Best AAA Rated Corporate Bonds In India: Features, List And How To Choose (2026)

AAA-rated corporate bonds are high-quality debt instruments, but the category needs more than a surface-level reading.

A corporate bond is a loan given by investors to a company. In return, the issuer pays interest through coupons and repays the principal on maturity, subject to the bond terms.

AAA is the highest rating on the long-term credit scale. It shows that the issuer has a strong capacity to service debt on time. This does not mean the bond is risk free. Ratings can change, market prices can move and some bonds may be difficult to sell before maturity.

The category has become more relevant because India’s corporate bond market has grown in size. Outstanding corporate bonds stood at INR 59,19,817.11 crore in May 2026, compared with INR 47,45,005.64 crore in April 2024.1 That is an increase of about 25% in just over two years.

The issuer mix also matters. As of May 2026, corporates accounted for 28.37% of outstanding corporate bonds, followed by PSUs and statutory bodies at 20.03%, bank or government-owned NBFCs at 16.19%, NBFCs at 14.44% and banks at 12.75%.2

This is why investors should treat these highest rated corporate bonds as the first filter, not the final decision. The better question is simple. Is the bond’s return enough for its maturity, liquidity and structure?

List Of Best AAA-Rated Corporate Bonds In India

The following list is based on available data as of 29 June 2026, for AAA-rated corporate bonds with a maturity of more than one year, sorted by coupon rate.

Bond name | Rating | ISIN | Issue size | Maturity | Coupon |

Poonawalla Fincorp Limited | CARE AAA | INE511C07714 | INR 2.03 crore | 06 May 2029 | 10.75% |

Iot Utkal Energy Services Limited | IND AAA | INE310L07993 | INR 365.00 crore | 20 May 2028 | 10.63% |

ICICI Lombard General Insurance Co Ltd | ICRA AAA | INE513L08024 | INR 35.00 crore | 29 Apr 2029 | 10.50% |

Poonawalla Fincorp Limited | ACUITE AAA | INE511C07706 | INR 2.67 crore | 06 May 2029 | 10.27% |

Tata Motors Finance Limited | ICRA AAA | INE601U08069 | INR 100.00 crore | 30 Apr 2029 | 10.25% |

Iot Utkal Energy Services Limited | IND AAA | INE310L07928 | INR 1,525.00 crore | 20 Jan 2028 | 10.08% |

A closer look at the table shows that the highest coupon does not necessarily come from the largest bond issue. For example, some smaller issuances offer higher coupon rates than larger issuers, highlighting that investors should evaluate liquidity, maturity, issuer fundamentals and bond structure instead of comparing coupon rates alone.

Note: This list is not an investment recommendation. Investors should verify the latest details and suitability before investing.

Why Do Some AAA-Rated Corporate Bonds Offer High Coupon Rates?

Many investors assume that AAA-rated corporate bonds should always offer relatively low returns because they carry the highest credit rating. In practice, coupon rates depend on several factors beyond credit quality.

The coupon is fixed when the bond is issued and reflects prevailing interest rates, the issuer's funding requirements, market liquidity, and investor demand at that time. As a result, two AAA-rated bonds issued in different market conditions may offer noticeably different coupon rates.

It is also important to remember that the coupon rate is not always the return an investor earns. If a bond is purchased above or below its face value in the secondary market, the actual return is better measured by its Yield to Maturity (YTM).

Features Of AAA-Rated Corporate Bonds

The main appeal of AAA-rated top corporate bonds in India comes from credit quality, defined income and portfolio balance.

1. Higher Credit Quality

AAA-rated bonds usually come from issuers with stronger repayment capacity.

The rating indicates the highest degree of safety for timely debt servicing and the lowest credit risk within the rating scale. This gives investors more comfort than lower rated bonds.

Still, the rating is not permanent. Investors should check the latest rating, rating outlook and any recent downgrade risk. A stable outlook gives more comfort than a negative outlook.

What Happens If A AAA Bond Is Downgraded?

Although uncommon, a AAA-rated bond can be downgraded if the issuer's financial position weakens. A downgrade does not automatically mean the company will default, but it can reduce the bond's market value because investors may demand a higher yield for the increased credit risk.

Investors who intend to sell before maturity should therefore monitor rating changes regularly rather than checking the rating only at the time of purchase.

2. Predictable Income

Most AAA bonds in India pay a fixed coupon, which helps investors estimate income in advance.

For example, an investment of INR 1 lakh in a bond with a 10.5% annual coupon can generate INR 10.5K in gross yearly interest, before tax. If the investor falls in the 30% tax slab, the post-tax interest falls to about INR 7,350.

Coupon Rate vs Actual Return

Many first-time investors confuse the coupon rate with the return they will actually earn.

For example, a bond carrying a 10.50% coupon may generate a lower overall return if it is purchased above its face value in the secondary market. Similarly, purchasing the same bond below face value can increase the effective return.

