Types Of Pension Plans In India: Choose The Right Retirement Strategy

Most Indian professionals intuitively know they should save for their retirement, yet the way is often not clear. Choosing a pension plan is not a tick in the box. You need to match your age and career stage, along with your comfort with risk, to choose the types of pension plans that will work over decades.

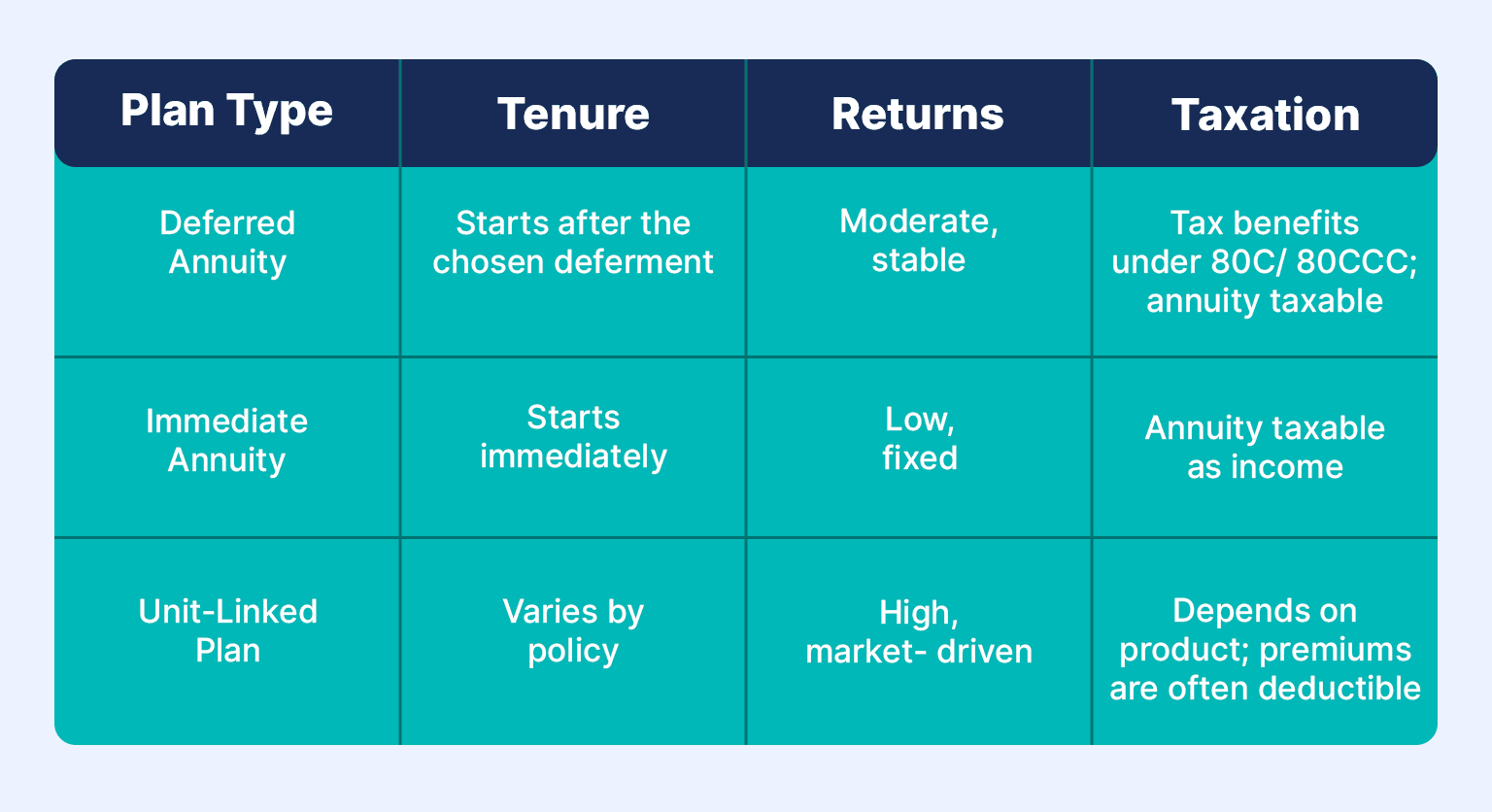

Deferred annuities give you time to build your retirement corpus, immediate annuities give you income now, NPS lets you invest in markets with controlled risk, and unit-linked plans let you leverage growth.

Compare tenure, returns, and tax benefits to make the right choice for the best pension plans in India.

Major Types Of Pension Plans In India

Your lifestyle after retirement will be funded by the retirement plan you choose today. In India, four broad choices exist to accommodate different needs, income levels, and risk profiles.

Beyond the basic differences of returns and taxation, each has features of its own that affect how well it fits into your financial plans.

1. Deferred Annuity Plans

Deferred annuity plans are best known for their reliability, but few people realise how flexible this life insurance plan can be. Most insurers allow both regular and single-premium payment options. The deferment period, often five to thirty years, lets you decide when the pension starts.

