Risk Tolerance Vs Risk Capacity: Understanding The Difference Before You Invest

The paradox of investing lies in one’s ability to handle the risk associated with returns. Whether emotional or practical, this largely depends on how you view your finances when stepping into a space that often triggers anxiety.

Many investors assume that simply knowing when to be aggressive or conservative, or diversifying across asset classes, is enough. However, the reality is more nuanced. A proper assessment of risk capacity is essential.

Investors frequently make costly mistakes, such as panic-selling during market downturns or overexposing themselves to high-risk assets without a financial safety net. This is why understanding risk tolerance vs risk capacity becomes critical when making investment decisions, especially when markets test both patience and financial stability.

Today, several platforms offer in-depth tools for investment risk assessment, helping investors navigate volatility with greater confidence. These tools highlight mismatches between perceived and actual risk-taking, a gap that has become more evident in recent years as participation in equities and mutual funds has surged and market movements have intensified.

What Is Risk Tolerance?

Risk tolerance refers to the investor’s ability to endure market fluctuations without panic or concern. An investor’s overall personality, previous experiences, and their response to financial stress influence it. Fears and confidence levels also play a role. It reflects the emotional readiness to remain calm during market changes.

A study shows that loss aversion impacts the psychology of Indian investors more than the positive market shift. SEBI investor survey data show that in India, many first-time investors tend to overestimate their risk tolerance during Bull Markets and underestimate it during downturns1. This shift in perception is why financial advisors commonly use a risk tolerance questionnaire to assess how they would react to a hypothetical loss, how comfortable they are with volatility, and whether they would remain calm in the near future.

Risk Tolerance is not constant. It can change as people change, age, have different life experiences, see other things happen in the economy/markets, and even experience gains/losses over time. Therefore, behavioral risk investing will always remain a significant component of long-term investment success.

What Is Risk Capacity?

In comparison, risk capacity calculation is not based on emotions but rather on your financial ability to take on risk without jeopardizing your fundamental objectives. Risk capacity assesses your income stability, asset accumulation, outstanding liabilities, duration before asset utilisation, and future expenses.

Therefore, risk capacity calculation determines whether you can recoup any losses incurred during a bear market.

Calculation of risk capacity usually incorporates factors such as: debt-to-income ratio; degree of liquidity; investment horizon, and any dependent obligations. Financial advisors in India commonly recommend taking less equity risk as one nears their investment goal, regardless of how comfortable they may feel emotionally with this level of equity risk.

It blurs the distinction between evaluating risk appetite vs capacity India when making decisions related to goal-oriented investing, such as children's educational expenses or retirement funding.

