Taxation Of Market-Linked Debentures (MLDs) In 2026: Here Is What Has Changed

Introduction

Market-linked debentures (MLDs) have become increasingly popular as investment instruments that offer potential returns based on the performance of an underlying market benchmark. While MLDs provide investors with unique opportunities, there is a need to have a comprehensive understanding of market linked debentures taxation.

In this blog, we will explore the taxation of MLDs in India, changes implemented in the Finance Act 2023 especially the implementation of Section 50AA, and shed light on key investor considerations when assessing MLDs in 2026.

Taxation Provisions In Respect Of MLDs (Before April 01, 2023)

MLDs have gained significant popularity among investors due to shorter holding periods for being entitled to lower capital gains tax rates. According to Section 2(42A) of the Income Tax Act, listed securities, including MLDs, are subject to a holding period of 12 months for determining capital gains instead of the standard 36 months applicable to unlisted securities. The gains from MLDs with a holding period of 12 months or more are treated as Long-Term Capital Gains (LTCG) and taxed at 10% plus a surcharge.

- Gains arising on the transfer of a listed MLD after a period of 12 months but before its maturity period are treated as Long Term Capital Gains and are subject to the applicable tax rate of 10% plus applicable surcharge, just like any other listed debt security.

- In cases where the MLD has not been transferred before its maturity, the investor gets back the principal amount plus interest at the time of redemption(subject to the fulfilment of the market-linked condition). This is the interest income and is taxable in the hands of the investor like all other interest income at the applicable tax slab rate of the investor.

- Overall, the tax advantage does not apply to MLDs transferred or redeemed on or after the 1st of April. 2023.

Also Read: Rise In STT After The Budget: What The Securities Transaction Tax Hike Means For Investors

Tax Advantage On MLDs Compared To Plain-Vanilla Debt Instruments

Before April 1, 2023, a meaningful tax advantage was enjoyed by market-linked debentures over plain-vanilla debt instruments, including bank fixed deposits and non-convertible debentures (NCDs).

Annual taxation on interest income is applicable at the investor’s income tax slab rate in the cases of traditional debt instruments and FDs. Comparatively, the listed MLDs, which are held for more than 12 months, have qualified as long-term capital gains. They were taxed at a concessional rate of 10%.

The distinct treatment helps investors with high tax brackets to optimise post-tax returns by holding MLDs beyond the short holding period threshold.

How The Advantage Changed After 2023: MLD Vs FD

The tax arbitrage was removed under the Finance Act in 2023 by introducing Section 50AA. This brought all gains from market-linked debentures under short-term capital gains taxation regardless of the holding tenure. Due to this, MLD returns are now taxed at the investor’s suitable slab rate. This is similar to interest earned on fixed deposits and most non-convertible debentures.

While FDs continue to offer predictable, low-risk return slab rates, MLDs now justify their inclusion through higher pre-tax return potential, market-linked upside, or specific payoff structures instead of tax efficiency alone.

The tax gap between MLDs and plain-vanilla debt instruments has narrowed considerably. This is applicable for investors with higher tax brackets, making product structure and aligning risk-return crucial compared to tax treatment when making allocation decisions in 2026.

Changes In Taxation Of MLDs As Per The Finance Bill 2023

Section 50AA And Its Objective

There was a fundamental shift in the taxation framework for market-linked debentures in accordance with the enactment of the Finance Act 2023. The reason behind introducing the amendment was to curb tax arbitrage arising from structured debt products that were economically similar to fixed-income instruments, enjoying seasonal capital gains taxation.

Holding Periods No Longer Relevant For MLDs

Any gains from the transfer, redemption, or maturity of market-linked debentures are treated as short-term capital gain under the post-2023 regime. This is applicable irrespective of the duration for which the instrument is held. The tax treatment remains the same regardless of whether an investor exists an MLD after a few months or holds it until maturity over several years.

Example Of MLD Taxation After April 1, 2023

Understanding the practical impact of the changes is important and can be done using examples. Let's consider an investor who purchases an MLD for INR 10,00,000 and receives INR 11,50,000 after redemption. The gain is treated as a short-term capital gain. The entire gain is taxed at 30% if the investor falls under the 30% income tax slab.

With this example, we can see how the post-2023 tax regime removes any incentive to hold MLDs for longer durations.

