Canara Bank FD Interest Rates 2026: Latest Rates, Tenure Options, and Safer Alternatives

Canara Bank FD rates currently range from 3- 6.60% p.a. for general customers on domestic callable fixed deposits below INR 3 crore, depending on the tenure1. Senior citizens can earn up to 7.10% p.a., while investors looking for tax benefits can consider the Canara Tax Saver Scheme.

The bank offers fixed deposit tenures from as low as 7 days for eligible deposits to a maximum of 120 months.2

Canara Bank is one of India’s leading public sector banks, founded in July 1906 at Mangalore and headquartered in Bengaluru3. The bank strengthened its market position after the amalgamation of Syndicate Bank came into effect in 2020 and is currently led by Managing Director & CEO Shri Brajesh Kumar Singh. It is known for its strong government backing, wide branch network, and diversified retail and corporate banking operations4.

Mr Sharma, or Sharmaji as he is lovingly called, has been associated with Canara Bank for over thirty years. When he recently received a bonus of INR 2.50 lakh, he decided to get another Fixed Deposit in the home branch. A fixed deposit has been the most preferred investment alternative, as he has a low risk appetite and predetermined financial goals. His son, now 22, told him that the real post-tax rate of interest on fixed deposits is quite low. He suggested looking for alternative investments such as fixed-income securities or bonds.

Fixed Deposits or FDs are quite popular investment assets, especially when you have a low to moderate risk appetite. People having long-term financial goals often prefer Fixed Deposits over other investment assets largely because they provide fixed returns, and the chances of default, especially with established banks, are quite low.

One of the popular government-owned public sector banks is Canara Bank, which has been in existence for over a century and is trusted by millions of people around the country. If you are looking to open a new fixed deposit, you can consider Canara Bank, as it has a large network with a seamless digital experience.

As interest rates have fluctuated across the banking system in 2026, understanding the latest Canara Bank FD interest rates becomes crucial for choosing the right tenure and maximising earnings.

Let us find out more about the latest rates, tenure options, and the alternatives to a fixed deposit in Canara Bank.

Canara Bank FD Interest Rates 2026 Update

Following the recent changes to the repo rate requirements by the RBI, deposit and loan interest rates have also changed. Here are the latest FD interest rates, including Canara Bank senior citizen FD rates:

