Bond Vs Loan: Key Differences Borrowers And Investors Should Know

Introduction — Bonds And Loans Are Not The Same

India’s debt market is shifting. Up to 9 December 2025, companies raised INR 8.66 trillion through listed bonds, via private placements and public issues1. That number matters because bonds are a clear slice of the debt market. They are securities that can be issued to many investors, listed, and traded.

Loans also create debt, but they work differently. A loan is usually a one-to-one contract with a lender, with negotiated terms that do not trade in the open the way bonds can.

Since both involve borrowing and interest, the two are often mixed up. In this blog, we break down bond vs loan in plain terms, so you know what changes for the borrower, the investor, and the risk.

What Is a Bond?

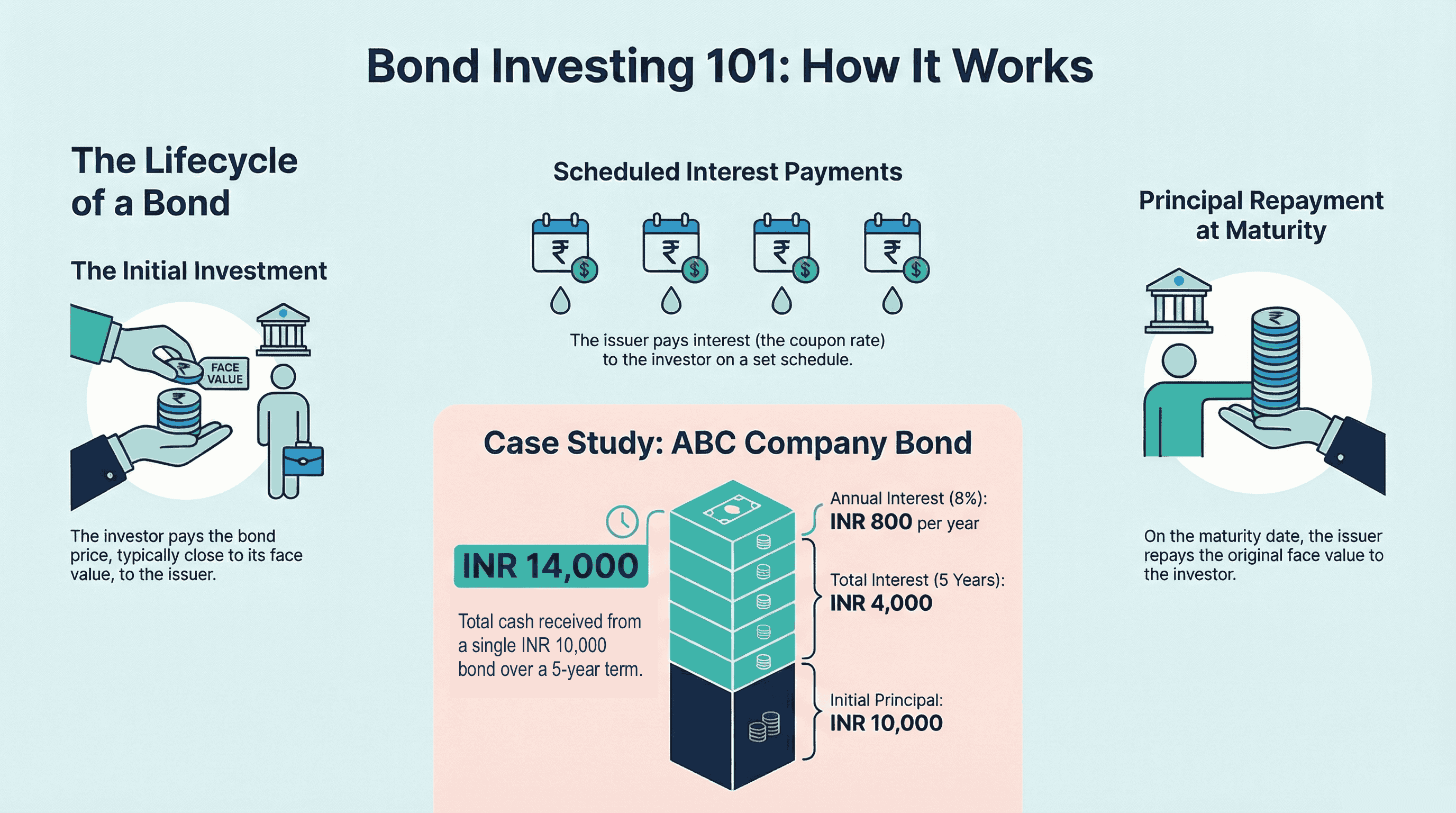

A bond lets an issuer raise money from investors for a set time, under written terms. When you buy a bond, you lend it to the issuer. The issuer can be a government, municipality, bank, or company.

How does a bond work?

