Volatility Vs Risk: Understanding The Difference Before You Invest

A lack of nuanced analysis of financial theories and asset performance often causes a wrongful parity between volatility and risk, as investors use the former as an indication or proxy of the latter. Moreover, behavioural finance amplifies this inconsistent volatility vs risk understanding. A short-term volatility triggers our loss aversion and makes a drop feel catastrophic, resulting in investors ignoring historic performance records and reacting to short-term movements.

Although volatility vs risk in investing is often equated as similar or related concepts, they measure different phenomena. While volatility explores price fluctuations, risk refers to a permanent capital loss. Therefore, optimal portfolio risk management is untenable without a complete understanding of risk and market volatility, along with their interplay.

What Is Volatility In Investing?

The first step to decoding volatility vs risk is to understand their individual meaning.

In finance, volatility measures the frequency and degree of price change in assets. Simply put, it measures how often and how much the market price of a financial instrument changes over time. Measured through metrics like standard deviation, annualised volatility, etc., volatility helps make sense of stock market fluctuations and short-term price movements.

High volatility indicates uncertainty caused by large and frequent swings, while low volatility means prices are more stable, giving an anticipation of expected returns and portfolio stability to investors. However, it is also important to note that, unlike fixed-income assets like FDs, price movements are essential to stock market gains since they are the primary mechanism for generating profit through capital appreciation.