Tenure | General Public Rate (% p.a.) | Senior Citizen Rate (% p.a.) |

7–45 days | 3 | 3 |

46–90 days | 4 | 4 |

91–179 days | 4.25 | 4.25 |

180–269 days | 5.25 | 5.75 |

270 days – < 1 year | 5.5 | 6 |

1 year & above – 1 year 3 months, except 444 days | 6.25 | 6.75 |

444 days | 6.5 | 7 |

Source: Canara Bank6

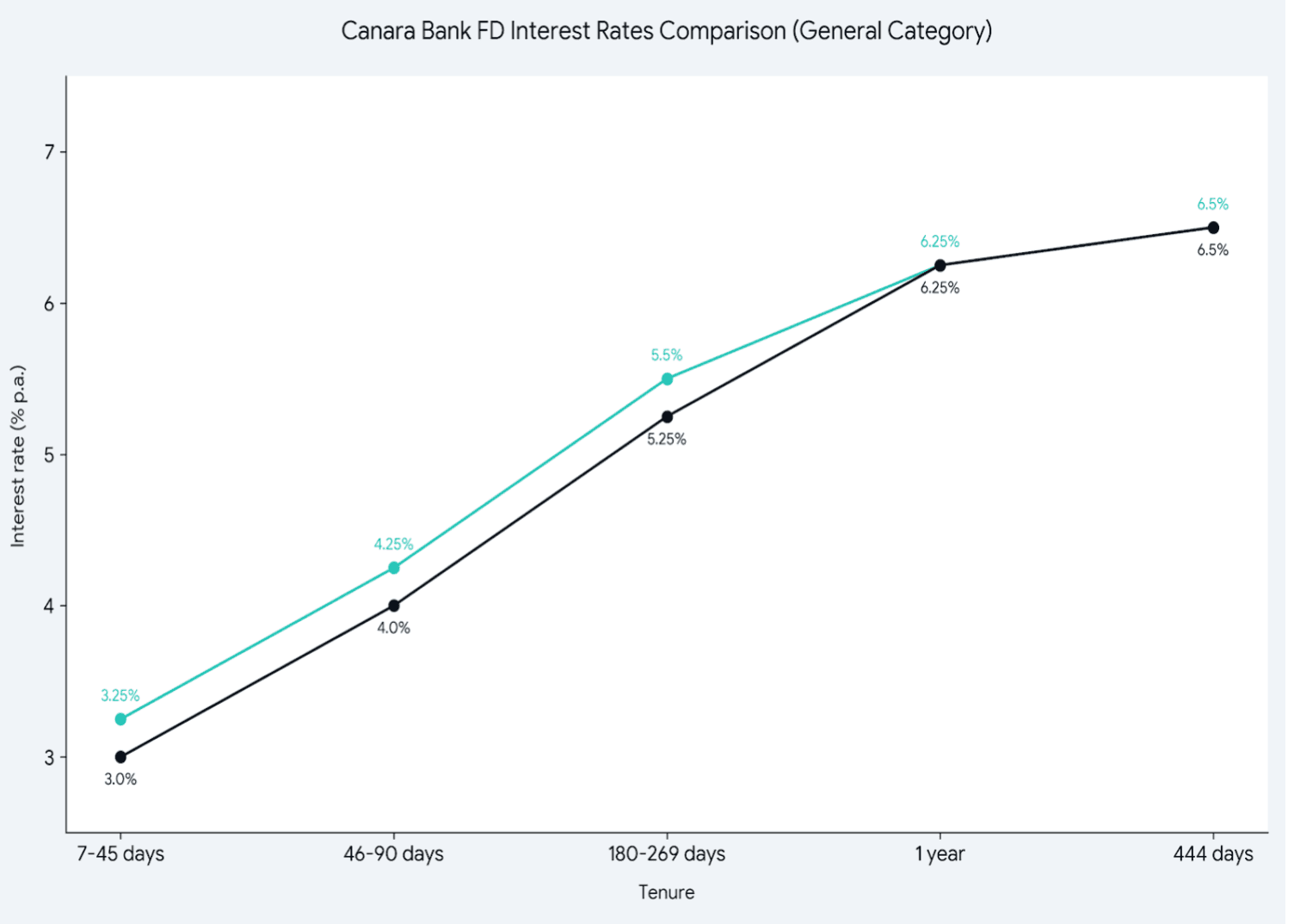

Here is how the rate of interest on Canara Bank FDs has changed in two years:

The comparison shows that Canara bank FD have not fallen uniformly across all tenures. Rates for shorter tenures of less than one year have declined, while the 1-year-and-above tenures and the 444-day special deposit have remained broadly unchanged.

Also Read: FD Auto Renewal: What Are The Risks & Benefits and How To Do It?

Key Features Of Canara Bank FDs

Canara Bank offers flexible fixed deposit options with a low minimum investment and multiple payout modes, including monthly, quarterly, and annual interest. Investors can easily manage reinvestments through the Canara Bank FD renewal facility, which supports auto-renewal across most tenures.

Premature closure is allowed subject to the bank’s Canara Bank FD premature withdrawal rules and applicable penalties. Senior citizens earn higher returns compared to regular customers, while NRIs can benefit from competitive Canara Bank NRE FD rates. For long-term savers, Canara Bank tax saver FD rates offer assured returns with a five-year lock-in.

Also Read: Post Office 1 Year FD Interest Rate 2026

Canara Bank FD Schemes

Canara Bank offers different fixed deposit schemes for regular investors, tax-saving depositors, senior citizens and NRIs. These schemes vary based on tenure, interest payout, premature withdrawal facility and tax treatment.

Canara Bank FD scheme | Key details |

Canara Tax Saver Deposit | Official tax-saving deposit scheme available under Fixed Deposit and Kamadhenu Deposit streams. The minimum deposit is INR 100 and the maximum is INR 1.50 lakh per person. |

Senior Citizen FD | Offers an additional 0.50% interest on eligible domestic term deposits below INR 3 crore for tenures of 180 days and above. |

Monthly Income FD | Canara Bank FDs allow monthly interest payout at discounted rates. Investors can also choose quarterly, half-yearly or annual payout options. |

NRE/NRO FD | NRI customers can open NRE and NRO deposits. NRE deposit interest is tax-free in India, while NRO deposit interest is taxable. |

Callable FD | Allows premature closure or part withdrawal, subject to the bank’s applicable penalty and conditions. |

Non-callable FD | Does not allow premature closure or part withdrawal. It is suitable for depositors who do not need liquidity before maturity. |

Source: Canara Bank5

How To Open Canara Bank FD Online?

