AT1 Bonds Explained: Features, Risks, And Returns For Investors

When most investors hear the word bonds, they usually think of steady income and relatively lower risk. But not every bond works like a regular fixed-income product. Some are built very differently, especially when banks issue them to strengthen their capital position.

That is where AT1 bonds come in. Short for Additional Tier 1 bonds, these instruments can offer higher coupon rates, but they also come with features that many investors may not fully understand at first glance.

Therefore, what exactly are AT1 bonds, why do banks issue them, and what should investors know before considering them? This blog breaks down how they work, their key features, the risks involved, and how they compare with other fixed-income options.

What Are AT1 Bonds

AT1 bonds are perpetual debt instruments issued by banks to raise Additional Tier 1 capital. They do not have a fixed maturity, coupon payouts can be skipped, and they can be written down or converted into equity if the bank’s capital falls below specified levels.

Their role in the banking system is to help banks absorb losses, strengthen capital buffers, and support overall financial stability. For example, if a bank faces heavy losses and its capital position weakens sharply, its AT1 bonds may be written down or converted into shares to help absorb the stress and protect the bank’s overall financial position.

The examples below are illustrative issue examples from Indian bank disclosures (as of 20 March 2026):

| Bank | Issue | Coupon rate | Perpetual / stated term | First call date / call period |

| State Bank of India1 | AT1 bond issuance announced on 18 Jan 2024 | 8.34% | Perpetual | Call option after 10 years and every anniversary thereafter |

| Canara Bank2 | Basel III Tier I bond, ISIN INE476A08241 | 8.27% | AT1 / perpetual instrument | Call option date: 29 Aug 2029, and annually on coupon dates thereafter |

| Bank of India3 | Additional Tier I Bonds Series VII | 9.30% | AT1 / perpetual instrument | Call option on 30 Mar 2026 for bonds issued on 30 Mar 2021 |

Key Features of AT1 Bonds

The main AT1 perpetual bonds' features explain why these instruments differ from regular bank bonds and why they carry a higher level of risk:

1. Perpetual nature: AT1 bonds do not have a fixed maturity date. RBI’s framework for Perpetual Debt Instruments says they are perpetual and carry no maturity date.

2. Callable structure: These bonds may carry a call option, but the bank can exercise it only after the instrument has run for at least ten years, and only with prior RBI approval4. The bank also cannot create an expectation of early redemption.

3. Higher coupon rates: AT1 bonds usually offer higher coupon rates than regular bank bonds because they are riskier, perpetual, and subordinated.

4. Coupon flexibility: Banks have full discretion to cancel coupon payments, and unpaid interest is non-cumulative.

5. Loss-absorption feature: These bonds can be written down or converted into equity when the specified trigger is breached, and they must also be capable of write-off or conversion at the point of non-viability if RBI so requires.

6. Lower repayment priority: Investor claims rank below depositors, general creditors and subordinated debt, though they rank above equity.

7. Not a typical retail product: RBI says banks should not issue AT1 instruments to retail investors, and the minimum subscription amount, face value, trade lot, and bid lot for AT1 bonds is INR 1 crore5.

Risks Associated With AT1 Bonds

Before investing, it is important to understand the main AT1 bond risks. Unlike regular bank bonds, these are Basel III AT1 capital instruments designed to absorb losses:

1. No fixed maturity: AT1 bonds are perpetual instruments, so investors do not get a defined repayment date.

2. Call option is not assured: A bank may call these bonds only after the minimum period allowed under RBI rules and with prior RBI approval, so early redemption cannot be assumed.

3. Coupon payment uncertainty: Under AT1 bonds RBI regulations, banks can skip coupon payments on these instruments, and unpaid coupons are non-cumulative.

4. Write-down or conversion risk: One of the biggest AT1 bond risks is that the bonds can be written down or converted into equity if the bank’s capital falls below the prescribed trigger or reaches the point of non-viability.

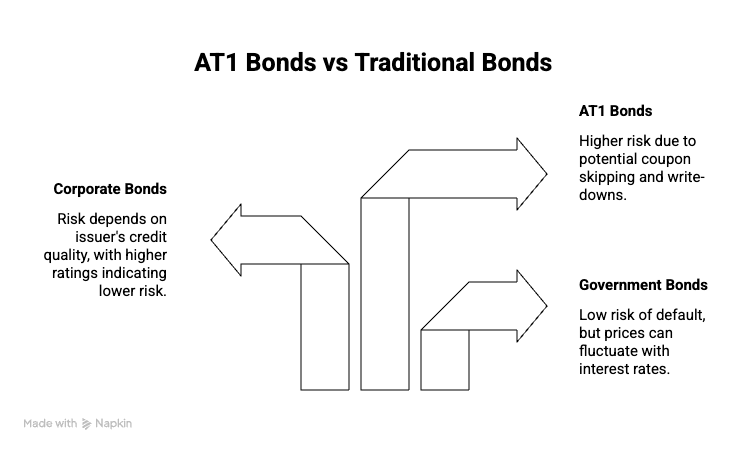

AT1 Bonds Vs Other Fixed Income Investments

Not all fixed income products carry the same level of risk. AT1 bonds are very different from regular debt products because RBI treats them as Additional Tier 1 capital instruments that can absorb losses through coupon cancellation, write-down or conversion. They are also perpetual and are not meant for retail investors.

Corporate bonds are debt securities issued by companies. Their risk and coupon levels largely depend on the issuer’s credit rating and creditworthiness. In simple terms, a stronger issuer usually pays a lower coupon, while a weaker credit profile may come with a higher yield.

Government bonds are issued by the Central or State Governments. RBI says G-Secs carry practically no risk of default in the domestic market, though they can still face interest-rate-related price movements in the secondary market.

That is why understanding risk matters even within fixed income. A higher coupon may look attractive, but the product structure, repayment priority and loss-absorption terms matter just as much before investing.

On Grip Invest, you can explore different fixed-income options in one place and compare them across risk, tenure, and return potential before investing. Sign up today!

FAQs

1. What are AT1 bonds?

These are perpetual debt instruments that banks issue to raise additional capital and strengthen their balance sheets. They carry higher risk because coupon payments can be skipped, and the bonds may be written down or converted into equity if the bank comes under severe stress.

2. Are AT1 bonds safe?

They are generally seen as higher-risk fixed income instruments rather than plain-vanilla debt products. Under RBI rules, coupon payments can be skipped, and the bonds can be written down or converted into equity if the bank faces serious stress or regulatory intervention.

3. Why do AT1 bonds offer high interest?

They tend to offer higher coupon rates because investors are taking on more risk than they would with regular bonds. AT1 bonds are perpetual, coupon payments can be skipped, and the bonds can be written down or converted into equity during stress, so the higher interest helps compensate for these features.

References:

1. NSE, accessed from: https://nsearchives.nseindia.com/corporate/SBIN_18012024164513_bsensedsc.pdf

2. NSE, accessed from: https://nsearchives.nseindia.com/corporate/CANBK_09032026170653_LettertoSE09032026CRatingSD.pdf

3. NSE, accessed from: https://nsearchives.nseindia.com/corporate/BANKINDIA2_17022026144723_AT1_Calloptionintimation.pdf

4. RBI, accessed from: https://www.rbi.org.in/commonman/Upload/English/Notification/PDFs/70BIIIMC010713.pdf

5. SEBI, accessed from: https://www.sebi.gov.in/sebi_data/faqfiles/jan-2023/1674793029919.pdf

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001