Zomato Share Price Explained: What Quick Commerce Rules Mean For Investors

Zomato is one of the most popular food delivery services in India. The company initially started as a restaurant rating platform and diversified into restaurant discovery, table reservations, and Hyperpure, a B2B supply-side business.

In addition, Zomato quick commerce business with Blinkit, a grocery and essentials delivery service, is a pioneer in quick commerce in India, serving Tier I, II, and III cities effectively.

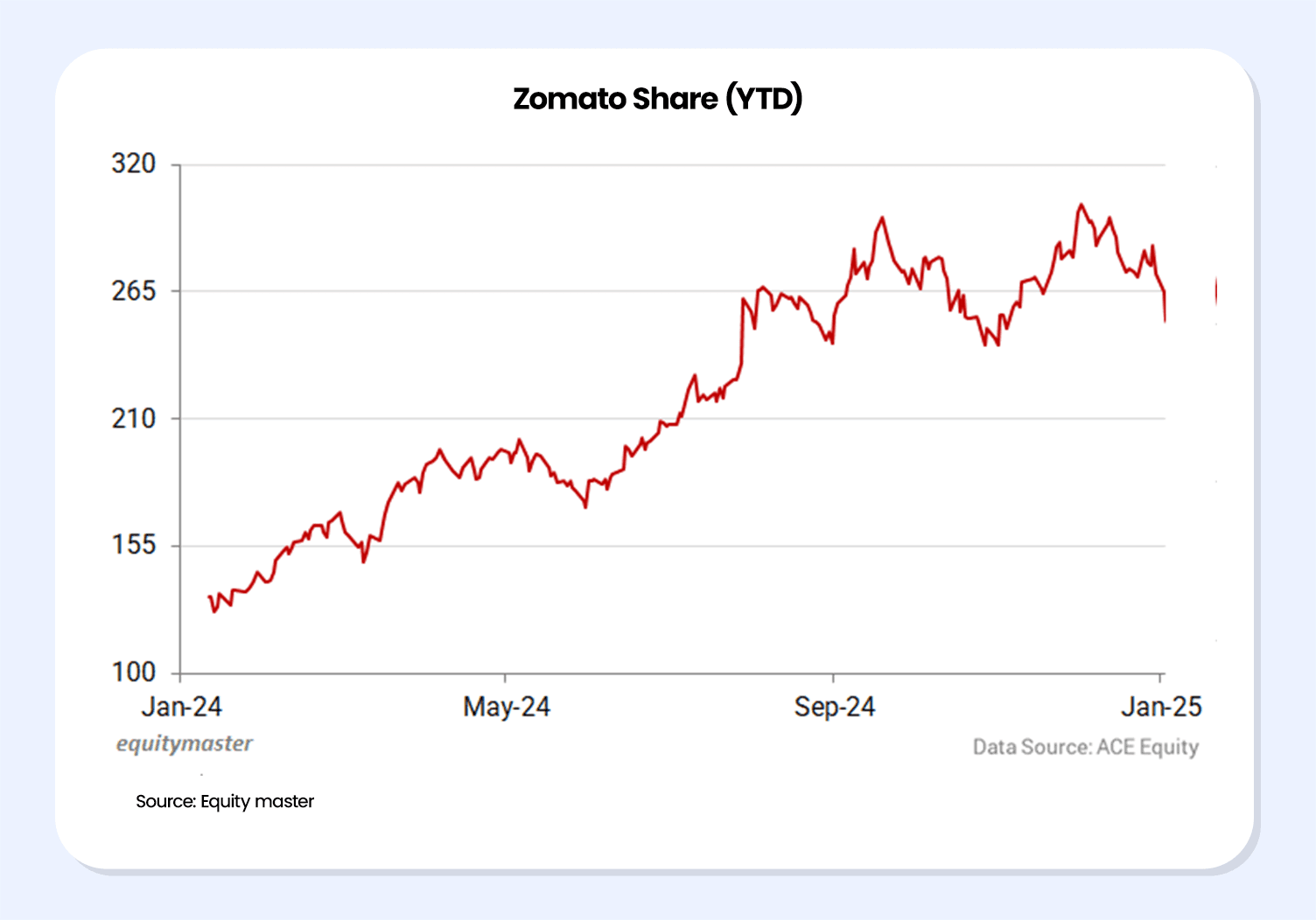

The Zomato stock (now NSE: ETERNAL) was listed on the exchanges in 2021 and the share has surged by close to 130% since its listing (having listed at INR 115 per share and currently trading at INR 288.00 per share).