Canara Bank Fixed Deposit can be opened online through net banking or mobile banking by customers who already have an active Canara Bank account. Customers who do not use digital banking can also open an FD by visiting a Canara Bank branch.

How to open Canara Bank FD through net banking?

Canara Bank customers with active internet banking can open an FD online without visiting the branch. The deposit amount is debited from the selected savings or current account.

- Step 1: Visit the official Canara Bank net banking portal and log in using your user ID and password.

- Step 2: After logging in, go to the deposits section. The option may appear as fixed deposit, term deposit, open deposit or online term deposit opening, depending on the net banking layout.

- Step 3: Select the account from which the FD amount has to be debited. This is usually the customer’s Canara Bank savings or current account. The account should have enough balance before the FD is booked.

- Step 4: Enter the deposit amount. The minimum deposit amount is INR 1,000. For regular fixed deposits, Canara Bank does not specify any maximum ceiling.

- Step 5: Choose the deposit tenure. The regular FD tenure ranges from 15 days to 120 months. If the single deposit amount is INR 5 lakh or more, a shorter tenure of 7 to 14 days may also be available.

- Step 6: Select the interest payout option. Canara Bank allows interest payout at monthly, quarterly, half-yearly or annual intervals, depending on the depositor’s choice. Monthly interest is usually paid at a discounted rate.

- Step 7: Choose the maturity instruction. Customers can select whether the maturity amount should be credited to the bank account or whether the deposit should be renewed, based on the options available on the portal.

- Step 8: Add nominee details. Nomination helps the nominee claim the deposit amount in case of the depositor’s death. If the nominee is already registered, the customer may be able to select the same nominee.

- Step 9: Review the FD details carefully. Check the deposit amount, tenure, interest payout option, maturity instruction, nominee details and debit account before confirmation.

- Step 10: Confirm the request using OTP, transaction password or any other authentication required by Canara Bank.

Once the FD is created, save or download the FD receipt. The deposit details can usually be viewed later through the deposits section in net banking.

How to open Canara Bank FD through mobile banking?

The mobile banking process is almost the same as net banking. The main difference is that the FD is opened through the Canara ai1 mobile banking app instead of the net banking portal.

To open an FD through mobile banking, log in to the Canara ai1 app and go to the deposits section. Select fixed deposit or term deposit, choose the debit account, enter the amount and select the tenure.

After that, choose the interest payout option and maturity instruction. Add or confirm nominee details, review the FD summary and complete the request using MPIN, OTP or the required authentication.

This method is useful for customers who prefer booking the FD directly from their phone.

How to open Canara Bank FD at a branch?

Customers who do not use net banking or mobile banking can open a Canara Bank FD by visiting the nearest branch.

At the branch, ask for the fixed deposit application form and fill in details such as name, account number, deposit amount, tenure, interest payout option, maturity instruction and nominee details.

Existing Canara Bank customers may be able to fund the FD from their savings or current account. New customers or customers with pending KYC updates may have to submit documents before the FD is opened.

After the request is processed, the bank will issue the FD receipt. Customers should check the name, deposit amount, interest rate, tenure, maturity date and nominee details on the receipt.

Documents required to open Canara Bank FD?

The documents required may differ for existing and new customers. Existing customers with updated KYC may not need to submit fresh documents while opening an FD online.

For branch-based FD opening, the following documents may be required.

- Application form in the bank’s prescribed format

- PAN card or Form 60 or 61 if PAN is not available

- 2 photographs of the depositor

- Proof of identity as per KYC norms

- Proof of address as per KYC norms

- Canara Bank account details for existing customers

Other documents for proprietorship concerns, partnership firms, companies, HUFs and other applicants, wherever applicable

Minimum deposit amount for Canara Bank FD

The minimum deposit amount for Canara Bank Fixed Deposit is INR 1,000.

There is no maximum ceiling under the regular fixed deposit scheme. However, the rules may differ for special deposit schemes, tax-saving deposits or non-callable deposits.