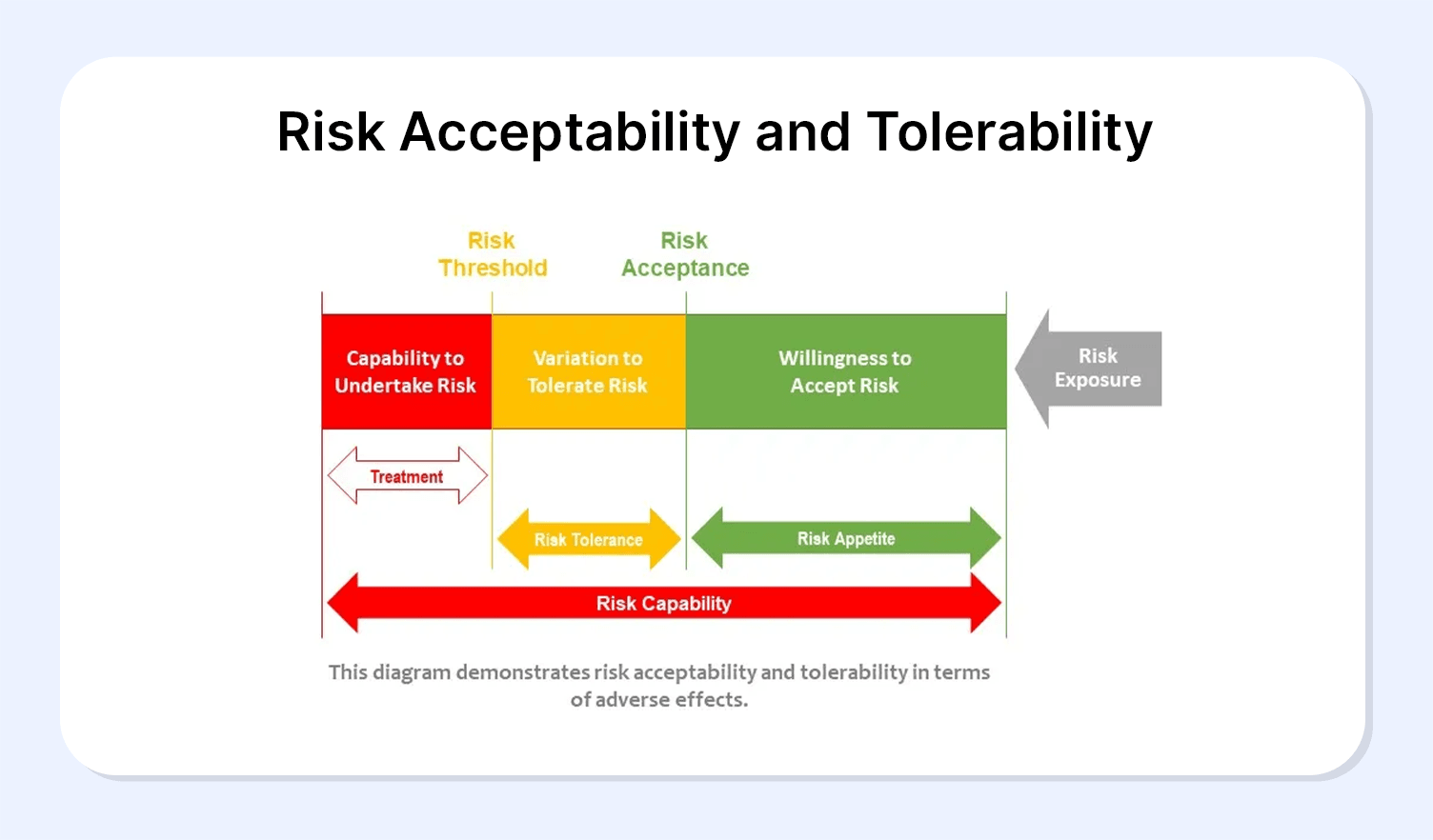

Risk Tolerance Vs Risk Capacity: Key Differences

The difference between risk tolerance vs risk capacity lies in psychology rather than financial reality. Here is a table showing the difference between the two

| Basis | Risk Tolerance | Risk Capacity |

| Meaning | Emotional comfort with investment risk | Financial ability to take investment risk |

| Nature | Psychological and behavior-based | Financial and numbers-based |

| Focus | Feelings about volatility and losses | Ability to absorb losses |

| Measurement | Assessed through risk tolerance questionnaires | Calculated using income, savings, and obligations |

| Time horizon impact | May not change with time | Improves with a longer time horizon |

| Stability | Can change frequently | Changes slowly over time |

| Market reaction | Affects panic or patience during downturns | Affects long-term financial survival |

Why Both Matter In Portfolio Building

Portfolio risk planning will not work when either risk capacity or risk tolerance is disregarded. When a particular portfolio is constructed based on the capacity to take risks, it might appear optimal in mathematical analysis.

However, it will lead to emotional strain, resulting in poor timing choices. On the other hand, risk-only portfolios can subject investors to losses beyond their capabilities.

Historical data can support this2. During the March 2020 market crash, retail investors were heavily redeeming equity mutual funds even though those funds could recover over the long term. Most of these investors were technically prepared to have enough risk capacity, but were not emotionally ready.

Such action led to the irreparable loss of capital through the exit at market lows. Risk profile investing is most effective when there is equity between emotional ruggedness and financial capabilities.

