Karnataka Bank FD Interest Rates: Tenure-Wise Returns And Comparison

Karnataka Bank is a private sector bank established in 1924 and headquartered in Mangaluru, Karnataka. The bank is led by MD & CEO Srikrishnan Hari Hara Sarma and is known for its strong South India presence, SME banking focus, and steadily expanding digital banking services.

One Sunday afternoon, Raghav and his father, Mahesh, were reviewing their savings when Raghav noticed that a Karnataka Bank fixed deposit was nearing maturity. Mahesh suggested simply renewing it, as there were no immediate expenses planned.

Raghav agreed but added that comparing fixed deposit tenures could help them choose an option better aligned with their goals. Mahesh was pleasantly surprised and realised that even small decisions could make a meaningful difference.

Fixed deposits have been a safe way to save money for decades now. In fact, this investment tool has made its way into even the younger generation’s investment portfolio. However, one mistake that people from all generations make is assuming that all fixed deposits are the same. While the overall terms of fixed deposits are similar across the board, there are some fine differences, even when offered by the same bank.

Why Investors Track Karnataka Bank FD Rates

Karnataka Bank has been a trusted entity for a long while. The bank was established a century ago, in 19241. Since then, it has become a favoured bank for many. The main reason why the bank has been popular among the people is that it is a regional bank. Karnataka Bank FD interest rates are also competitive, which further adds to its popularity.

1. Regional Bank Trust

The benefit of the bank being regional is that it understands the needs of its region's people. By using this knowledge, the bank can craft schemes that best suit its customer base.

2. Competitive Deposit Rates

Having competitive Bank FD interest rates India has also helped the bank a lot. People want to save more while ensuring safety, which they can easily do with Karnataka Bank FD interest rates.

3. Karnataka Bank FD Interest Rates Overview

Karnataka Bank offers various FD schemes based on factors such as tenure, amount, and the depositor's age. The interest of these different schemes also differs. Here is a brief review of Karnataka Bank FD interest rates:

4. Tenure-wise Rates

The first, most crucial deciding factor of Karnataka Bank FD rates today is the tenure. Karnataka Bank offers various FDs with tenures such as 444 Days Fixed Deposit and 555 Days Fixed Deposit.