However, the recent conversations around the need for implementing stricter rules in the context of Zomato quick commerce business, particularly related to the dropping of 10-minute delivery guarantee has resulted in a fresh debate around the Zomato share’s future growth and the group’s overall journey towards profitability1.

Zomato Share Price Performance Overview

As mentioned before, Zomato share price has surged upwards in the past few years but has been equally volatile. Following a first post-IPO run, share prices ranged widely, with major inflexion points driven by earnings surprises, fluctuations in profitability, and the macroeconomic mood.

A Zomato stock analysis shows that its share price declines have frequently been associated with either profit warnings or cost pressures from expansion programs. The company has seen strong revenue growth, and its expansion strategy has disrupted various sectors and positively influenced end customers. The investors have reacted well to the strategies, and hence the growth in investment has been rather satisfactory.

However, investor sentiment may be affected by regulatory developments, including changes to the timeline for quick-commerce delivery. News involving changes to the operating model, regulatory reviews, or labour issues can affect the share price. Interestingly, the stock has remained strong over the past month, with a 1.25% price increase and stronger trade volumes.

Corporate Leadership Shifts and Equity Market Reactions

A key corporate development that investors are closely tracking is the recent leadership change at Eternal Ltd, the parent company of Zomato and Blinkit. Founder Deepinder Goyal has stepped down as CEO and will transition to a vice chairman role, while Albinder Singh Dhindsa takes over as the new CEO. Such leadership transitions often influence short-term investor sentiment and stock price movements, especially for widely held consumer tech stocks. As discussed in our Zomato share price analysis, management changes, growth strategy clarity, and execution play a crucial role in shaping market expectations and long-term valuation for Zomato shares.