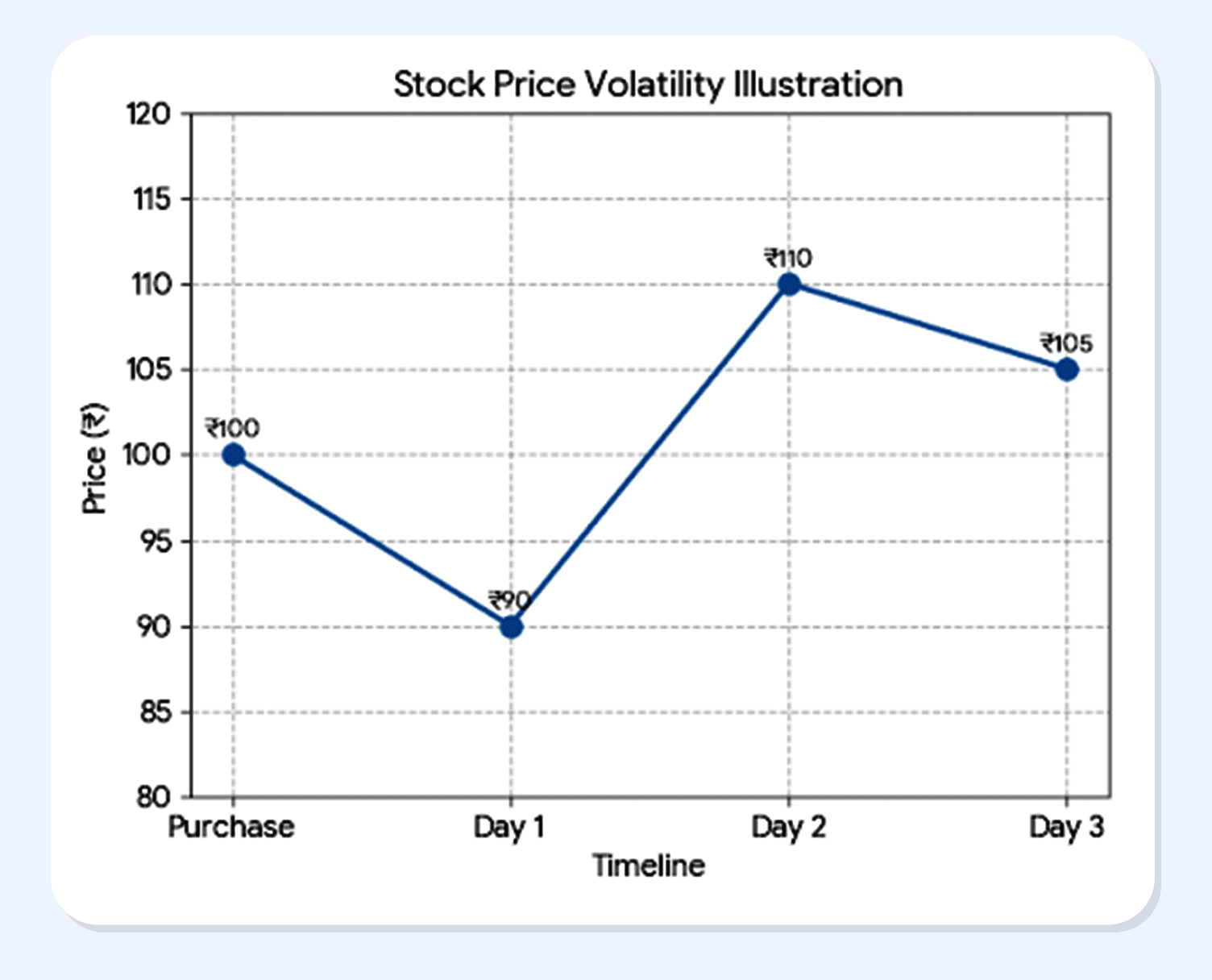

For instance, suppose Mr A invested INR 100 in stocks. On Day 1, his equity investment fell to INR 90 and then on Day 2 it reached INR 110. Finally settling on INR 105 on Day 3. His standard deviation in this short-term window is around 17.25%, indicating high volatility.

Therefore, while volatility is popularly considered an indication of risk, there is a caveat to it. To understand why asset volatility does not always reflect real investment risk, understanding market volatility meaning is not enough. An analysis of risk as a concept is equally important.

What Is Risk In Investing?

The possibility of a permanent loss of capital in investing, when the value of the investment in question drops with no anticipation of recovery, is called risk. For example, Mr K invests INR 10,000 in the stock market. If he actually loses INR 5,000, it is a capital loss. The chance that he might lose INR 5,000, however, is a risk.

Risk is a cost of return. When investors invest in an asset, the risk they run of their capital being lost yields the return. Therefore, when returns increase, the risk increases. For instance, equity assets give higher returns than FD, resulting in a higher risk.

Furthermore, there are different types of risks in investing. A brief look at them below is crucial to decode the investment risk meaning.

1. Business Risk: Failures or downturns in the business of the investment issuer can impact the investment and cause capital loss. For instance, if K bought stocks of XYZ company that is incurring consistent losses despite a good industry performance, the market price of his stocks can fall, resulting in a loss.

2. Credit or Default Risk: Unlike equity investments, which represent partial ownership, investment in debt securities makes investors a creditor of the issuer. If the issuer fails to repay the capital, the issuer will suffer a loss.

3. Market Risk: An overall impact in financial markets, like economic downturn, political instability, etc., can cause investment loss across assets and sectors. For instance, from Q1 of 2007 to Q2 of 2011, the home prices in the US fell by over a fifth on average, marking the 2008 Financial Crisis1. However, the impact of this historic crisis was not limited to housing; it impacted mortgage-related assets, asset-backed commercial paper, money market instruments, etc.

4. Liquidity Risk: In the case of certain assets, investors might not be able to liquidate their investment quickly, without substantial loss. For instance, selling off a real estate asset during a slump can cause substantial loss.