5. Senior Citizen Benefits

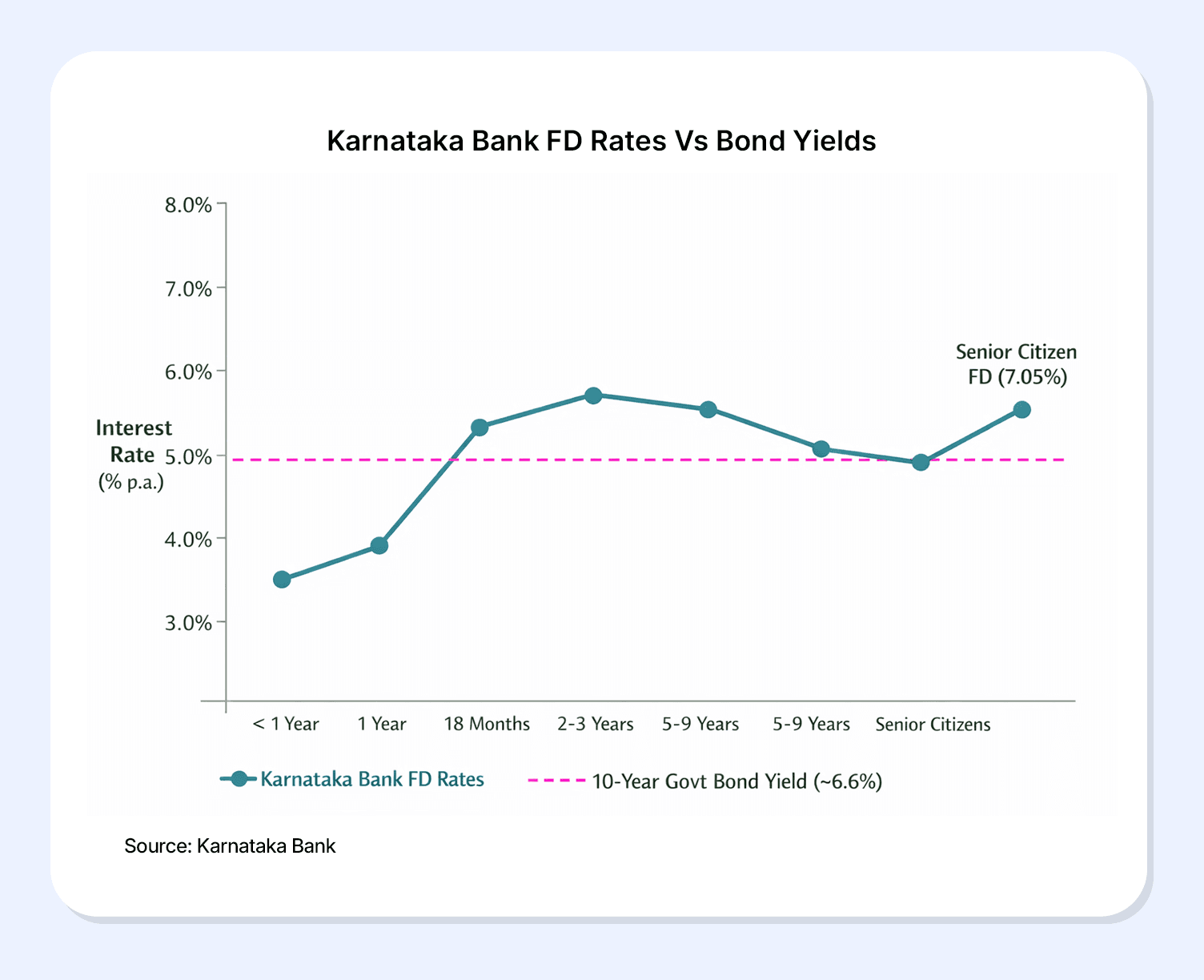

Another factor that influences Karnataka Bank FD rates today is the age of the depositor. So if the depositor is a senior citizen, then they will qualify for higher Karnataka Bank FD interest rates, so while a general citizen will receive 6.50% on a 444 Days Fixed Deposit and 6.65% on a 555 Days Fixed Deposit, senior citizens will get 6.90% on a 444 Days Fixed Deposit and 7.05% on a 555 Days Fixed Deposit2.

Key Features Of Karnataka Bank Fixed Deposits

Karnataka Bank fixed deposits come with several customer-friendly features that make saving simpler, more accessible, and flexible for both short-term and long-term goals.

1. Minimum Deposit

When it comes to minimum deposits, Karnataka Bank's special FD schemes require just INR 100. Depending on your financial situation, you can increase the amount. However, the amount will only be increased in multiples of INR 100. Having such a low minimum deposit requirement, Karnataka Bank has allowed people with limited earnings to enjoy the benefits of Fixed deposit returns.

2. Premature Withdrawal

While premature withdrawals are usually not permitted in fixed deposits, Karnataka Bank offers callable options. Callable options allow early withdrawal before maturity. However, depositors should note that premature withdrawals also affect the interest earned and may incur penalties.

Additionally, premature withdrawal rules include recalculation of Karnataka Bank FD interest rates and a penalty (usually 0.5%–1%) depending on the amount and type of deposit.

3. Auto Renewal

Auto-renewal means that once your current FD matures, it will get renewed for the same tenure without the need for any new documentation. Karnataka Bank provides an auto-renewal facility for its special FD schemes. After maturity, your FD will automatically renew for the same tenure at the prevailing Karnataka Bank FD interest rates.

Karnataka Bank FD Vs Other Fixed Income Options

Fixed income options offer stability and predictable returns, but their features, risks, and benefits vary significantly across Karnataka Bank FDs, corporate FDs, and bonds.

Feature | Karnataka Bank FD | Corporate FD | Bonds |

Issuer type | Scheduled commercial bank | Private or public companies | Government or corporate entities |

Returns predictability | Fixed and guaranteed for the chosen tenure | Fixed, but it depends on the issuer's strength | Can be fixed or market-linked |

Wide range from short-term to long-term (up to 10 years) | Usually limited, pre-defined tenures | Varies widely based on bond type | |

Minimum investment | INR 100 | Typically higher than bank FDs | Often higher entry amounts |

Higher interest rates are available | May or may not offer senior benefits | Generally, no senior-specific rates | |

Allowed as per bank rules | Often restricted or penalised | Limited liquidity unless traded | |

Risk level | Low | Moderate | Varies from low to high |

Insurance cover | Covered under DICGC up to INR 5 lakh | No deposit insurance | No deposit insurance |

Types Of Fixed Deposits At Karnataka Bank

1. Regular Fixed Deposits

This is the standard fixed deposit that most investors use. You can open an FD with as little as INR 100 and choose a tenure from 7 days up to 10 years, earning a higher interest rate than a savings account. You also get options for how interest is paid — quarterly, half-yearly, yearly or at maturity — and can opt for a monthly payout at a slightly discounted rate if you need regular income. Premature withdrawal is allowed under the bank’s rules, usually with a reduction in interest.