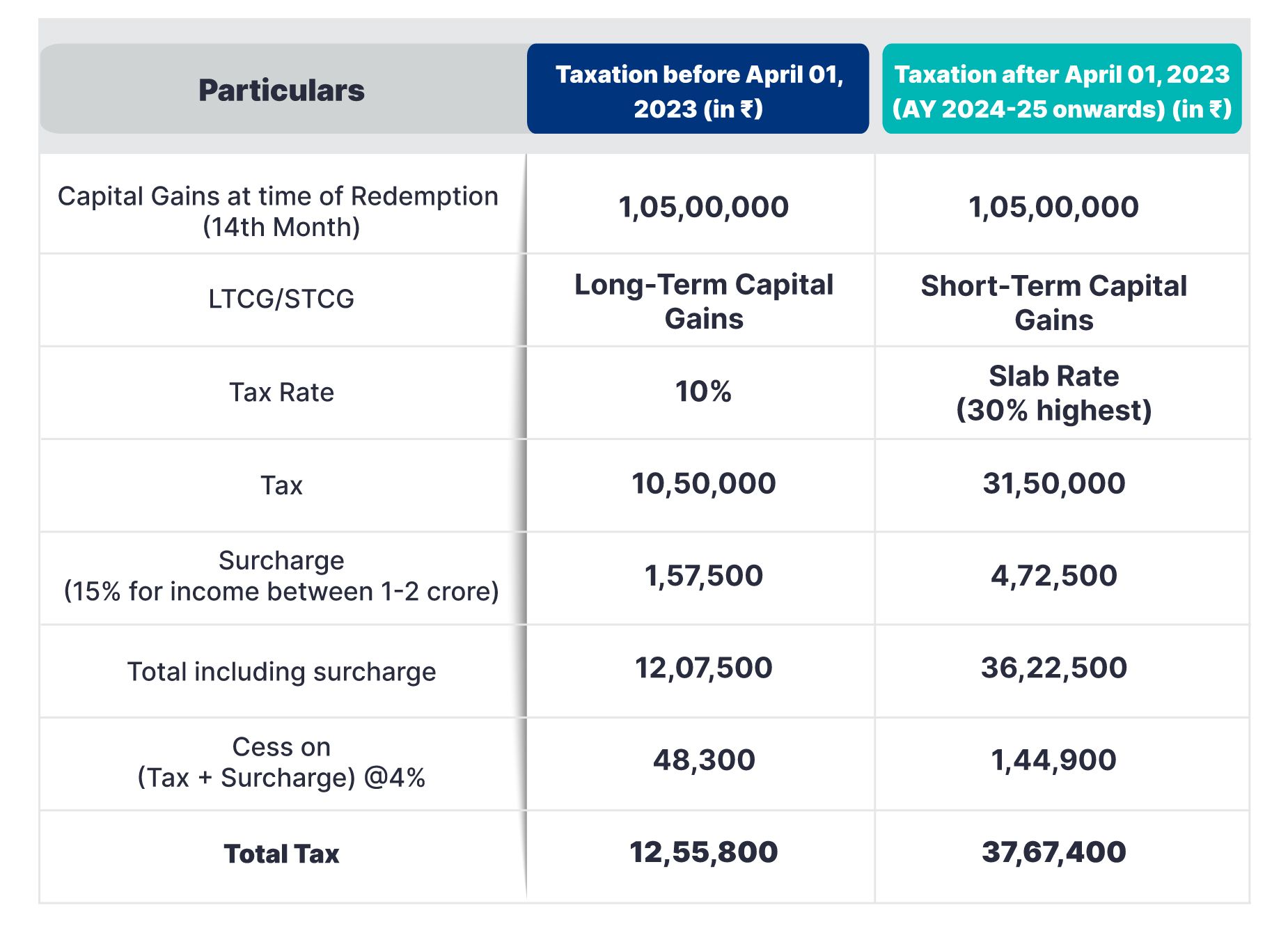

Example To Understand The Taxation Before And After April 01, 2023

Let us take a simple example to understand post-tax returns before and after the tax changes.

- XYZ Ltd. issues MLDs linked to ‘Government Bonds maturing in 2030’ and pays a 9% per annum coupon maturing in 14 months.

- 9% is only given because the ‘Government Bond maturing in 2030’ does not fall 25% in price in the 13th month.

- If the government bond has fallen 25%, only principal protection is there, and you get no interest.

- Say you invested INR 10 crores in MLDs and sold them before maturity, realizing a gain of 9%, which amounts to INR 1.05 crores

Assumptions

- Investor redeemed the MLDs just before maturity.

- The redemption amount will be a little lower, but for ease of calculation, we assume it to be a round figure.