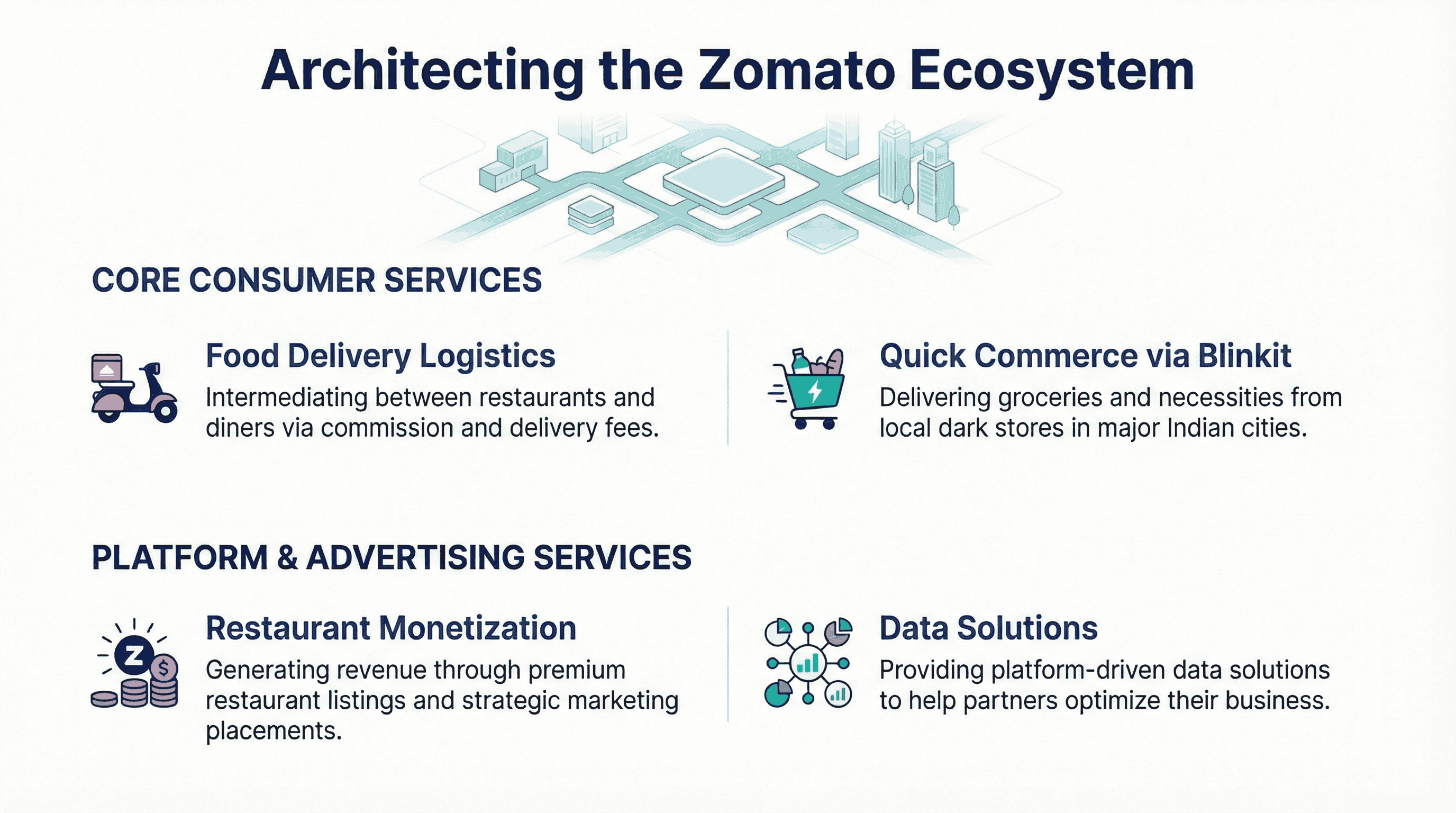

Zomato’s Business Model At A Glance

Zomato is essentially a multi-revenue stream entity within the Indian online food and groceries ecosystem. It has the following major segments:

- Food delivery: Intermediation between restaurants and diners at a commission, as well as a delivery fee.

- Quick Commerce through Blinkit: Groceries and necessities provided by local dark stores in metros and Tier-I cities;

- Advertising and platform services: Monetising restaurant listings, marketing placements and data solutions.

Quick-commerce division Blinkit needs a significant amount of initial capital to develop dark-store networks, logistics, and store warehousing, and to organise the workforce. Although this segment is regarded as a long-term growth driver, it can result in short-term cost pressure.

Why Quick Commerce Matters For Zomato Share Price

Blinkit has emerged as one of Zomato’s most important strategic pillars. While food delivery is already a mature and stable business that generates consistent cash flows, rapid commerce offers the potential to significantly expand overall order volumes, provided it scales efficiently and with disciplined capital deployment.

Prior to the recent regulatory nudges, Blinkit's impact on Zomato's about 10-minute deliveries has become one of the key marketing points of difference, driving customer engagement and high repeat business. This promise was anchored in a broader market notion that equates speed with growth, appealing to investors seeking large addressable markets.

Regulations that narrow these differentiating factors encourage companies to strengthen other competitive levers such as pricing, product assortment, and service reliability. Customers can still benefit from fast deliveries, but the emphasis shifts from an ultra-fast, guaranteed promise to a more balanced and sustainable value proposition.

How The 10 Minute Delivery Rule Could Impact Zomato

The more recent conversations around the 10-minute delivery guarantee is a minor yet significant change in Zomato's approach to quick-commerce. With such a Zomato business model India might include more emphasis on opening new dark stores, strengthening the safety measures undertaken for the delivery partners, and improving the packaging times.

The top management of the company has stated that no partner is ever penalised for late deliveries, and that deliveries are quicker only because the stores are located within a 1.5-2 km radius of a customer’s residence. The top management also underlined that Blinkit's packaging time is much shorter than that of conventional retail, giving them an edge as a leader in quick commerce in India.

1. Revenue Impact

Customers can continue to access fast deliveries within the quick-commerce segment, even without positioning the 10-minute promise as the core differentiator. This shift may naturally moderate incremental revenue growth, as competitive focus broadens to include factors such as product assortment, pricing efficiency, and overall service experience, rather than speed alone.

2. Cost and Margin Impact

Expenses associated with a large network of dark stores and last-mile delivery logistics will not disappear simply because of a shift in the marketing tagline. In an imaginary situation in which Blinkit can sustain its speed by investing in more dark stores but cannot advertise ultra-fast timelines, the cost base might further pressure margins unless operational efficiencies are improved.

3. Investor Sentiment

Regulations that focus on promotional statements, particularly those related to workers' safety and operational risks, can undermine investor confidence. It will be interesting to see how Zomato share price moves after dropping the 10-minute delivery promise. There might be some volatility, but the investors might also appreciate the steps undertaken by the company to enhance the safety of the delivery partners and the fact that this development can result in the expansion of operations with more dark stores and exploring more opportunities in Tier II and III cities.

Nevertheless, investors must note that recent clarifications from the company indicate that operational delivery times are not significantly affected. Also, the elimination of 10-minute branding does not constitute a fundamental change in Blinkit's operations.