- You pay the bond price, often close to its face value

- The issuer pays you interest at the coupon rate on a set schedule

- On the maturity date, the issuer repays the principal, also called face value or par value

For example, imagine a company called ABC needs INR 10 crore to build a new factory, but it does not want to take a bank loan. So ABC issues 10,000 bonds, each worth INR 10000.

- You buy one bond for INR 10,000

- The bond pays 8% per year for 5 years, so you earn INR 800 each year

- Over five years, you receive INR 4,000 as interest

- At maturity, you get back the INR 10,000 principal

- Total cash received over the term equals INR 14,000, if the issuer pays as promised

Now that we have understood corporate bonds, we can look at the other side of the coin in the bond and loan difference.

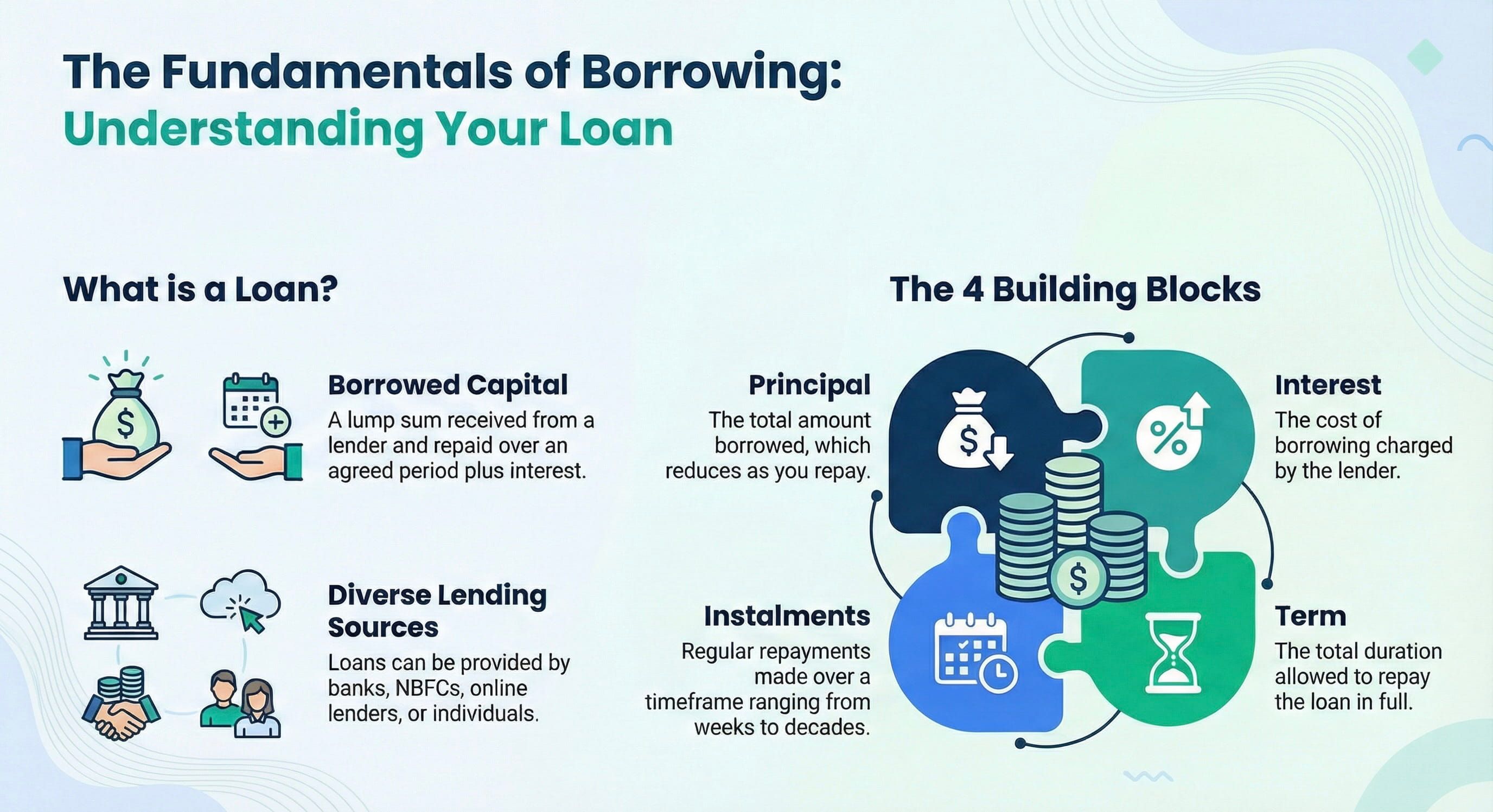

What Is A Loan?

A loan is borrowed money. You receive a lump sum from a lender and repay it over an agreed period, along with interest.

The lender can be a bank, a non-banking financial company- NBFC, an online lender, or even an individual in some cases. In the fixed-income bonds vs loans comparison, a loan usually stays between the borrower and the lender, with terms tailored to that relationship.

