IDCW In Mutual Fund: Meaning, Taxation & Growth Vs IDCW Explained

Investors typically choose between two payout options when investing in mutual funds: Growth and Income Distribution cum Capital Withdrawal (IDCW). Many assume IDCW provides additional returns, but that is a common misconception. Understanding IDCW in mutual fund investments is essential before selecting an option, as it affects cash flow, NAV, taxation, and the overall investment experience.

IDCW meaning is Income Distribution cum Capital Withdrawal. Formerly known as the dividend option mutual fund, the term was introduced by SEBI to clarify that these payouts are not additional income and may include a distribution of the scheme's capital, subject to distributable surplus. Understanding IDCW mutual fund payouts helps investors make informed decisions based on their financial goals rather than misconceptions.

movements. While you receive the payout, the overall value of your investment adjusts accordingly.

The revised terminology makes it clear that Income Distribution cum Capital Withdrawal may be paid from the scheme's realised gains, accumulated distributable surplus, or, where permitted under regulations, a return of capital.

Where Does IDCW Money Come From?

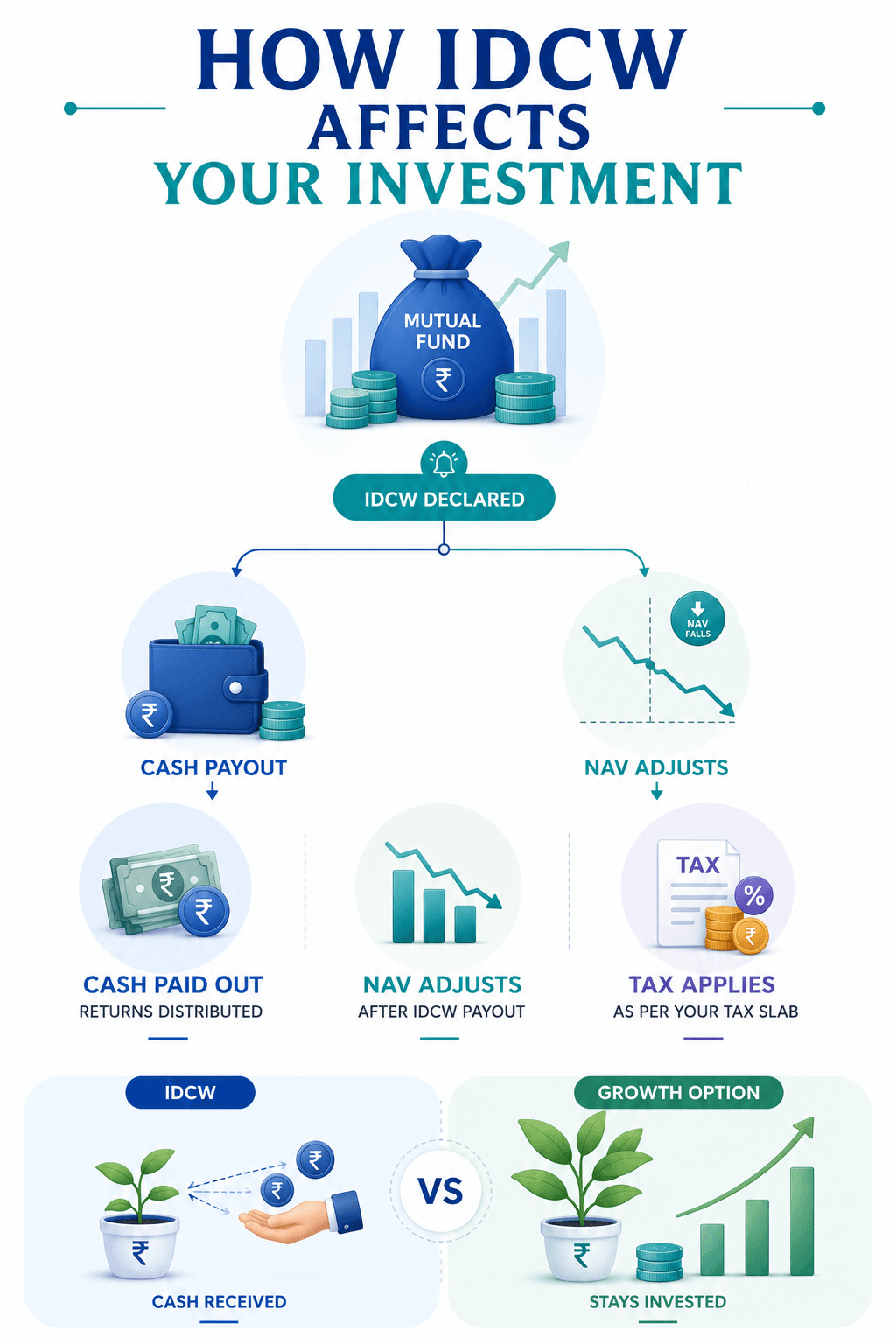

A common misconception about an IDCW mutual fund is that its payouts represent additional returns generated by the scheme. In reality, IDCW payouts are made from the scheme's distributable surplus, which may comprise realised gains, dividend income, interest income, or, where permitted under applicable regulations, a return of capital.

This is why IDCW should not be viewed as an additional wealth-creation mechanism. Whenever an IDCW is declared, the scheme's NAV typically falls by a corresponding amount, subject to market movements.

For example, suppose an investor holds units worth INR 5 lakh in an IDCW mutual fund. If the scheme declares an IDCW payout of INR 25,000, the investment value may reduce to approximately INR 4.75 lakh immediately after the payout, assuming there are no market-related changes in the NAV.

How IDCW Affects Your Investment?

Choosing the IDCW option affects how you receive returns rather than how the mutual fund is managed.

Whenever an IDCW is paid, the scheme's NAV typically falls by a corresponding amount, subject to market movements. As a result, a portion of your investment is distributed instead of remaining invested, which may reduce the power of compounding over the long term. This is one reason investors with long-term wealth-creation goals often prefer the Growth option.

Taxation is another important factor to consider. Under the current income tax provisions, IDCWs received from mutual funds are taxable in the hands of the investor at the applicable income tax slab. Additionally, mutual funds may deduct TDS on IDCW payments if the amount exceeds the threshold prescribed under the Income-tax Act.

