Target Maturity Funds In India 2026: Predictable Returns, Lower Volatility

There is a reason why maintaining an individual portfolio, attaining short and long-term financial goals, and tax planning is known as ‘personal financial management’. Every individual has different goals, aspirations, risk appetites, and investment philosophies. Financial products are designed to ensure that the outlooks and perceptions of various individuals are taken into account. Even though the products are highly regulated and have a strict structure, there is also tremendous flexibility in the choices available for portfolio management and investment decisions.

One such concept is Target Maturity Funds, which could be best described as an instrument positioned between traditional debt funds and fixed deposits. These funds provide goal-linked returns without exposing investors to excessive market volatility. As bond yields stabilise in 2026, these funds are attracting interest from investors seeking a clearer view of potential outcomes across 3–7-year horizons.

Further, these could be an excellent addition to your portfolio for diversification and medium to long-term financial planning.

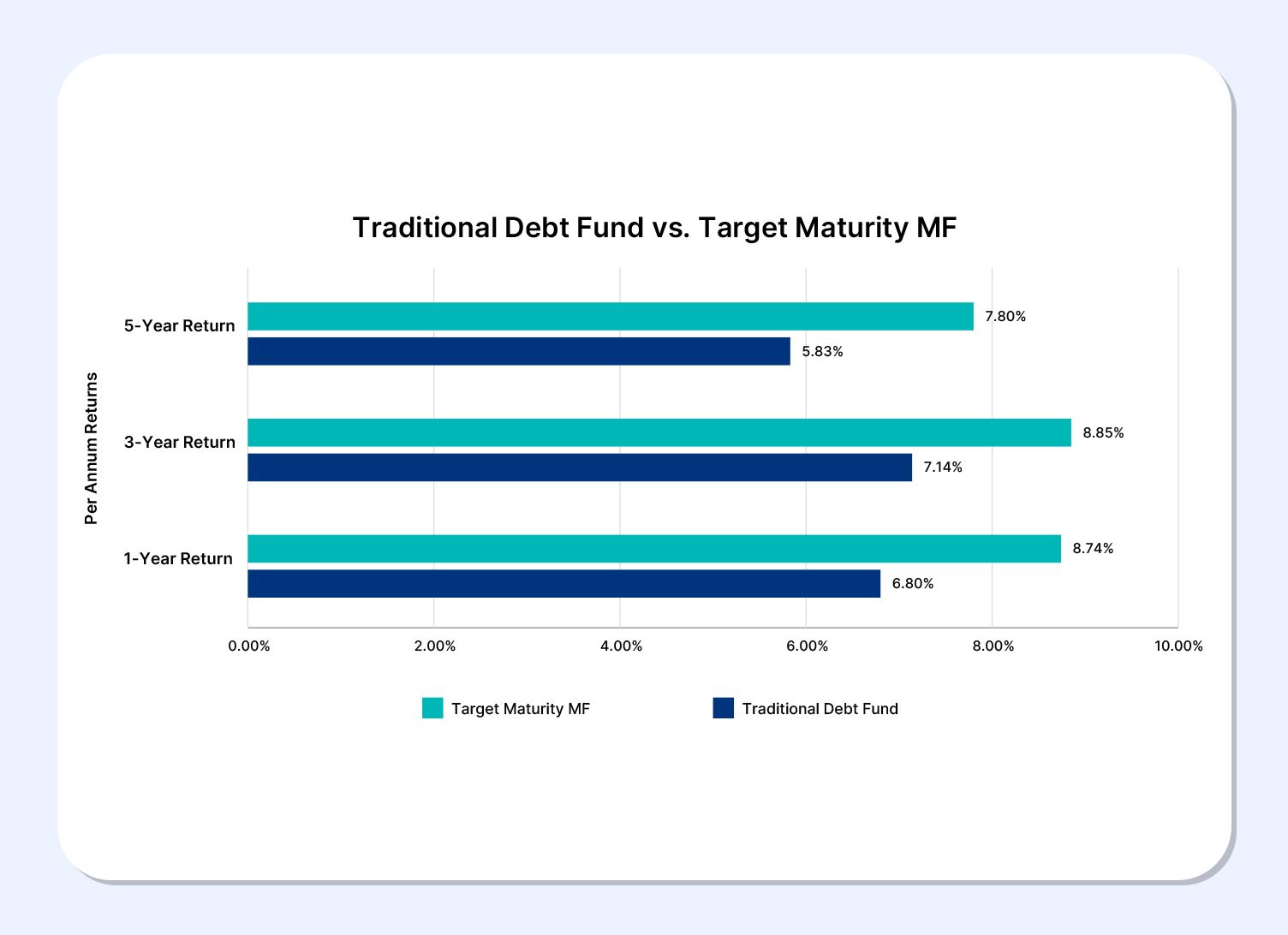

There is a wide range of Asset Management Companies offering both traditional debt funds and the best target maturity funds in India. Here is a chart showing the comparison of the most popular debt fund with the target maturity mutual fund:

How Target Maturity Funds Work

Figure 1.0 shows that target maturity funds provide a slightly higher return than traditional debt funds, with less risk for investors. These funds have a simple, predictable structure that provides investors with greater clarity about potential outcomes. The funds invest in government securities, state development loans or high-quality corporate bonds that all mature around the same date.

