Bond Indenture Explained: Meaning, Clauses & Investor Protection

A bond indenture is the legal agreement that records the terms under which a company borrows from bond investors. In India, this indenture agreement is generally reflected in the debenture trust deed and supporting issue documents. It defines payment promises, bond covenants and remedies when those promises are broken.

The role of this agreement is critical because corporate bond awareness remains limited. SEBI’s Investor Survey 2025 found that only 10% of surveyed Indian households recognised corporate bonds, compared with 53% for mutual funds and exchange-traded funds.1 Clear documentation therefore plays an important role in helping investors understand what they are buying and what protections apply.

Three parties form the core of a bond indenture:

- Issuer: The company raising money and promising to pay interest and principal.

- Bondholder: The investor lending funds by purchasing the bond.

- Debenture trustee: The SEBI-registered intermediary appointed to represent bondholders and monitor compliance.

The trustee role also gives the agreement legal weight. Section 71 of the Companies Act, 2013 requires a debenture trustee to protect debenture holders’ interests. SEBI’s non-convertible securities regulations, amended up to 21 January 2026, provide the current framework for issuing and listing such instruments. 2,3

This area has also received fresh regulatory attention. On 30 June 2026, SEBI formed an expert working group to review the framework governing debenture trusteeship activities.

Understanding the document’s purpose is the first step. The next is knowing what investors should locate inside it.

Why Should Retail Investors Read The Bond Indenture?

Many retail investors compare corporate bonds based on coupon rate or credit rating alone. However, two bonds with the same rating can provide different levels of investor protection because their indenture terms may differ.

Reading the bond indenture helps investors understand:

- Whether the bond is secured or unsecured

- What happens if the issuer misses a payment

- Whether additional borrowing is restricted

- How bondholders can enforce their rights

- The role of the debenture trustee during financial stress

Even if investors do not read every clause, understanding the key provisions can help them evaluate the overall risk of a bond more effectively.

What Does A Bond Indenture Contain?

A bond indenture brings together the financial terms, issuer obligations and investor protections attached to a bond. These provisions determine when investors receive payments, what the issuer must maintain and what action follows a breach.

The most common indenture clauses are outlined below:

| Clause | Description | Significance |

| Promise to pay | The issuer’s obligation to pay interest and repay principal according to the agreed terms | Establishes the basic legal claim for all scheduled payments |

| Rights and obligations | The duties, powers and responsibilities of the issuer and trustee | Clarifies who monitors compliance and who can act on behalf of bondholders |

| Bond covenants | Financial, affirmative and restrictive conditions that apply during the bond’s tenure | Can limit excessive borrowing, asset sales or other actions that may weaken repayment capacity |

| Security creation and maintenance | The issuer’s obligation to create and preserve security over specified assets | Helps determine whether investors have a secured claim and where that claim ranks |

| Minimum security cover | The required value of charged assets relative to the outstanding debt | Indicates the contractual collateral cushion, although it does not guarantee full recovery |

| Events of default | Payment failures, insolvency, covenant breaches, cross-defaults and other specified triggers | Defines when the trustee or bondholders can begin remedial action |

| Cure periods | Time allowed for the issuer to correct certain breaches | Shows how long enforcement may be delayed after a non-payment or covenant failure |

| Acceleration and enforcement | Procedures for demanding early repayment or enforcing security | Explains the actions available once a default becomes effective |

| Bondholder meetings and voting | Quorum, consent thresholds and collective decision-making rules | Determines how investors approve waivers, amendments or recovery measures |

| Reporting obligations | Financial statements, compliance certificates and other periodic information | Helps investors and the trustee detect weakening financial or covenant conditions |

| Amendments and notices | Procedures for changing terms and communicating material developments | Protects investors from significant changes being made without the required consent |

| Governing law and jurisdiction | The legal framework and courts that apply to the agreement | Establishes where and how disputes may be resolved |

These indenture clauses do not operate separately. Reporting obligations help identify covenant breaches, events of default activate remedies, and voting provisions determine how bondholders respond collectively.

For secured bonds, the deed may also refer to a separate security document containing detailed information about the charged assets. The indenture agreement then connects that security arrangement with the issuer’s obligations and the trustee’s enforcement powers.

These clauses create the contractual map. Their practical value becomes clearer when the issuer faces financial stress.