Some plans even offer guaranteed additions or bonuses during the accumulation phase, which quietly enhance your future payout. What is often overlooked is the surrender clause; early exit may trigger penalties and tax implications, so planning tenure carefully is the key here1.

2. Immediate Annuity Plans

Immediate annuity schemes are preferred by retirees who have a lump sum available. However, the payment options available are more diverse for this insurance product. You may choose from a lifetime income, a joint-life product that continues for a spouse, or even a "return of purchase price" feature that will pay back invested capital to your nominee.

All these options impact the annuity rate, which may also vary considerably from one insurance company to another. A proper comparison can make all the difference to long-term income2.

3. National Pension System (NPS)

NPS, though with equity exposure, is often perceived to be a government-backed scheme. Flexibility is inherent in this retirement product. You can actively change your asset allocation between equities, corporate bonds, and government securities, or let it auto-adjust with age.

Tier II accounts allow for withdrawals at any time (unlike Tier I accounts that lock in withdrawals before 60), offering liquidity not available with traditional pension products. Remember, Tier I accounts are mandatory before you can open a Tier II account3.

4. Unit-linked Pension Plans

Unit-linked pension plans India combine investment and insurance, but their value lies in their transparency. The policyholder can view the performance of the fund in real time and switch between equity, debt, and balanced funds without the incidence of tax during the accumulation phase.

Many of these plans also add loyalty benefits after a set number of years, hence rewarding long-term commitment4.

How To Choose The Right Pension Plan

The choice of a retirement plan depends on what the investor needs. A young investor may seek growth, while those who are closer in age to retirement may appreciate more stability and guaranteed income from their investment. Having a plan that's suited to your goals and risk appetite works better5.

Here’s how you can choose the pension plan according to your age and retirement goals:

| Age | Life Stage | Recommended Plan Type | Why It Fits |

| Ages 25–35 | Early career, moderate income | NPS or Unit-Linked Pension Plan | A long investment horizon allows higher equity exposure for better growth. |

| Ages 35–50 | Mid-career, higher income | Deferred Annuity or Hybrid Plan | Weigh growth with safety as retirement approaches. |

| Ages 50–60+ | Pre-retirement or retired | Immediate Annuity | Provides regular, guaranteed income shortly after investing. |

| Any Age | Conservative investor | Deferred Annuity - Traditional | Ensures predictable returns with stable income and very low risk. |

Complementary Fixed-Income Alternatives

If you have already planned for your core pension income, you can consider fixed-income tools that can top up your cash flow in retirement. One such tool is listed bonds offered via the Grip Invest platform. These bonds pay regular interest in the form of monthly or quarterly payments and are designed to give periodic income along with your pension.

Grip Invest enables access to rated and listed corporate bonds or securitised-debt instruments. Some pay interest monthly or quarterly, which allows you to align payouts with your monthly retirement budget.

Check the following before you add this option to your retirement plan:

- Credit rating of the bond or SDI

- Monthly or quarterly interest payment

- Maturity date

- How the income is taxed

Interest constitutes “other income” while principal repayment possibly has different implications. This type of fixed-income stream, when used correctly, can help reduce reliance on riskier investments and provide a layer of steady income that will help augment your pension plan.

Conclusion

When you align your age, income, and retirement vision with a plan's features, you can shift into retirement with more control. Deferred annuities might work if you are decades away from your retirement and stability is your number one concern. If you want income now, immediate annuities suit those closer to retirement.

NPS also has the potential to grow with a long investment horizon. Unit-linked plans are also a good choice if you understand the associated market risk. Along with fixed-income components, add bonds and SDI from Grip Invest to your portfolio, so that you can increase a life annuity pension or reduce overall risk in your portfolio.

FAQs on Types Of Pension Plans

1. What are the four major kinds of pension plans in India?

A deferred annuity offers income after a set period. An immediate annuity pays right after investment. The NPS mixes equity and debt for long-term growth. Unit-linked pension plans link returns to the performance of the market, with higher potential coming at higher risk.

2. Which pension plan gives the best return?

No single plan suits everyone. NPS and unit-linked options often offer higher returns through market exposure. Guaranteed annuity plans emphasise regular, low-risk income over growth. The best option would be determined by age, income, and risk comfort.

3. How is pension income taxed?

Employer pensions are taxed as "Salary." Family pensions fall under "Other Sources." Commuted pensions may receive partial exemptions, while annuity income from life insurance products is taxable under “Other Sources.”

References:

1. ICICI, accessed from: https://www.iciciprulife.com/retirement-pension-plans/annuity-planning.html

2. Policy Bazaar, accessed from: https://www.policybazaar.com/en-us/annuity/

3. SBI Life, accessed from: https://www.sbilife.co.in/en/life-insurance/retirement-pension-plans

4. India First Life, accessed from: https://www.indiafirstlife.com/knowledge-center/retirement-planning/what-is-unit-linked-pension

5. Edelweiss Life Insurence, accessed from: https://www.edelweisslife.in/blogs/insurance-glossary/what-are-the-different-types-of-pension-plans-in-india-and-which-one-should-you-buy

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001