As the portfolio components have defined maturities, the fund's NAV converges toward the final proceeds as the maturity date approaches. Most TMFs track a specific bond index, making them a passively managed product with lower costs and minimal portfolio churn. This also ensures that the fluctuations in interest rates can be minimised during the investment journey.

Investors also gain better visibility on the yield-to-maturity (YTM) at the time of investment, which acts as a reasonable indicator of target maturity fund returns. However, the key is to remain invested throughout the maturity period of the fund.

Why Investors Prefer Target Maturity Funds

Investors can prefer TMFs in a medium to long-term financial planning scenario, especially when they have a specific goal in mind. These funds ensure a slightly higher return than the debt index fund India without exposure to market volatility. Further, TMFs are an excellent source of adding portfolio diversification.

Here are three main reasons why investors prefer TMFs:

1. Predictable Maturity Value

One of the biggest advantages of Target Maturity Funds is the visibility of returns. Since investments are made in high-quality bonds, investors can expect overall fund returns close to the YTM of the portfolio at the time of investment. This predictability makes TMFs ideal for those seeking stable and target maturity fund returns without worrying about short-term market volatility.

2. Lower Duration and Interest Rate Risk

Traditional debt funds can fluctuate based on interest rate movements. However, TMFs largely mitigate this by following a “hold-to-maturity” approach. As the maturity date nears, the duration and interest rate sensitivity reduce, offering a smoother investment journey.

3. Tax Efficiency and Indexation Benefits

For the investments made before April 1, 2023, there were indexation benefits available under the capital gain taxation regulations (if the holding period is more than three years), reducing the overall tax liability of an individual. However, any investment made on or after the date will be subject to short-term capital gain, regardless of the holding period.

Do consult your tax advisor before making any investment decisions to learn the exact implications on your taxable income.

Target Maturity Fund’s Vs Fixed Deposits

Another common comparison of TMFs (besides the traditional debt funds) is often made with fixed deposits (FDs). Despite the rise of alternative investments and stock-market-linked alternatives, FDs remain very popular in India due to their reliability, low risk, and consistent return-providing capabilities.

Let us carry out the comparison: TMF vs FD, considering different aspects:

Feature | TMFs | FDs |

Nature of Returns | Market-linked but predictable if held till maturity; reflects bond yields | Fixed interest rate locked at booking |

Average 3–5 Year Returns (2025) | ~7.5%–8.1% p.a. (based on current target maturity fund returns) | ~6.5%–7.2% p.a., depending on the bank |

Risk | Low, as bonds are held till maturity | Very low as the principal is secured |

Liquidity | Can be redeemed anytime without penalties (subject to NAV movement) | Premature withdrawal allowed with a penalty |

Taxation | As per Slab | As per Slab |

Transparency | Portfolio composition and YTM are disclosed daily | No portfolio visibility; only rate and tenure |

Suited For | Investors seeking predictable, tax-efficient, and diversified returns, such as fixed income mutual funds investors | Investors preferring guaranteed returns |

Conclusion

As mentioned before, despite the regulatory factors, there is a significant amount of flexibility when it comes to personal financial management. TMFs are preferred by investors seeking stability, predictability, and efficient post-tax returns. By blending the safety of government-backed securities with the transparency of index-based investing, TMFs provide a compelling alternative to traditional fixed deposits.

You can include TMFs in your portfolio if you have medium to long-term targets such as retirement planning, children’s education, and capital preservation. The recent popularity of funds like the HDFC Target Maturity Fund, Kotak Target Maturity Fund, and Axis Target Maturity Fund reflects growing confidence in this category of fixed-income mutual funds.

Visit Grip Invest today!

FAQs On Target Maturity Funds In India

1. Are target maturity funds safe?

Yes, they are relatively safe since most TMFs invest in government securities, PSU bonds, and state development loans. However, they are not risk-free: returns can fluctuate if you exit before maturity.

2. How are TMFs taxed?

Gains from TMFs are taxed as short-term capital gains, added to your income, and taxed as per your slab. Earlier indexation benefits for long-term holdings were removed in 2023, but TMFs may still offer better post-tax outcomes than FDs for higher-income investors.

3. Which is better – TMF or FD?

TMFs typically offer higher potential returns and better liquidity, while FDs guarantee fixed interest and capital protection. For investors seeking predictable yet flexible returns, TMFs can be a more efficient alternative.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001