Things to check before opening Canara Bank FD

Before opening the FD, customers should check the latest interest rate for the selected tenure. The applicable rate is generally based on the rate available on the date of deposit booking.

Customers should also choose the payout option carefully. Monthly payout can help those who need regular income, while quarterly, half-yearly or annual payout may suit those who do not need monthly cash flow.

The maturity instruction should also be reviewed. If auto-renewal is selected, the FD may be renewed after maturity. If account credit is selected, the maturity amount will be credited to the linked bank account.

Interest earned from fixed deposits is taxable as per the depositor’s income tax slab. TDS may also apply as per prevailing income tax rules.

Taxation And Real Returns

Interest from Canara Bank FDs is fully taxable, and TDS is deducted at 10% when the total FD interest in a financial year exceeds INR 40,000 for regular customers and INR 50,000 for senior citizens (20% if PAN is not provided). Since tax reduces your actual earnings, the final yield may differ from the headline Canara Bank FD interest rates.

Using the Canara Bank FD calculator helps estimate post-tax maturity values. Inflation further impacts real returns. Long-term investors can explore Canara Bank tax saver FD rates, which offer Section 80C benefits (as per the old tax regime) but carry a five-year lock-in without premature withdrawal.

Canara Bank FD vs SBI FD vs HDFC FD

Canara Bank, SBI and HDFC Bank all offer fixed deposits across short, medium and long terms. The right choice depends on the interest rate, senior citizen benefit, minimum investment and whether the depositor wants a tax-saving product.

The table below compares key FD details across the three banks for retail domestic deposits below INR 3 crore.

| Bank | 1-year FD rate | 5-year FD rate | Senior citizen rates | Minimum deposit | Tax saver FD option |

| Canara Bank | 6.25% | 6.25% | 1 year: 6.75%; 5 years: 6.75% | INR 1,000 | Yes. Canara Tax Saver FD has a 5-year tenure, minimum deposit of INR 100 and maximum eligible deposit of INR 1.5 lakh under Section 80C. |

| SBI | 6.25% | 6.05% | 1 year: 6.75%; 5 years: 7.05%, including SBI We-care benefit | INR 1,000 | Yes. SBI Tax Savings Scheme has a 5-year lock-in, minimum deposit of INR 1,000 and maximum deposit of INR 1.5 lakh in a year. |

| HDFC Bank | 6.25% | 6.40% | 1 year: 6.75%; 5 years: 6.90% | INR 5,000 | Yes. HDFC Bank Five Year Tax Saving FD has a 5-year lock-in, minimum investment of INR 5,000 and maximum eligible deposit of INR 1.5 lakh in a financial year. |

Best FD Alternatives For Higher Returns

Corporate fixed deposits have become a practical alternative for investors seeking better returns than traditional bank FDs. These deposits are issued by reputable NBFCs and corporates and offer fixed tenures, predictable interest payouts, and clearer visibility on credit quality through accredited ratings. For many investors, they provide an FD–like structure with comparatively higher yield potential.

As bank FD rates softened in 2025, corporate FDs can help bridge the gap between stability and returns. They come with flexible payout options, medium-term maturities, and transparent issuer disclosures, allowing investors to assess risk before committing funds. For those with low to moderate risk appetite, corporate FDs serve as an income-generating tool without the volatility associated with market-linked products.

Grip Invest makes it easy to explore curated corporate FDs from credible issuers. Each listing undergoes detailed evaluation, helping investors compare yields, tenures, and issuer profiles in one place. If you are looking to diversify beyond conventional fixed deposits while keeping your portfolio focused on fixed income, corporate FDs available on Grip can be a suitable option.

Also Read: TDS On FD Interest Explained: Rules, Rates, And How To Avoid Excess Tax

Conclusion

Fixed Deposits have remained an extremely popular investment for investors looking for consistent returns without taking too many risks. FDs have helped millions of investors in attaining their long-term financial goals. It is important to note that with changes in monetary policies, the actual and real interest rates have declined, and FDs might be insufficient in beating inflation or being an effective investment asset.

With rising inflation and shifting interest-rate cycles, it’s equally important to compare post-tax and real returns with other fixed-income options. Evaluating corporate bonds and similar alternatives can help investors balance safety with stronger long-term performance.

Visit Grip Invest today!

FAQs On Canara Bank FD Rates

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001