Should Investors Track These Developments Closely?

Regulatory clarity is important to valuations of listed companies such as Zomato. Unrevealed liabilities relating to labour policies, marketing statements, or operating schedules can lead to risk premiums, which are reflected in stock prices by investors. Therefore, to make informed investments, it is necessary to stay up to date on changes and cases involving gig workers, as well as on policymaking trends and enforcement.

To an investor, risk is not just embedded in today's earnings reports, but also in future regulations that might redefine cost structures and competitive relationships.

Pros And Cons Of Purchasing Eternal Stocks

Pros

- Eternal has diversified its business model from a restaurant discovery website to food delivery, quick e-commerce, B2B supply chain and event bookings and ticketing. This reduces the dependence of Eternal on a single sector and strengthens its long term growth potential as a wider consumer-commerce ecosystem.

- Eternal has displayed a significant increase in revenue (169.6% jump from FY25 to FY26) due to larger order volumes and increasing customer adoption. Even though profit margins remain under pressure due to higher spending on newer ventures, investors view this as a strategic long term move to strengthen the company’s market position.

- Eternal’s position as a high-growth new-age technology company gives it exposure to rapidly expanding digital consumer trends. Unlike traditional businesses with slower expansion opportunities, Eternal operates in scalable markets where successful execution can drive rapid revenue growth and long-term market dominance.

Cons

- Since Eternal is currently building new businesses while aggressively expanding existing ones, they do not distribute dividends and are focussed on reinvestment. Zero dividend yields would turn away investors who want predictable income.

- Potential regulatory changes in e-commerce (particularly quick commerce) might increase compliance and operating costs, increasing pressure on Eternal’s profit margins.

- Extremely high competition in all areas from Swiggy, Zepto, Bookmyshow and BigBasket could lead to aggressive discounting and rising customer acquisition costs.

Zomato Peer Comparison: Market Cap, Returns And Valuation Metrics

| Name | EPS 12M | P/E | NP QTR RS CR | 1YR RETURN % | MAR CAP RS CR |

| Eternal | 0.38 | 668.82 | 174.00 | 11.29 | 244781.15 |

| Meesho | -2.97 | -166.35 | 10.5* | 85286.37 | |

| FSN E-Commerce | 0.7 | 359.49 | 78.75 | 32.43 | 75267.34 |

| Swiggy | -15.05 | -800.00 | -20.69 | 74072.98 | |

| Urban Company | -1.52 | -161.16 | -26.13** | 18953.43 | |

| Brainbees Solut. | -2.69 | -48.21 | -32.74 | 11960.16 | |

| Cartrade Tech | 46.58 | 36.92 | 70.85 | 12.28 | 8408.75 |

Source: Screener

*Calculated from 10th December 2025 when Meesho stocks were first publicly listed

**Calculated from 18th September 2025 when Urban Company stocks were first listed

Eternal is trading at an extremely high P/E ratio despite a low EPS, which suggests that investors are pricing in very high future growth expectations. Its 1-year return is positive, but still lower than FSN E-Commerce and Cartrade Tech.

FAQs On Zomato Share Price

1. Does dropping the 10-minute delivery promise hurt Zomato’s revenue outlook?

Not materially. Demand for quick commerce is driven more by convenience, assortment, and reliability than a fixed time claim. Operational delivery speeds largely remain unchanged.

2. How important is Blinkit to Zomato’s long-term valuation?

Blinkit is a key growth engine for Zomato, especially as food delivery matures. Its ability to scale profitably will heavily influence future earnings and market multiples.

3. Will new quick-commerce regulations impact Zomato’s margins?

Regulations mainly affect marketing claims and labour safeguards, not core operations. However, compliance costs and expansion of dark-store infrastructure could keep margins under pressure in the short term.

4. Is the regulatory push a long-term risk for Zomato investors?

It is more of a monitoring risk than a structural threat. Clearer rules can actually reduce uncertainty, improve worker safety, and support sustainable growth if managed well by the company.

References:

1. National herald India, accessed from: https://shorturl.at/6ZYZh

2. Economic Times, accessed from: https://economictimes.indiatimes.com/magazines/panache/no-timers-for-delivery-workers-zomatos-deepinder-goyal-explains-blinkits-10-minute-delivery-promise/articleshow/126299286.cms?from=mdr

3. Equity master, accessed from: https://www.eqimg.com/images/2025/01152025-chart9-equitymaster.gif

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.