds, FDs |

| Tax planning | Tax-free bonds (where available) |

| Higher return potential | Selected corporate bonds |

| Diversification | Debt Mutual Funds + Corporate Bonds |

How To Build A Corporate Bond Portfolio?

A corporate bond portfolio should not depend on one issuer or one rating bucket. A mix can reduce the risk of one bad selection affecting the whole allocation.

Here are the main portfolio checks:

Portfolio rule | Practical approach |

Spread issuers | Avoid putting all money in one company or group |

Mix credit ratings | Use AAA or AA names as the base, add lower-rated bonds only if suitable |

Ladder maturities | Hold bonds across short, medium and long tenures |

Check payouts | Match monthly, quarterly or annual interest with cash flow needs |

Review liquidity | Prefer bonds with clearer exit visibility if early sale matters |

While a conservative investor can maintain the majority of their bond allocation in AAA, AA, or sovereign-linked alternatives, an investor with high risk appetite may increase exposure to high-yield bonds rated BBB or A, based on their needs.

Investors should also track rating actions. A downgrade can affect both price and exit options. Bond investing is not a one-time selection exercise.

Conclusion

The best corporate bonds in India for 2026 can't be chosen solely based on the highest bond returns in India. Its suitability also depends on its rating, yield to maturity, coupon, maturity, issuer quality, liquidity, and tax treatment. High-yield bonds may have YTMs exceeding 13%, but they need more intensive credit checks due to their high-risk profile.

Before investing, investors should review the most recent rating rationale, compare post-tax returns, and more. At Grip, you can compare a range of corporate bonds that offer up to 12.5% YTM on one platform, with a detailed brief on their feature, benefits, risks, etc.

Investors should compare available corporate bonds using parameters such as Yield to Maturity, credit rating, maturity, issuer quality and liquidity before making a decision. Platforms that provide these details in one place can make the comparison process easier.

FAQs On Best Corporate Bonds In India In 2026

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001