A balanced portfolio recognises that risk is not only associated with maximising returns. It is concerning being invested in cycles. Therefore, portfolio risk planning focuses on discipline over market timing and the importance of asset allocation in minimizing the stress of volatility.

Aligning Risk With Investment Choices

Fitting the risk with appropriate investment instruments is where theory and practice meet. Equity investments are more volatile and promise long-term growth. Stable assets such as bonds, debt funds, and predictable-income assets help mitigate downside risk across high-, moderate-, and low-risk investments.

The portfolio shocks of moderate-risk and high-quality debt instruments should be reduced to a greater extent than the growth of the portfolio of high-risk investors with moderate risk capacity.

According to AMFI statistics in India, hybrid funds have become popular for their ability to provide emotional comfort and help overcome financial limitations3.

Predictable-income assets, such as government bonds, fixed deposits, and goal-oriented maturity funds, are particularly stabilising for goal-oriented investments. These tools enable investors to invest in growth assets without putting the whole portfolio at risk of equity risk.

Profiling investments also presupposes periodic risk assessments.

Life changes, such as marriage, a change of career, or health changes, change the risk capacity, whereas market experiences change the risk tolerance.

As we noted in our blog post on investment risk assessment basics, it is always a good idea to review your risk profile after 2 to 3 years to keep your portfolio relevant.

Going Beyond Basics

One thing that risk tolerance and risk capacity people fail to notice is how market cycles affect decision-making. In long-term bull markets, investors are likely to overestimate both their tolerance and their capacity.

Behavioural studies have demonstrated that confidence increases with portfolio value, leading to excessive risk-taking. The converse occurs during bear markets, and investors undermine their ability to recover.

This repetitive action behaviour supports the role of systematic risk profiling and not intuitive decisions. Emotional judgments may be avoided by using past data, conducting stress tests on portfolios, and being aware of what can go wrong.

Behavioral risk investing aims to create portfolios that are stickable rather than those that appear optimal in good times.

Conclusion

Understanding the difference between risk tolerance and risk capacity is what separates short-term reactions from long-term investing discipline. When emotional comfort and financial ability are aligned, investors are far more likely to stay invested through market cycles and avoid costly, panic-driven decisions.

Platforms like Grip Invest help bridge this gap by offering access to predictable, well-structured investment options that support balanced portfolio construction. By combining data-driven insights with a clear view of cash flows, timelines, and goals, investors can build portfolios that not only look good on paper but also feel sustainable in real life.

FAQs

1. Can risk tolerance and risk capacity be different for the same investor?

Yes. An investor may feel comfortable taking high risk emotionally but lack the financial capacity to absorb losses, or have strong capacity but low emotional tolerance for volatility.

2. How often should investors reassess their risk tolerance and risk capacity?

A reassessment every 2 to 3 years is ideal, or sooner if there are major life changes like marriage, career shifts, or significant market experiences.

3. Which matters more while building a portfolio: risk tolerance or risk capacity?

Neither works alone. A sustainable portfolio balances both, ensuring investments are financially feasible and emotionally manageable through market cycles.

References:

1. SEBI, accessed from: https://www.sebi.gov.in/reports-and-statistics/research/sep-2025/investor-survey-2025_96982.html

2. BHU, accessed from: https://www.bhu.ac.in/Images/files/BMReview-Vol_8-P58-62.pdf

3. TOI, accessed from: https://timesofindia.indiatimes.com/city/pune/amfi-data-shows-rise-in-hybrid-funds-inflow-in-may/articleshow/122263661.cms

4. Economic times, accessed from: https://economictimes.indiatimes.com/wealth/invest/risk-tolerance-or-risk-capacity-which-one-should-guide-your-investments/what-is-risk-tolerance-your-emotional-comfort-with-volatility/slideshow/125973182.cms

5. Angle one, accessed from: https://www.angelone.in/news/mutual-funds/hybrid-mutual-fund-inflows-surge-46-percent-in-may-here-is-why

6. CNBC, accessed from: https://www.cnbc.com/2023/09/08/why-investors-need-to-know-about-risk-tolerance-and-risk-capacity.html

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.