Examples Of Common Bond Covenants

| Covenant | Example |

| Debt restriction | Issuer cannot borrow above a specified leverage ratio |

| Dividend restriction | Company cannot pay excessive dividends while debt remains outstanding |

| Asset sale covenant | Important assets cannot be sold without lender approval |

| Reporting covenant | Quarterly financial statements must be shared with the trustee |

| Security maintenance | Charged assets must remain adequately insured and unencumbered |

These examples show how covenants help protect bondholders before repayment problems arise.

How Bond Indentures Protect Investors?

A bond indenture protects investors by converting the issuer’s promises into defined rights, continuing obligations and enforceable procedures. These protections become particularly important when the issuer’s financial condition begins to weaken.

1. Investor Rights & Enforcement

Bondholders receive explicit contractual rights relating to timely coupon payments, principal repayment, information access, and voting on material changes. The indenture also states when investors can accelerate repayment or authorize enforcement against secured assets.

2. Issuer Obligations And Early Warning Signs

Issuer responsibilities often extend beyond paying interest. Companies may be required to maintain asset cover, meet financial ratios, preserve security, retain credit ratings, and submit periodic compliance certificates. These requirements can provide warning signs before an actual payment default occurs.

3. The Central Role of the Trustee

Because individual investors rarely have the resources to monitor every condition or act collectively, the debenture trustee serves as the central coordinator. The trustee reviews compliance, communicates material developments, and represents bondholders when consent or enforcement becomes necessary.

4. The Default Response Mechanism

Events of default activate the indenture’s operational response. Depending on the terms, the trustee may issue notices, call a bondholder meeting, accelerate the debt, or enforce security.

5. Strict Regulatory Timelines

Regulatory frameworks dictate how quickly these protections must move under stress. For instance, a May 2026 SEBI adjudication order highlighted strict timelines, such as requiring trustees to notify investors within three days of a default and swiftly convening bondholder meetings.4

Protection is not a guarantee of recovery. Enforceable terms improve coordination, but asset value and the priority of competing lenders still influence the outcome. Investors must therefore look for clauses that offer less protection than they first appear to provide.

Bond Indenture vs Bond Prospectus

| Aspect | Bond Indenture | Bond Prospectus |

| Nature | Legal contract | Offer document |

| Core purpose | Defines investor rights | Explains the bond issue |

| Key content focus | Contains enforcement provisions | Contains issue details |

| Primary use phase | Used after issuance | Used during issuance |

While the prospectus explains the investment opportunity, the bond indenture governs the legal relationship between the issuer and investors throughout the life of the bond.

Red Flags Investors Should Look For

The following warning signs can indicate that the headline coupon does not fully compensate investors for the credit and documentation risk.

- Weak covenants: Broad exemptions, long cure periods or no meaningful limits on additional debt can reduce investor control. Check whether thresholds are measurable and whether breaches trigger clear action.

- High leverage: Review total debt to equity, interest coverage and debt service coverage rather than relying only on the credit rating. Compare at least two reporting periods.

For example, a fall in interest coverage from 2.5x to 1.4x provides more useful information than simply saying repayment capacity weakened. The direction and size of the change help investors assess whether operating earnings can still cover interest payments.

- Limited protections: An unsecured bond ranks behind secured creditors over charged assets. For secured issues, check whether the security is shared, subordinated or subject to earlier-ranking claims.

Investors should also examine the stated asset cover. A security document may identify collateral, but that does not establish how easily the assets can be sold or how much they may recover during enforcement.

- Callable features: A call option allows the issuer to redeem the bond early. Examine the first call date, call price and notice period. Early redemption can reduce the realised return when market interest rates have fallen.