- For ease of understanding, expenses related wholly or exclusively to the transfer or redemption of MLDs have been ignored.

Also Read: What Is Debenture Redemption Reserve And Why It Matters?

Tax Deduction At Source (TDS) On MLDs

Clause (ix) of the Proviso to section 193 of the Income Tax Act provides an exemption from the requirement of deductions of TDS on any interest income arising on a listed debt security. The aforesaid section provides no tax deduction for any interest payable on any security issued by a company where such security is in dematerialised form and is listed on a recognized stock exchange in India under the Securities Contracts (Regulation) Act, 1956.

Finance Minister Nirmala Sitharaman, in the Budget 2023-2024, announced the removal of this exemption from TDS. This is because ‘there is under-reporting of interest income by the recipient due to above TDS exemption. Hence, it is proposed to omit clause (ix) of the Proviso to section 193 of the Act. 4. This amendment will take effect from 1st April 2023,’ read the finance bill.

However, TDS is deducted at source in interest payouts post April 1, 2023. Investors must still compute and pay the final tax liability based on their applicable income slab while filing returns.

No Grandfathering Relaxation

It is important to highlight the tax treatment of considering the transfer of market-linked Debts (MLDs) as short-term capital gain in all cases and taxing them at the higher tax rate as per the slab rate of the investor. The implementation is without any grandfathering relaxation for existing MLDs held in investors' portfolios before April 1, 2023. The Finance Bill 2023 does not propose any exemption or special treatment for MLDs acquired before this date.

Consequently, for MLDs acquired before April 1, 2023, any gains resulting from their transfer, redemption, or maturity will also be subject to this provision.

Post-Tax Returns Comparison: MLD Vs FD Vs NCD

| Factors | MLDs | FDs | NCDs |

| Return Type | Market-linked | Fixed | Coupon-based or Fixed |

| Tax Treatment | STCG at slab rate | Interest tax based on slab rate | Interest tax based on slab rate |

| Benefit of Holding Period | None | None | None |

| Post-tax return | High | low | moderate |

| Risk Return | Moderate | Low | Moderate to low |

| Best Suited | Return-seeking investors | Capita; safety seekers | Yeild-focused |

Explore Grip Invest to make your investment journey easier.

MLDs In 2026: Are They Still Worth It? (Risk-Return Analysis)

The role of market-linked debentures has been significantly altered following tax changes introduced under the Finance Act, 2023. MLDs are no longer evaluated primarily as tax-efficient debt instruments due to the removal of long-term capital gains benefits and the application of slab-based taxation under Section 50AA.

MLDs continue to offer pre-tax yields in comparison to traditional debt instruments, including FDs and plain-vanilla non-convertible debentures. MLDs are not guaranteed, unlike fixed-income instruments. Investors must be comfortable with conditional payouts and limited downside protection in certain scenarios.

MLDs may still be worth considering in 2026, especially for investors with a greater risk tolerance. They understand structured products and seek enhanced risk potential beyond traditional debt instruments. However, MLDs should be seen as a return-enhancement tool instead of a tax-saving instrument and should be evaluated with caution within a diversified instrument portfolio.

FAQs On Tax Implications Of Market Linked Debentures

1. How are gains from market-linked debentures taxed now?

From April 2023, MLD gains are taxed as short-term capital gains at your slab rate, regardless of holding period.

2. Why don’t longer holding periods cut my tax on MLDs anymore?

Earlier, holding beyond 1 year gave a 10% long-term tax. Now, all gains are short-term, removing the benefit of holding longer.

3. What happened to the 10% long-term tax benefit on MLDs?

It was removed in Budget 2023 to prevent tax arbitrage between MLDs and other debt instruments.

4. Is TDS now applied when I get maturity or redemption proceeds from MLDs?

Yes, issuers deduct TDS at payout, and you must report the income under capital gains in ITR.

5. Will MLDs bought before April 1, 2023, face the new tax rules?

Yes, even older MLDs sold or redeemed after April 1, 2023, are fully taxable under the new rules.

6. How is my gain from an MLD calculated for tax purposes?

Your gain is the difference between the sale/redemption value and the purchase cost, taxed as short-term income.

7. Is there any indexation benefit on MLDs now?

No, indexation benefits do not apply—your entire gain is taxable at the applicable slab rate.

8. Why did the tax rules change for MLDs?

The government aimed to simplify debt taxation and prevent the misuse of structured products for lower taxes.

References:

- Ministry of Finance <https://tinyurl.com/mrxy63pv>

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.