Active vs Passive Mutual Funds India 2025: Returns, Fees And Risks

The Mutual Fund industry in India recorded a new high in August 2025 as the assets under management (AUM) reached an all-time high of 75.19 Lakh Crore, post a 12.7% rise1. Moreover, in September 2025, the passive fund market efficiency grew as its AUM grew 13% and reached 17% of the total mutual fund AUM2.

While the actively managed mutual fund continued to dominate the market with INR 3.62 lakh crore inflows, passive funds contributed INR 36,000 crore3.

With the growing tussle between active vs passive mutual funds, a pertinent question arises for investors. How are these funds different from one another, and which is suitable for an investor?

Understanding the difference between actively managed vs passively managed funds, through this detailed guide, can aid in addressing this dichotomy.

What Are Active And Passive Funds?

The first step in understanding active vs passive mutual funds is to explore individual meanings. Both active and passive, in the case of mutual funds, depict the method of managing the fund. Therefore, their key meaning and difference stem from the fund manager of active vs passive funds. Let us decode each category in detail.

What Are Active Mutual Funds?

If the fund managers of a mutual fund actively formulate the investment strategy of the fund to outperform the market benchmark through the selection, purchase and sale of securities, it is an active mutual fund.

These funds aim to generate greater returns than their benchmark. Let us take an example to understand the active fund return potential.

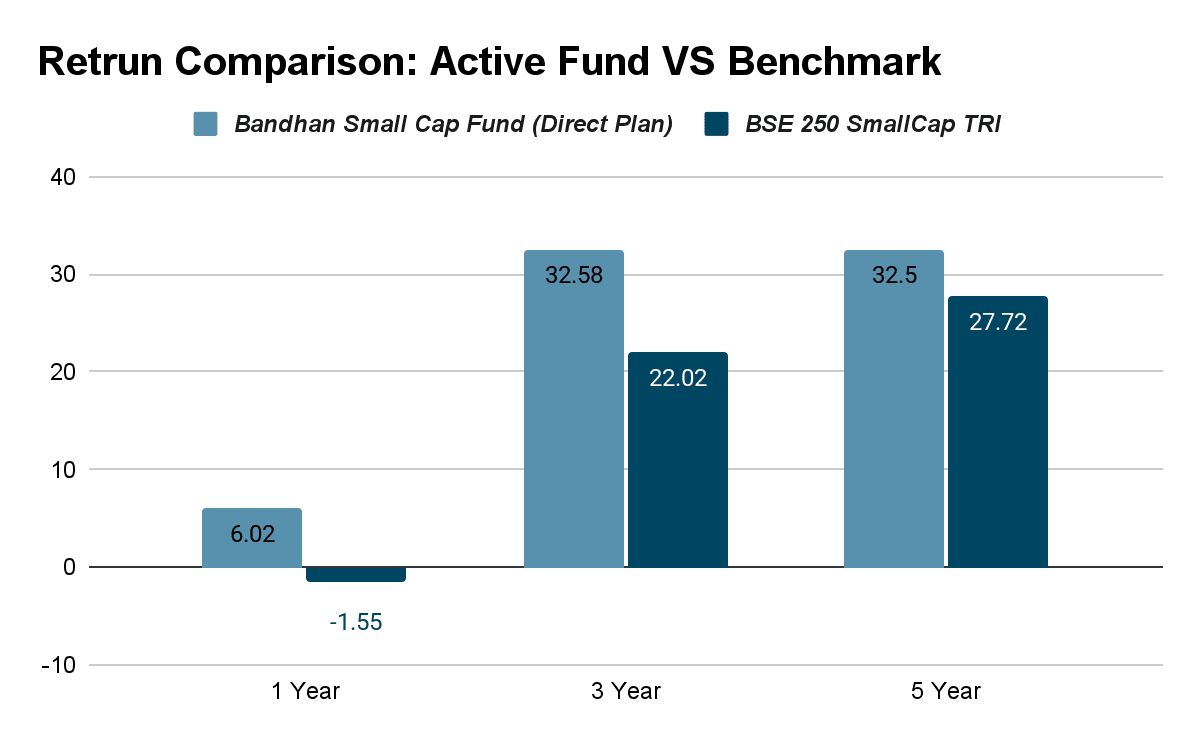

For example, Bandhan Small Cap Fund (Direct Plan) is an actively managed fund. The illustration below compares its performance with its benchmark BSE 250 SmallCap TRI as of 24 October 2025.

Source: The Value Research Online4

Now, let us move on to the next leg of our comparison, that is, the passively managed funds.

What Are Passive Mutual Funds?

If a mutual fund aims to track the performance of the benchmark and replicate it by investing in the same securities in an equivalent proportion, it is a passive mutual fund. The investing strategy is passive fund index replication, meaning that these funds aim to provide the same returns as the benchmark by emulating its portfolio and investment. Given that the most common type of passive mutual fund is an index fund, an example can crystallise the understanding of such investments.