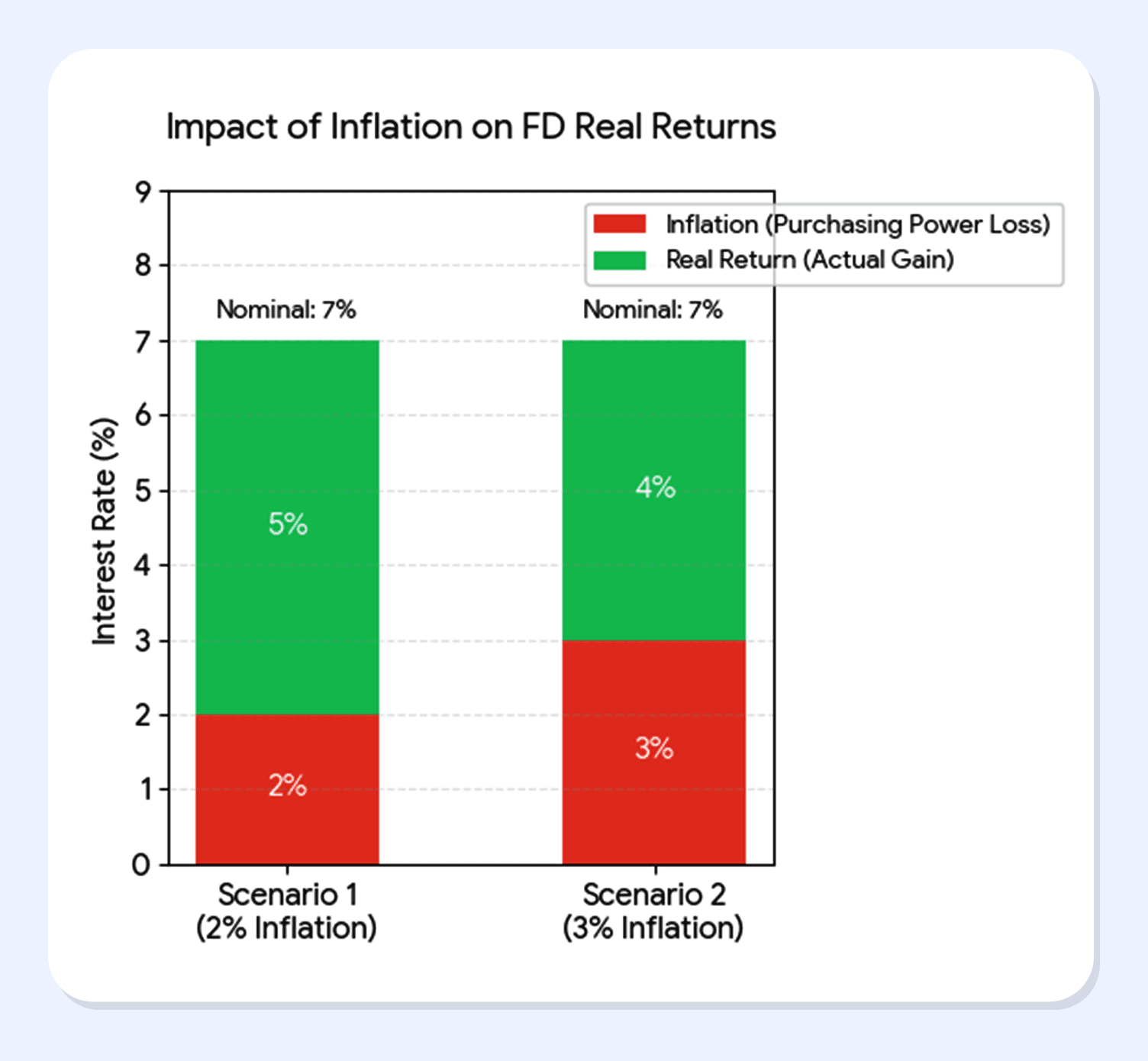

5. Inflation Risk: Rising inflation corrodes the return available to an investor. For instance, if Mr P invests in an FD that gives 7% interest. When inflation is at 2%, his real return would be 5%. However, if inflation increases to 3%, his real return rate will fall to 4%.

Therefore, while risk is an anticipation of capital loss, volatility is a fluctuation in prices. The comparison between risk vs volatility in stocks, fixed-income assets, and others is integral in optimal risk analysis.