Growth vs IDCW: The Comparison

Feature | Growth Option | IDCW Option |

Payout | No periodic payout method is available. | Periodic payouts can be declared. |

NAV Impact | It continues to grow with gains | Reduces after every IDCW declaration. |

Compounding | Higher growth rates due to potential reinvestments. | Lower compounding potential as periodic payouts reduce the amount remaining invested. |

Taxation | Taxation arises on redemption: subject to capital gains rules under the Indian tax system. | It is taxable as per an individual’s income tax slab |

Suitable For | Long-term wealth creators | Investors seeking periodic cash flow |

Who Should Consider IDCW?

The suitability of IDCW in mutual fund investments depends on an investor's financial goals rather than market performance.

Retirees or investors looking for periodic cash flows may consider the IDCW option, as the fund house may declare payouts whenever distributable surplus is available. Similarly, investors seeking supplementary cash flows alongside other sources of income may also find IDCW suitable.

On the other hand, investors focused on long-term capital appreciation generally prefer the Growth option, as gains remain invested and continue to compound over time.

It is important to remember that IDCW payouts are neither fixed nor guaranteed, unlike the interest earned on a fixed deposit with a bank. The fund house decides whether to declare an IDCW and the payout amount based on the scheme's distributable surplus and applicable regulations.

Common Myths About IDCW That Mislead Investors

Myth | Reality |

IDCW offers extra returns | IDCW reduces the NAV amount by frequent payout withdrawals. |

IDCW is guaranteed | The payouts are based on fund performance and distributable surplus. |

IDCW equals bank FD interest. | IDCW is not assured as it is market-related.

|

A higher IDCW indicates better fund performance. | A higher IDCW does not necessarily indicate better fund performance, as payouts may reduce the scheme's NAV and can include a return of capital where permitted. |

IDCW As Part Of A Diversified Income Strategy

Although IDCW can provide periodic cash flows, it may not be the most reliable source of income because payouts are discretionary and depend on the scheme's distributable surplus.

A more balanced approach is to combine equity or hybrid mutual funds with other investments that offer relatively predictable income. For instance, investors may diversify across IDCW-based mutual funds, high-quality corporate bonds, fixed deposits, and other fixed-income investment options available through GripInvest, depending on their financial goals and risk appetite.

Ultimately, the choice between the Growth and IDCW options should be based on your income needs, tax implications, investment horizon, and risk tolerance rather than the expectation of receiving additional returns.

FAQs On IDCW In Mutual Fund

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001