2. Senior Citizen Fixed Deposits

If you are aged 60 or above, Karnataka Bank provides preferential interest rates on its regular FDs. Senior citizen rates are higher than the standard ones across most tenures, helping retirees maximize income from their savings while keeping risk low.

3. Tax Planner Fixed Deposits

This is Karnataka Bank’s tax-saving FD option that qualifies for deduction under Section 80C of the Income Tax Act. It comes with a mandatory 5-year lock-in period, and you typically can’t withdraw funds early or take a loan against this deposit. This makes it a disciplined choice for long-term savings with tax benefit.

4. Special Fixed Deposit Schemes (e.g., 444 & 555 Days)

Karnataka Bank occasionally offers special tenure FDs such as 444-day and 555-day deposits that come with competitive interest rates on those specific durations. These aren’t permanent products like regular FDs, but they give investors an extra option between short and medium-term tenures with attractive rates and usually senior citizen premiums as well.

5. Flexi Fixed Deposits (Soulabhya Flexible Deposit)

Under the Flexi FD (sometimes called the Soulabhya scheme), your surplus savings can be automatically converted into a fixed deposit to earn higher interest, while still allowing partial withdrawals without breaking the entire FD. This combines the liquidity of savings accounts with the better yields of fixed deposits

How To Choose The Right FD Tenure

While fixed deposits are a crucial part of any financial portfolio, one should always be vigilant before choosing which one to invest in. It is because not all fixed deposits are made the same. While some would work extremely well for you, others might not be a good fit. Therefore, when choosing the right fixed deposit, make sure:

1. Matching Deposits with Financial Goals

All fixed deposits are not made similarly. It is not only Bank FD interest rates India that make them different. There are several other factors, such as the depositor's age, the tenure of the deposit, and the specific financial goals you aim to achieve, that should guide your choice to ensure the investment serves its intended purpose effectively.

2. Diversification Across Issuers

The best financial advice that anyone can give you is not to put all your eggs in a single basket. The power of diversification in financial investment is undeniable. Having various schemes in your portfolio will help you reduce risk and increase returns. You can explore various safe and fixed income investments on the Grip Platform as an alternative to the conventional fixed deposits.

Conclusion

Choosing the right fixed deposit is less about blindly renewing and more about aligning tenure, rates, and flexibility with your financial goals. Karnataka Bank fixed deposits continue to offer safety, predictability, and ease, especially for conservative investors and senior citizens who value stability and assured returns.

At the same time, relying on a single issuer or product can limit long-term outcomes. A balanced approach that combines bank fixed deposits with diversified fixed-income options helps manage risk while improving return potential.

Platforms like Grip Invest make it easier for investors to explore regulated fixed-return opportunities beyond traditional bank FDs, enabling smarter diversification within a disciplined, long-term financial plan.

FAQs

1. What are Karnataka Bank FD interest rates today?

Karnataka Bank FD interest rates range from 3.50% to 6.65% per annum for general customers, and from 3.75% to 7.05% per annum for senior citizens on selected schemes and tenures.

2. Does Karnataka Bank offer higher rates for senior citizens?

Karnataka Bank FD rates today are decent, ranging from 6.90% on a 444 Days Fixed Deposit and 7.05% on a 555 Days Fixed Deposit. The current range is somewhere between 3.75% to 7.05% per annum.

3. Are bank FDs safer than bonds?

FDs are generally simpler and safer, while bonds offer a range of risk and return profiles.

4. Should investors diversify fixed-income investments?

Yes, investors should always diversify their fixed-income investments. Including a variety of schemes in your portfolio can help minimise risk while enhancing the potential for higher returns.

References:

1. Karnataka bank, accessed from: https://www.karnatakabank.bank.in/about/bank

2. Policy bazaar, accessed from: https://www.policybazaar.com/fd-interest-rates/karnataka-bank-fd-rates/special-fd-scheme/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001