For this reason, experienced investors generally compare bonds using Yield to Maturity (YTM) rather than coupon alone.

3. Diversification Benefits

AAA corporate bonds can add fixed income investments beyond fixed deposits, debt funds and equities.

They may suit investors who want defined payouts but do not want to take equity-like risk. They can also help spread money across issuer types and maturity dates.

The recent market movement shows why timing matters. AAA corporate bond yields in the two to five year bucket moved above 8% in late May 2026, the highest level since early 2019.3 In May, two year AAA yields rose by about 40 basis points, while three to five year yields rose by around 30 basis points.

That movement created better entry yields for some investors, but it also showed that bond prices can change quickly.

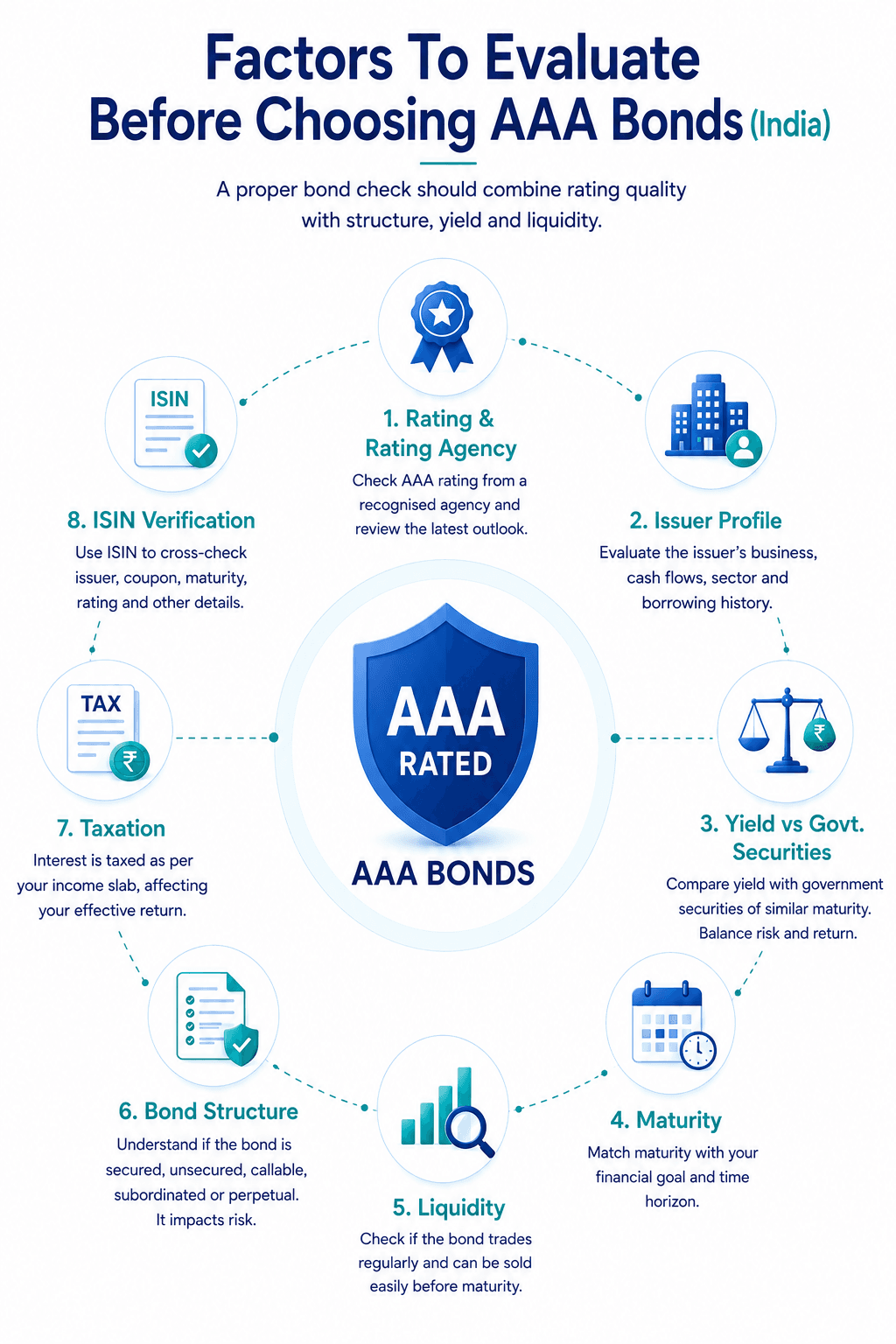

Factors To Evaluate Before Choosing AAA Bonds (India)

A proper bond check should combine rating quality with structure, yield and liquidity.

1. Rating and rating agency: Check whether the bond is rated AAA by a recognised agency. Also review the latest rating date and outlook. A rating from last year may not reflect the issuer’s current position.

2. Issuer profile: Look at the issuer’s business, cash flows, sector and borrowing history. A large issuer with stable earnings may offer better comfort than a smaller issuer with limited public information.