Volatility Vs Risk: Key Differences Explained

A comprehensive comparative analysis of risk and volatility is essential for a nuanced understanding of the two parameters and their relation in gauging asset investibility. The table below aids in the said analysis.

| Parameters | Volatility | Risk |

| Meaning | Measures the degree and frequency of asset price fluctuations | Probability of capital loss when the asset price falls without any recovery |

| Time Horizon | Mostly short-term and can be recovered | Indicates long-term downturn with little to no scope of recovery |

| Outcome | Temporary dips and recovery | Consistent dip with no scope of recovery |

| Impact | High volatility can cause panic selling, adversely impacting long-term returns | Risk can cause financial loss, capital erosion, etc. |

| Measurements | Annualised standard deviation, beta, etc. | Credit rating, downside scenarios, drawdown depth, etc. |

The difference between volatility and risk becomes clearer when we understand how high volatility can often not result in high risk.

Why High Volatility Does Not Always Mean High Risk

Volatility is a key trait of markets. Short-term market volatility can ease over time as the market recovers and generates anticipated returns. Therefore, a high market volatility does not automatically indicate risk. As discussed, risk refers to potential capital loss with no recovery. However, if the high volatility of an asset is short-term and it recovers over time, the asset no longer remains risky.

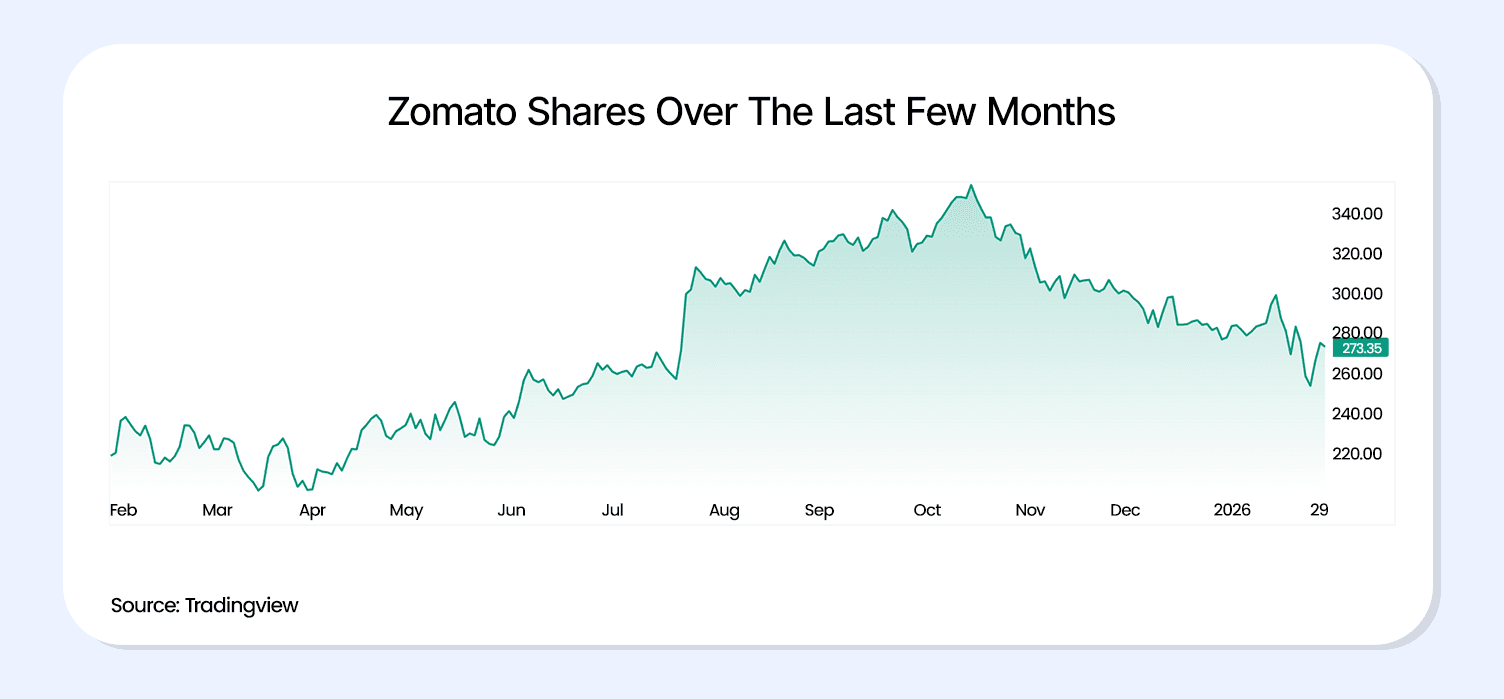

For instance, in July 2022, the shares of Zomato (now known as Eternal) plummeted more than 14%2. However, a look at its one-year performance shows a positive return of 22.60% as of 30 January 20263.

Therefore, since short-term volatility does not guarantee long-term capital loss, panic-selling of assets due to high short-term volatility can disrupt investment plans. Holistic analysis through metrics like risk-adjusted returns, along with decoding the risk-volatility relation in impact on a particular asset, can aid decision-making.

How Volatility And Risk Affect Different Asset Classes

While market-linked assets like mutual funds and equity encounter greater volatility, fixed-income investments witness little to no fluctuations. For instance, while the market value of bonds can fluctuate, the fixed deposit principal cannot.

Therefore, due to this intrinsic nature, despite short-term or long-term investing volatility, market assets have a higher risk and return compared to fixed-income assets, as illustrated in the table below.

