Post Office 1 Year FD Interest Rate: Returns, Safety And Alternatives

When we talk about market volatility, government-backed saving instruments attract investors seeking options that offer stability and predictability. These include the post office 1 year FD interest rate, which remains a popular option for investors interested in low-risk, short-term returns.

With a post office time deposit, you can earn assured interest without exposure to market fluctuations. A one-year tenure is suitable for many individuals, during which they can park surplus funds temporarily, which may include emergency savings or surplus salary.

Understanding how the post office 1 year FD interest rate works has become important with fluctuating interest rates across banks and market-linked instruments.

Read through the article to learn about rate structure, eligibility, return comparisons, etc.

Post Office 1 Year FD Interest Rate Explained

The post office 1-year FD interest is best suited for investors seeking predictable and assured returns over a short period of time. It is notified by the Government of India and is consistent throughout all branches of India.

Current Rate Structure

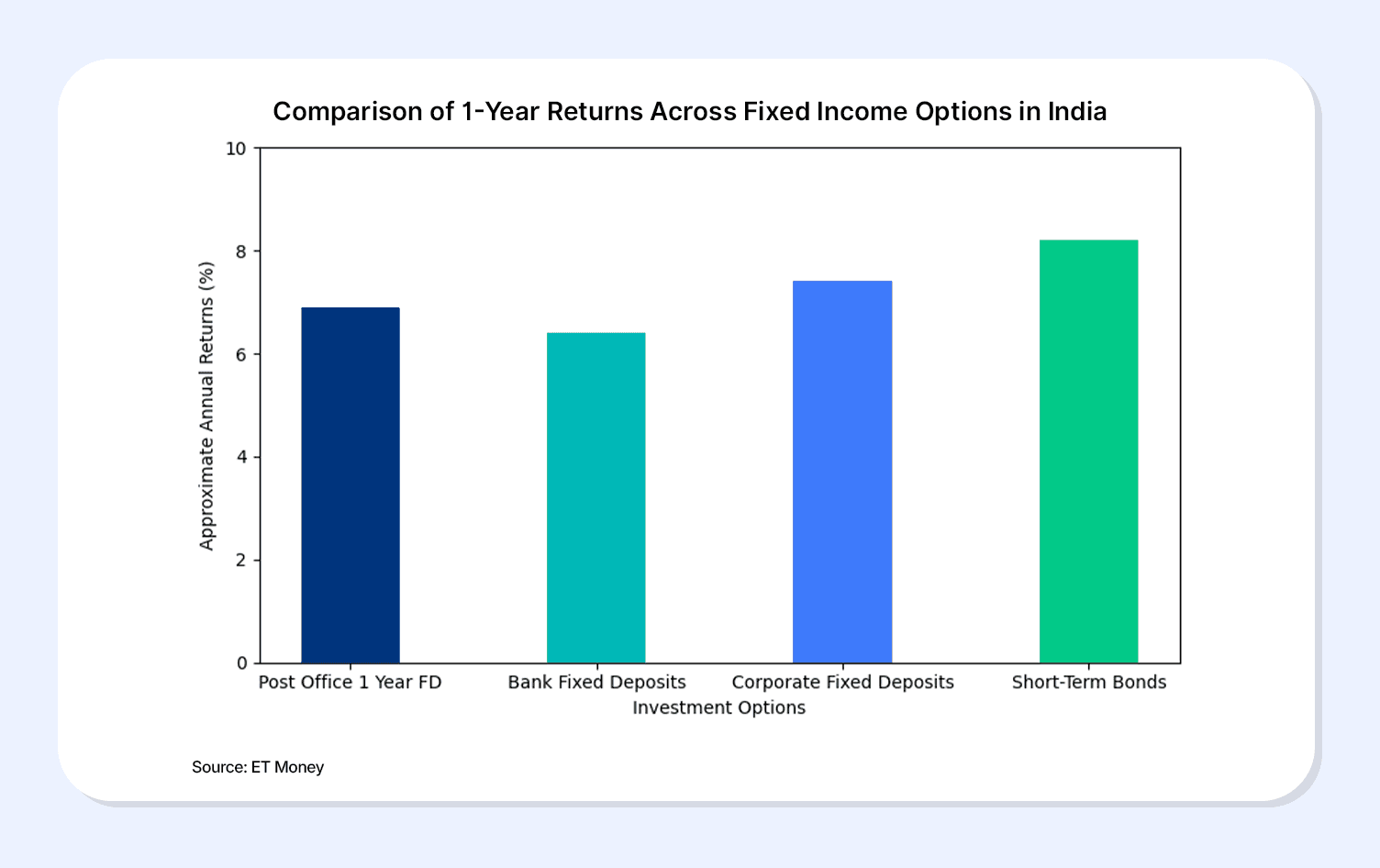

According to the latest updates, the current interest rate for the post office 1-year FD stands at 6.9 percent per annum. The interest gained is calculated annually and added to the amount at maturity.