The basic building blocks

- Principal is the amount you borrow, and it reduces as you repay.

- Interest is the cost of borrowing, and lenders set it based on risk and loan type.

- Instalments are your regular repayments, usually monthly, and each instalment includes principal plus interest.

- Term is the time you get to repay the loan in full, which can range from weeks to decades.

For example, you take a personal loan of INR 2,00,000 from a bank for a course.

- The loan term is 2 years and the interest rate is 12% per year.

- The bank sets a fixed monthly repayment amount, called an EMI.

- You pay the EMI every month until the term ends.

- In the early months, more of the EMI goes towards interest than principal.

- Over time, the principal share increases as the outstanding balance reduces.

By the end of 2 years, you repay INR 2 lakhs plus the interest charged over the period, and the loan closes.

Bond Vs Loan: Core Differences

If you are comparing debt instruments India offers, bonds and loans can look similar at first glance. Both involve borrowing and interest, but they work very differently once you look at structure and flexibility.

Feature | Bonds | Loans |

| What it is | Tradable debt security issued to investors | Private borrowing contract with a lender |

| Source of funds | Public and institutional investors | One or a few lenders, such as banks or NBFCs |

| Main purpose | Capital raising for the issuer and investment for the buyer | Funding for a specific borrower's need |

| Tradability and liquidity | Often tradable, so liquidity can be higher | Generally non-tradable, so liquidity stays low |

| Interest setting | Coupon set at issue, often fixed, sometimes variable | Fixed or variable, often linked to a benchmark |

| Repayment pattern | Interest through the term, principal usually repaid at maturity | Regular instalments, usually monthly, covering interest and principal |

| Flexibility of terms | Terms stay fixed; renegotiation is uncommon | Terms can allow prepayment, refinancing, or renegotiation, sometimes with charges |

1. Liquidity

- Bonds can trade in the secondary market, so you may sell before maturity if buyers exist.

- Loans do not offer that exit route for the borrower, and lenders do not easily “trade” typical retail loans.

2. Risk

- For bond investors, the key risk is whether the issuer pays interest and repays principal on time.

- For lenders, the risk sits on the borrower’s ability to repay, so they monitor closely and may set covenants.

3. Return visibility

- Bonds usually show return expectations upfront through the coupon and maturity value, although the market price can move daily.

- Loans give no “return” to the borrower, but they do give cost visibility through the rate and installment schedule.

4. Cash flow shape

- Bonds often mean steady interest inflow and a large principal repayment at the end.

- Loans usually spread repayment across the term, so the outstanding balance reduces month by month.

5. Control and flexibility

- Bonds typically lock in terms at issuance, which limits mid-course changes.

- Loans often allow restructuring or early closure, though penalties may apply based on the contract.

Why Bonds Matter To Retail Investors

In bonds vs loans for businesses India, a bond is an investment instrument, while a loan is a borrowing instrument.

When you buy a bond, you usually know two things upfront. How much interest you will receive and when you will get your principal back at maturity. That makes bonds useful for planning near to mid term goals where you do not want surprises.

Predictable cash flows are the big draw. If a bond pays interest every month, quarter, or year, you can map that income to regular expenses or a savings target. It is not “guaranteed” in the real world, because the issuer still has to pay, but the schedule is clear from day one.

For many investors, the hard part is not the concept. It is access, paperwork, and knowing what you are buying. Platforms such as Grip can make bond investing feel more straightforward by bringing options in one place and simplifying the process and ongoing tracking.

Explore Grip Invest's curated list of corporate bonds offering up to 12.5% post-tax returns!

Visit Grip today!

FAQs

1. Is a bond safer than a loan?

For an investor, a bond can feel safer than lending to someone through an informal loan, because bonds come with written terms, a defined interest schedule, and are usually issued under stricter rules.

But a bond is not automatically safe. If the issuer struggles to pay, you can still lose money. The real driver of safety is the issuer’s credit quality and whether the bond has any security or guarantees.

2. Do bonds offer regular income?

Yes, many bonds can offer regular income. Most bonds pay interest, also called a coupon, on a fixed schedule. That can be monthly, quarterly, half-yearly, or yearly, depending on the bond terms.

3. Can a company choose between issuing bonds or taking a loan?

Yes. Companies often decide based on cost, flexibility, and scale. Bonds are useful when large sums are needed and the company has strong credit, while loans suit smaller or quicker funding needs with more room for renegotiation.

4. Are bonds taxed differently from loan interest?

Yes. For investors, bond interest is usually taxable based on their income tax slab, unless it is a tax-free bond. Loan interest, on the other hand, is a cost for the borrower and may qualify for deductions depending on the loan type and usage.

References:

1. Live mint, accessed from: https://www.livemint.com/market/bonds/india-bond-market-listed-debt-structural-shift-11765863860127.html

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.