3. Yield versus government securities: Compare the bond yield with government securities of similar maturity. If the extra return is too small, corporate bond risk may not be worth taking. If the extra return is too high, understand the reason.

4. Maturity: Match maturity with your goal. A 2028 bond may suit a near-term goal better than a 2029 or 2030 bond. Longer maturity can increase price sensitivity when interest rates change.

5. Liquidity: Check whether the bond trades regularly. A bond may show a high coupon but still be hard to sell before maturity.

6. Bond structure: Read whether the bond is secured, unsecured, callable, subordinated or perpetual. These terms change the risk profile even when the rating is AAA.

7. Taxation: Interest is usually taxed as per the investor’s slab. This can reduce the effective return for higher-income investors.

8. ISIN verification: Use the ISIN to cross-check issuer name, coupon, maturity, rating and security details. This reduces the risk of relying only on a platform display.

Common Mistakes Investors Make When Buying AAA Bonds

Many investors focus only on the coupon rate while ignoring other factors that influence overall returns.

Some common mistakes include:

- Choosing the highest coupon without evaluating the issuer.

- Confusing coupon rate with Yield to Maturity.

- Ignoring liquidity before investing.

- Not checking the latest credit rating or outlook.

- Investing in longer-maturity bonds without understanding interest-rate risk.

- Looking only at returns without considering taxation.

Avoiding these mistakes can help investors make more informed fixed-income investment decisions.

What Investors Should Look For?

Instead of chasing the highest coupon, investors should understand which issuer type fits their risk profile.

1. PSU issuers

Public sector undertaking issuers often attract conservative investors because of government ownership or strategic importance.

These issuers may offer better comfort on repayment visibility. However, investors should still check the bond’s exact terms, maturity and yield. PSU ownership does not remove all market and liquidity risk.

PSU bonds may suit investors who prefer stability over the highest available coupon.

2. Financial institutions

Banks, NBFCs, housing finance companies and insurance-linked issuers are active borrowers in the bond market.

These bonds may offer higher coupons than some PSU issuers. In return, investors should check asset quality, capital strength, liquidity position and exposure to credit cycles.

For example, a finance company may be AAA rated, but its business can still be sensitive to borrowing costs and loan repayment trends.

3. Large corporates

Large corporates can offer a mix of brand strength, business scale and better coupon opportunities.

Here, investors should not rely only on the company name. They should review debt levels, cash generation, sector risk and group support.

A large corporate with stable cash flows may be suitable for investors who want quality debt exposure with a defined maturity.

AAA Bonds vs Fixed Deposits

AAA bonds and fixed deposits both offer regular income, but they work differently.

Factor | AAA corporate bonds | Fixed deposits |

Return | Coupon or yield based | Fixed interest rate |

Credit risk | Depends on issuer and bond terms | Depends on bank strength and deposit insurance limits |

Liquidity | Market based and may vary | Premature withdrawal may be available |

Price movement | Market price can change | Traditional FDs do not show daily market prices |

Taxation | Interest taxed as per slab | Interest taxed as per slab |

Complexity | Needs rating, ISIN and structure checks | Easier to understand |

A Practical Example

Suppose an investor has INR 5 lakh available for three years.

Choosing a fixed deposit provides a predetermined interest rate and relatively simple withdrawal rules. Investing in a AAA-rated corporate bond may generate a higher coupon, but the investor should also consider market liquidity, price fluctuations and taxation before deciding.

The right choice depends on the investor's income requirements, risk tolerance and investment horizon rather than returns alone.

Fixed deposits are simpler. Investors know the rate, tenure and premature withdrawal rules upfront.

AAA corporate bonds may offer higher income potential, but they require more checks. For example, a 10.50% coupon bond may generate higher gross income than a 7.00% fixed deposit. On INR 1,00,000, the annual gross interest difference is INR 3,500 before tax.

That gap is to be noted. But it should be weighed against liquidity, price risk and issuer-specific risk.

Final Checklist Before Investing In AAA Corporate Bonds

Before investing, consider the following checklist:

- Verify the latest credit rating and outlook.

- Compare Yield to Maturity instead of coupon alone.

- Review the issuer's financial position.

- Understand whether the bond is secured or unsecured.

- Check trading liquidity if you may sell before maturity.

- Match the bond's maturity with your financial goals.

- Evaluate post-tax returns instead of pre-tax coupon rates.

Even highly rated bonds should be selected only after considering these factors.

Conclusion

AAA-rated corporate bonds can be useful for investors who want high-quality fixed-income investment options beyond fixed deposits.

However, the right approach is not to pick the highest coupon blindly. Investors should check rating quality, issuer strength, maturity, yield spread, liquidity, structure, and post-tax return.

For beginners, AAA bonds can be a good way to understand fixed income beyond deposits. For informed investors, they can help improve portfolio income without moving too far down the credit-risk ladder.

FAQs On AAA Rated Corporate Bonds

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001