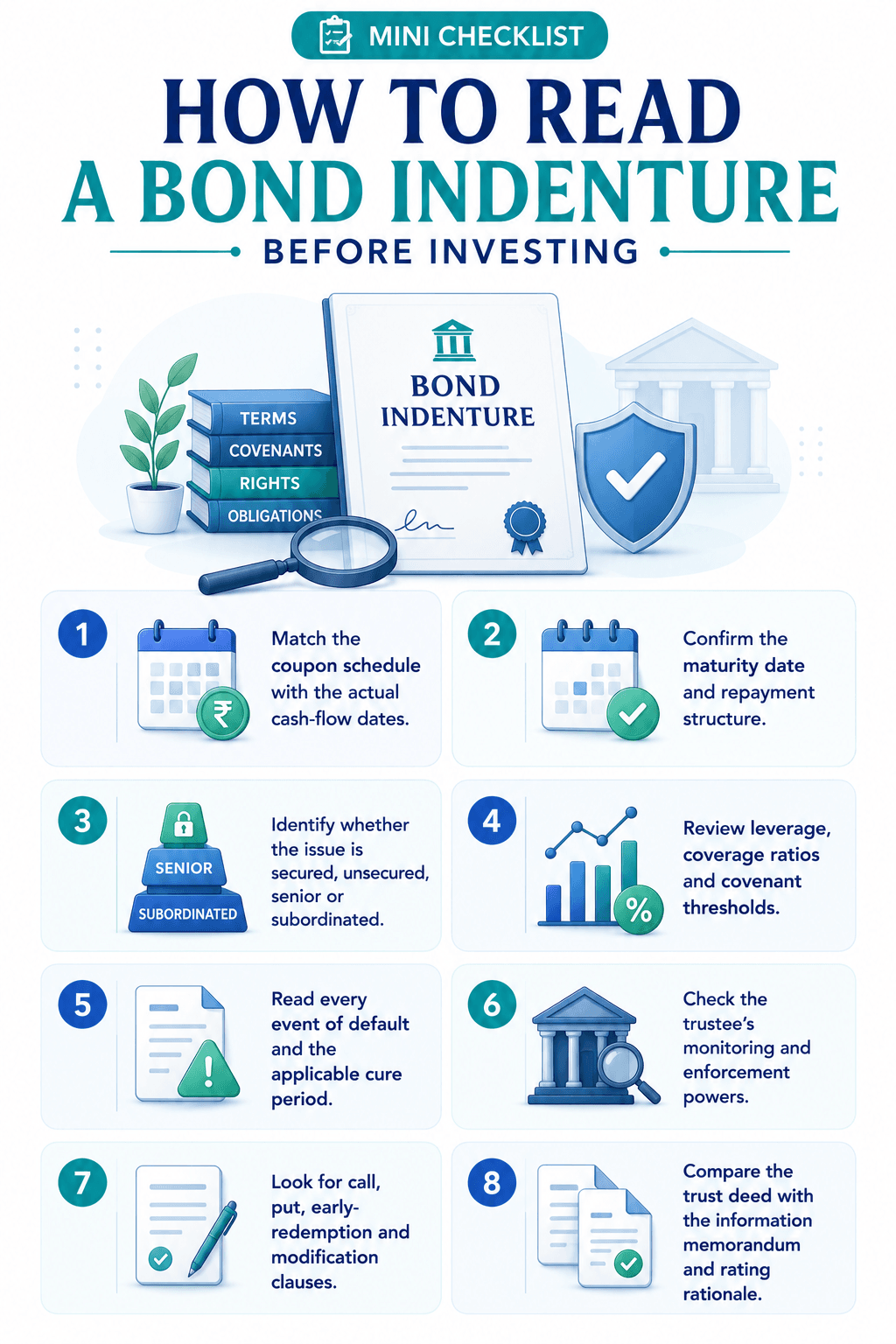

Mini Checklist: How To Read A Bond Indenture Before Investing

1. Match the coupon schedule with the actual cash-flow dates.

2. Confirm the maturity date and repayment structure.

3. Identify whether the issue is secured, unsecured, senior or subordinated.

4. Review leverage, coverage ratios and covenant thresholds.

5. Read every event of default and the applicable cure period.

6. Check the trustee’s monitoring and enforcement powers.

7. Look for call, put, early-redemption and modification clauses.

8. Compare the trust deed with the information memorandum and rating rationale.

A document review can reveal legal and structural risks. The final decision must also consider whether the issuer can generate enough cash to honour those terms.

Evaluating Corporate Bonds Beyond Returns

A complete bond assessment combines the issuer’s financial position with the protections written into its documentation.

SEBI reported that companies raised INR 9,11,078 crore through debt issues in FY 2025-26. Private placements contributed INR 8,99,736 crore, or about 98.8% of the total. Public debt issues contributed INR 11,343 crore.5

The size of the market makes careful selection important. Investors should examine the issuer’s business model, profitability, cash flows, leverage, repayment record and credit-rating changes.

They should then test those findings against the bond indenture. A high yield can reflect an opportunity, but it may also compensate for weaker credit quality, lower liquidity or fewer contractual safeguards.

Curated fixed-income opportunities on Grip Invest can simplify the initial comparison by presenting details such as yield, tenure, coupon frequency and credit rating in one place.

Sign up on Grip Invest to explore curated fixed-income opportunities and compare bonds based on their returns, tenure and risk profile.

FAQs On Bond Indenture

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001