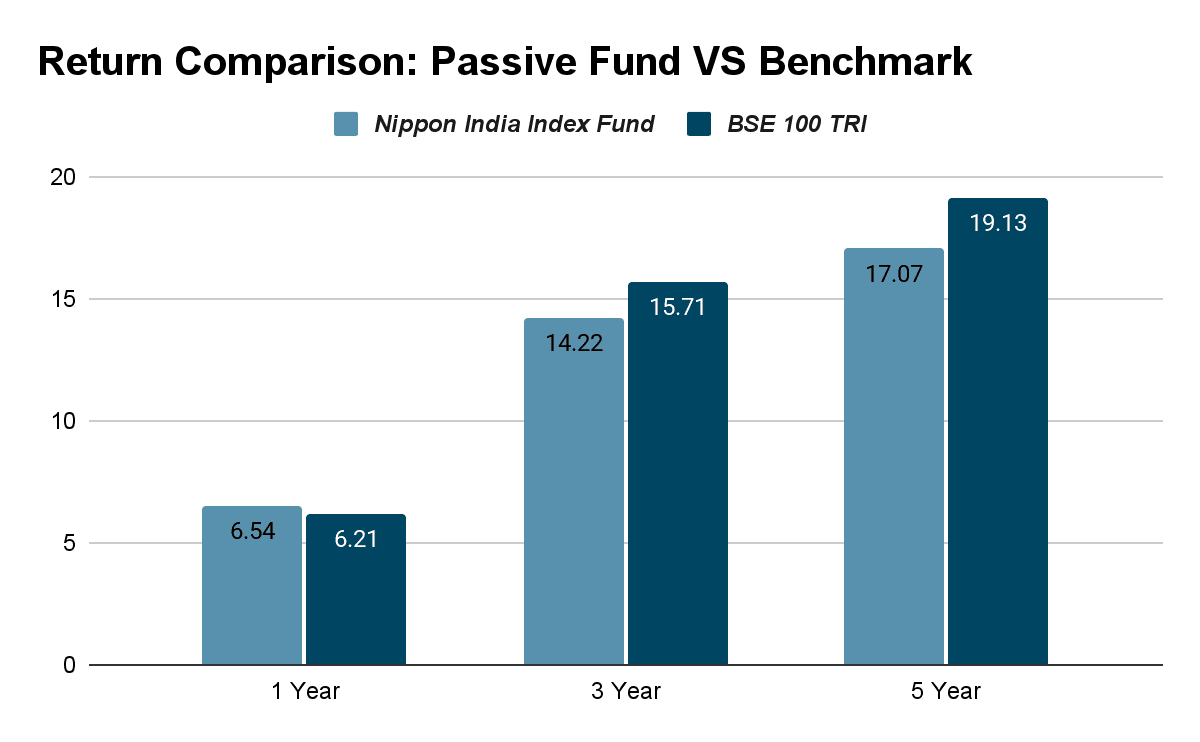

The illustration here shows the performance of the Nippon India Index Fund in comparison to its benchmark, BSE 100 TRI, as of 24 October 20255.

Therefore, the market-beating potential vs index tracking strategy is the fundamental difference between active and passive funds. While active funds aim to beat the market, passive funds aim to replicate it. Next, we must analyse the active fund vs index fund (passive fund) performance.

Active VS Passive Mutual Funds: Performance And Returns

To explore the difference between the performance of active and passive funds, this section picks the most commonly known fund categories that follow either of these styles and analyses their performance.

Active vs Passive Mutual Funds: Which Gives Better Returns?

The category average returns of top active mutual fund categories, like large-cap, small-cap, and debt corporate bond funds, as of 24 October 2025, are discussed here.

| Category | One-Year (%) | Three-Year (%) | Five-Year (%) |

| Large-Cap Equity | 4.44 | 15.90 | 18.60 |

| Small-Cap Equity | -0.87 | 20.90 | 27.67 |

| Corporate Bond Debt | 8.08 | 7.71 | 5.91 |

Source: The Value Research Onlline6

Unlike active funds that tend to outperform the market, resulting in a range of different returns recorded by diverse funds, a passive mutual fund aims to mirror the market. Therefore, rather than the category average, the analysis of the benchmark returns can aid in gauging the anticipated or expected return from the passive fund that follows it.

Now, index funds, which are the most common type of passive funds, have two common variants. They are regular index funds, which are related to equity and index fixed income funds.

The table below shows the most common indices and their returns (as of 24 October 2025), followed by market index funds.

| Benchmark | One-Year (%) | Three-Year (%) | Five-Year (%) |

| Nifty 50 | 7.06 | 14.62 | 18.07 |

| Nifty Small Cap 100 | 0.70 | 24.13 | 25.98 |

| Nifty IT | -12.55 | 10.27 | 13.00 |

| Nifty Bank | 12.86 | 12.73 | 19.59 |

Source: NiftyIndices7

Now, in the case of fixed income benchmarks for fixed income index funds, most benchmarks related to assets like bonds are extremely diverse, meeting unique investor objectives.mThe NIFTY AAA Corporate Bond Indices that have provided 7.59% to 8.18% returns since inception as of 30 September 20258.

Similarly, the NIFTY AA Category Corporate Bond Indices have delivered 7.60% to 8.70% returns since inception as of 30 September 2025.