These rates are reviewed by the Ministry of Finance every quarter. This signifies that future investments may be subject to revisions, while the existing ones continue at a locked-in rate.

Minimum And Maximum Investment

You will need to deposit a minimum amount of Rs. 1000 to open a post office time deposit. This makes it accessible to a wide range of investors. Investors can deploy large sums as there is no maximum limit, without any safety concerns.

- Lock in rules

The 1 year post office fixed deposit has a mandatory lock-in period of 12 months. Any premature or emergency withdrawal is allowed only after 6 months, which will result in reduced interest.

Also Read: Is Putting Rs.50k In FD for 10 Years Worth It?

How Returns Compare With Other 1 Year Options

It is common for investors to compare the post office 1 year FD interest rate with other short-term fixed income options before deciding. Each differs in terms of liquidity, risk, and returns.

Bank FDs

Both public and private banks offer a 1-year FD offering an interest rate ranging between 66.5 to 7.5 %. The rates are also dependent on the bank and depository category. Senior citizens will likely receive a higher interest rate compared to others. Bank FDs are insured only up to 5 lakhs per depositor, introducing a layer of credit risk for a larger investment.

Corporate FDs

Unlike post office 1 year FD interest rates, corporate FDs typically offer higher returns, often ranging between 7.5% to 9%, but come with relatively higher credit risk. These are non government backed instruments and may attract penalties on premature withdrawal. Corporate FDs are better suited for investors willing to take limited credit risk in exchange for improved yields. Today, investors can also access select corporate FDs through regulated digital platforms like Grip, which help simplify discovery, comparison, and investing across vetted fixed income options.

Also Read: Best Short-Term Investment Plans For 3 Months

Bonds With Similar Tenure

Some short-term bonds and debt instruments exceed traditional FDs in terms of returns. Investors with high tax brackets might receive better post-tax returns via high-quality corporate bonds.

Safety, Liquidity, And Taxation

Factor | Post Office 1 Year Fixed Deposit in India |

Safety Level | Fully backed by the Government of India, offering a sovereign guarantee |

Credit Risk | Nil, as returns are not linked to issuer performance |

Liquidity | Moderate, with restricted access during the lock-in period |

Premature Withdrawal | Allowed after 6 months, but at a reduced interest rate |

Interest Payout | Compounded annually and paid at maturity |

Tax Treatment | Interest is fully taxable as per the income tax slab |

TDS Applicability | No tax deduction at source by the post office |

Tax Benefits Under Section 80C | Not available for a 1-year tenure |

Suitability | Ideal for conservative investors and short-term fund parking |

When To Look Beyond Post Office FDs?

Although the post office's 1-year FD interest rate offers stability and capital protection, it may not suit all investors. Some situations call for exploring alternatives offering high returns or better tax efficiency.

Yield limitations

Even when post office FDs provide predictable and fixed returns, the interest rate may not always keep pace with inflation. The real returns after tax and inflation could appear limited to investors with higher risk tolerance.

Role Of Market-Linked Fixed-Income Instruments

High-quality corporate bonds, debt mutual funds, and other structured instruments are market-linked fixed income options that can offer superior yield potential. They offer investors benefits from credit spreads to interest rate movements.

Trusted platforms like Grip Invest are one such example that give you access to a curated list of fixed-income opportunities.

Recommended Reading: Best Corporate FDs of 2026

Conclusion

Investors seeking safety and short-term capital preservation will find the post office's 1-year FD interest rate a dependable investment option. They remain best suited for conservative investors offering predictable returns, government backing, and simple access.

However, they also have their limitations. Over time, real returns can be reduced due to inflation impact, taxability of interest, and capped yields. This is where moving beyond conventional deposits becomes necessary. Investing in corporate bonds and other selected fixed-income instruments could be the solution.

These investments become seamless when partnered with trusted platforms such as Grip Invest. You gain access to a curated list of market-linked fixed income options that offer transparency and investor-first principles.

Explore fixed income strategies with Grip and make more informed decisions for a better future.

FAQs

1. What is the current post office 1-year FD interest rate?

As per the latest announcements by the government in India, the 1-year FD interest rate per annum is 6.9%. The interest is compounded annually and paid at maturity. This makes it suitable for short-term capital parking.

2. Is the post office FD safer than a bank FD?

The post office FD is safer compared to the bank FD. This is because it is fully backed by the Government of India, which eliminates credit risk.

3. Is interest from a post office FD taxable?

The interest earned from a post office fixed deposit is fully taxable under the “Income from Other Sources,” and has no tax deduction at source by the post office.

4. Are bonds better than a post office FD for 1 year?

In a way, market-linked fixed income instruments and corporate bonds offer higher yields than the post office 1-year FD interest rate. Unlike post office FDs, they carry market risk and credit risk.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001