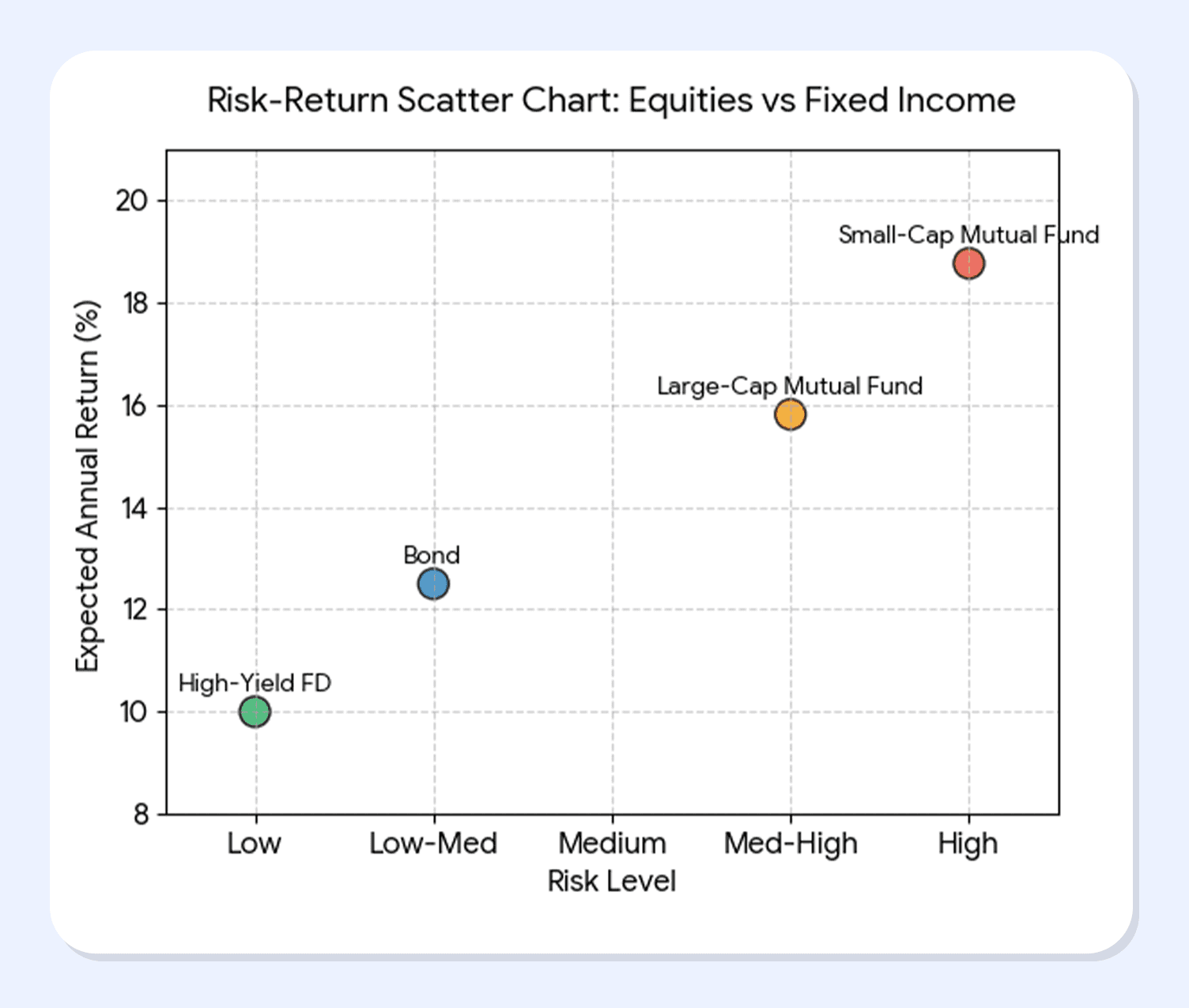

According to the scatter diagram, while a large-cap mutual fund can have medium to high risk, its 3-year category average performance is at 15.81%4, as of 29 January 2025. Small-cap funds, on the other hand, have delivered a 3-year category performance of 18.76%, as of the same date, but they can have high-risk metrics.

However, bonds and high-yield FDs can offer up to 12.5% and 10% return, respectively, on Grip with a low to medium risk profile. Therefore, portfolio diversification and optimal asset allocation are key to balancing portfolio stability and investment growth.

Grip offers a range of assets, including bonds that can offer up to 12.5% return.

Conclusion

Understanding the difference between volatility and risk is essential for making informed investment decisions. While volatility reflects short-term price movements, risk represents the possibility of permanent capital loss. Confusing the two can lead to reactive choices such as panic selling during temporary market swings, which often hurts long-term returns. A clearer view of both concepts helps investors focus on fundamentals, time horizon, and risk-adjusted outcomes rather than short-term noise.

By balancing market-linked assets with relatively stable fixed-income instruments, investors can manage uncertainty more effectively and build resilient portfolios. Platforms like Grip Invest make it easier to explore diversified fixed-income options, including bonds, helping investors align risk, return, and long-term financial goals with greater clarity.