The next step of performance comparison is the risk analysis.

Active vs Passive Mutual Funds: Understanding The Risk Factor

The table below discusses the key three-year risk metrics of different categories as of 30 September 2025.

| Category | Standard Deviation | Sharpe Ratio | Sortino Ratio |

| Large-Cap | 12.6822 | 0.6764 | 1.1171 |

| Small-Cap | 16.8210 | 0.7841 | 1.2660 |

| Index Fund | 1.3415 | 0.6509 | 1.0389 |

| Index Fixed Income | 0.6290 | 0.7601 | 1.4323 |

Source: Morningstar10

Now, let us discuss the fees and tax implications of these funds.

Active vs Passive Mutual Funds: Comparing Fees and Taxes

Both the fees payable to the fund house for investment management and the tax liability on mutual fund returns diminish the absolute yield in the hands of the investors. Therefore, taxation and expense ratio comparison is key to understanding the actual anticipated return.

- Expense Ratio: The active fund management fees are higher than those of passive funds because active fund managers proactively try to outperform the market, requiring more dynamic and hands-on portfolio management. Therefore, the active fund expense ratio is higher than that of passive funds.

- Taxation: The passive portfolio construction technique is different from the active fund strategy11. However, the mutual fund tax rates in India are determined based on mutual fund category, rather than management style. Therefore, investors must evaluate and compare based on category to gauge the active or passive fund tax efficiency.

Other than fund analysis, investors must also consider their unique investor needs and temperaments to choose between active vs passive mutual funds.

Active vs Passive Mutual Funds: Which To Choose?

Discussed below are some key metrics that investors must consider before choosing the right mutual fund.

1. Risk Tolerance: Conservative investors with low risk tolerance can opt for passive funds. Moreover, the passive fund tracking error can show how close the fund return is to the benchmark. While investors with an optimal risk appetite and growth objective might favour active funds.

2. Low-cost: Passive funds are among the low-cost investing strategies, with a lower expense ratio than active funds.

3. Blended Approach: Building a long-term portfolio with passive and active fund diversification might be an option. Conservative investors can opt for passive funds as a core investment and active funds for controlled growth. The allocation into these categories can be changed as per requirement.

Conclusion

Categories like active and passive funds offer investors with different temperaments and strategies a way to participate in the market. Active funds rely on professional fund managers who aim to outperform benchmarks through research and timely decisions, while passive funds simply track an index, offering lower costs and consistent returns. Within these categories, investors can further explore segments like active vs passive funds, equity funds, or hybrid funds, depending on their risk appetite and goals.

For those seeking steady, non-market-linked options, platforms like Grip Invest provide access to curated fixed-income investments that complement mutual fund portfolios and enhance overall diversification.

FAQs On Active Vs Passive Mutual Funds India 2025

1. Are passive funds safer than active?

Passive funds aim to mirror the market, while active funds aim to outperform it. While the popular opinion believes that passive funds are therefore safer than active funds, it is important to note that risk is involved in both.

2. Can active funds guarantee higher returns?

Although active funds aim to outperform the market, it is not guaranteed. Therefore, investors must compare fund returns with category averages and benchmarks to explore profitability.

3. Minimum SIP to start active vs passive?

Mutual fund investment, active or passive, can begin from as little as INR 100. Explore Grip and individual fund fact sheets to know more.

References:

1. The Times of India, accessed from: https://timesofindia.indiatimes.com/business/india-business/mutual-funds-scale-rs-75-lakh-crore-aum-share-of-passive-funds-has-more-than-doubled-heres-all-you-need-to-know/articleshow/124090177.cms

2. The Economic Times, accessed from: https://economictimes.indiatimes.com/mf/mf-news/equity-net-sales-positive-for-over-4-years-despite-market-correction-franklin-templeton-india-mutual-fund/articleshow/124784969.cms

3. DD News, accessed from: https://ddnews.gov.in/en/indias-mutual-fund-industry-grows-sevenfold-in-decade-passive-funds-gains-ground-report/

4. The Value Research Online, accessed from: https://www.valueresearchonline.com/funds/40564/bandhan-small-cap-fund-direct-plan/#performance

5. The Value Research Online, accessed from: https://www.valueresearchonline.com/funds/11536/nippon-india-index-fund-nifty-50-plan/#performance

6. The Value Research Online, accessed from: https://www.valueresearchonline.com/funds/fund-category/

7. Nifty Indices, accessed from: https://www.niftyindices.com/market-data/return-profile

8. Nifty Indices, accessed from: https://www.niftyindices.com/Factsheet/Factsheet_NIFTY_AAA_Corporate_Bond_Indices.pdf

9. Nifty Indices, accessed from: https://www.niftyindices.com/Factsheet/Factsheet_NIFTY_AAA_Corporate_Bond_Indices.pdf

10. MorningStar, accessed from: https://www.morningstar.in/tools/mutual-fund-category-risk-measures.aspx

11. AMFI India, accessed from: https://www.amfiindia.com/investor/knowledge-center-info?zoneName=TaxRegimeForMutualFunds

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001