FAQs On Volatility Vs Risk In Investments 2026

1. Is volatility the same as risk in investing?

No. Volatility shows how much prices move in the short term, while risk refers to the possibility of permanent loss of capital.

2. Does high volatility always mean an investment is risky?

Not necessarily. If price fluctuations are temporary and the asset recovers over time, high volatility may not result in real risk.

3. Why do equity investments feel riskier than fixed deposits?

Equities experience frequent price movements and higher uncertainty, while FDs offer stable returns with minimal price fluctuation but lower growth potential.

4. How can investors manage volatility and risk together?

By diversifying across asset classes, focusing on long-term goals, and evaluating investments using risk-adjusted returns instead of short-term price movements.

References:

1. Fedral Reserve, accessed from:

https://www.federalreservehistory.org/essays/great-recession-and-its-aftermath

2. Economic Times, accessed from:

https://economictimes.indiatimes.com/markets/stocks/news/zomato-plummets-14-hits-record-low-after-lock-in-for-613-crore-shares-ends/articleshow/93102194.cms?from=mdr

3. Trading View, accessed from:

https://in.tradingview.com/symbols/NSE-ETERNAL/?timeframe=12M

4. Morning Star, accessed from: https://www.morningstar.in/tools/mutual-fund-category-performance.aspx

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001