Mutual Fund Vs Property: Which Investment Is Better In India?

Long-term investing starts with a goal. The right choice depends on how much capital you have, when you may need the money and how much risk you can accept.

The mutual fund vs property investment decision is therefore not only about past returns. A comparison of mutual funds vs real estate must also include liquidity, income, borrowing costs and diversification. Investors considering investing in mutual funds or property should begin with these practical factors.

Mutual Fund Vs Property Investment: Which One Matches Your Goal?

The mutual fund vs property investment decision becomes clearer when investors compare how each option affects their money in practice.

Factor | Mutual funds | Property |

Capital requirement | Can start with a small SIP or lump sum | Requires a sizeable upfront amount |

Liquidity | Units can generally be redeemed easily | Sale depends on finding a suitable buyer |

Returns | Driven by the underlying market and fund category | Earned through price appreciation and rent |

Risk | Market, credit and fund-specific risks | Location, legal, vacancy and borrowing risks |

Diversification | Money can be spread across several securities | Capital may remain concentrated in one asset |

1. Capital Requirement

Mutual funds allow investors to begin without accumulating a large investment corpus. According to AMFI, SIP instalments can start from around INR 500 per month, although the minimum varies across schemes.1

Property requires considerably more upfront capital. Consider a residential property priced at INR 50 lakh. Assuming the lender finances 80% of its value, the investor must arrange an INR 10 lakh down payment.

The initial expense does not end there. Stamp duty, registration charges, brokerage, furnishing and loan-processing costs can push the total cash requirement higher.

The difference becomes relevant for goal planning. An investor saving INR 20,000 per month can immediately begin a mutual fund SIP. The same investor may need several years to accumulate enough money for a property down payment.

2. Liquidity

Mutual funds generally allow investors to access their money more easily. Redemption or repurchase proceeds must usually be transferred within three working days. Schemes investing at least 80% in permitted overseas assets have a five-working-day timeline.2

The investor can also redeem only the required number of units. For example, someone with an INR 15 lakh mutual fund portfolio can withdraw INR 2 lakh while leaving the remaining amount invested.

A property cannot normally be divided and sold in this manner. The owner must find a buyer, negotiate the price, complete title verification and execute the registration process.

An urgent sale can also affect the price received. The owner may have to accept a lower offer when the need for money cannot wait for favourable market conditions.

Liquidity therefore matters even when the investment horizon is long. Unexpected medical costs, education expenses or changes in employment may require access to part of the invested capital.

3. Returns

Mutual fund returns depend on the scheme’s underlying assets. Equity funds invest mainly in shares, debt funds invest in fixed-income securities such as government and corporate bonds, while hybrid funds combine multiple asset classes.

There is no single average return for mutual funds because performance varies across categories and periods. The table shows annualised category returns across four common investment types.

Asset class | Mutual fund category | 3-year return | 5-year return | 10-year return |

Equity | Large Cap | 10.81% | 10.50% | 11.79% |

Debt | Corporate Bond | 7.02% | 6.00% | 6.81% |

Hybrid | Aggressive Hybrid | 11.31% | 10.44% | 11.31% |

Commodity | Gold | 31.99% | 22.55% | 14.90% |

Source: Value Research. Returns are category averages as of 16 July 2026 and are annualised.

Property returns usually have two components:

- An increase in the property’s market value

- Rental income earned during the holding period

Neither component remains uniform across locations.3 NHB RESIDEX reported that its 50-city housing price index increased 5.0% year-on-year during October–December 2025, compared with 7.2% in the corresponding quarter one year earlier.

However, the national figure hides substantial regional variation. Gurugram recorded a 22.8% annual increase, while Raipur saw prices decline by 8.9%. Bengaluru rose by 12.7%, Chennai by 8.2%, Mumbai by 3.7% and Pune by 3.5%.4

This shows why a national property average may not reflect an individual investor’s return. The outcome depends on the city, neighbourhood, building, purchase price, rental yield and ownership costs.

Therefore, mutual fund performance varies by category, while property performance depends heavily on location.

4. Risk

Mutual funds carry different levels of risk depending on what they hold. An equity fund faces stock-market volatility, while a debt fund may face interest-rate and credit risks.

SEBI requires asset management companies to display a Riskometer for their schemes. The scale ranges from low to very high risk, helping investors compare the scheme with their own risk tolerance.

Property prices do not appear to change every day, but that does not make the investment risk-free. Its value depends on local employment, infrastructure, supply, legal documentation and demand within a limited area.

For example, an investor may purchase an INR 60 lakh flat near a proposed business district. If the project is delayed and several new apartments enter the market, rental demand may weaken. The investor may then receive lower rent or need to reduce the selling price to find a buyer.

Moreover, borrowing introduces another risk. Home-loan instalments continue even when the property remains vacant, rent falls short of expectations or the borrower’s income declines.

5. Diversification

Mutual funds can spread money across different instruments. However, the level of diversification depends on the scheme category and portfolio.

A sectoral fund may concentrate most of its portfolio in one industry, while a credit-risk fund may carry greater exposure to lower-rated debt. Investors should therefore review the scheme portfolio before investing.

Property investment is usually more concentrated. An investor placing INR 50 lakh in one flat depends on one building, neighbourhood and local market.

The same amount can be divided across equity, debt, hybrid and gold funds. This reduces concentration, although it does not eliminate investment risk.

Property investment vs mutual fund highlights the strengths and limitations of both options. The following sections explain what may draw investors towards property or mutual funds or both.

What Kind Of Investor Chooses Property?

Homeownership has long been viewed as a sign of financial stability. Many investors also value the sense of permanence that comes with owning a physical asset.

However, a self-occupied home and an investment property serve different purposes. A home used for living provides personal utility, while an investment property must be assessed through different factors.

1. Rental income: A rented property can provide regular cash flow. However, investors should calculate the net yield after maintenance, vacancy, property tax, repairs and society charges.

2. Tangible ownership: Some investors prefer an asset they can see, use or modify. A residential property may also serve a personal purpose later, such as becoming a family home.

Physical ownership does not remove investment risk. Building quality, neighbourhood development, title documentation and local demand can directly affect resale value.

3. Leverage: A home loan allows an investor to control a property worth more than the initial down payment. This can increase gains when prices rise.

The reverse also applies. The borrower must continue paying the equated monthly instalment (EMI) even if the property remains vacant or its market value declines. Interest also raises the property’s total acquisition cost.

4. Long holding periods: Property usually works better when the investor can wait through weak demand and slow sale periods. Frequent buying and selling may reduce returns because every transaction involves costs.

Property may therefore suit investors seeking rent, physical ownership and the controlled use of borrowing. Investors prioritising flexibility may find mutual funds more suitable.

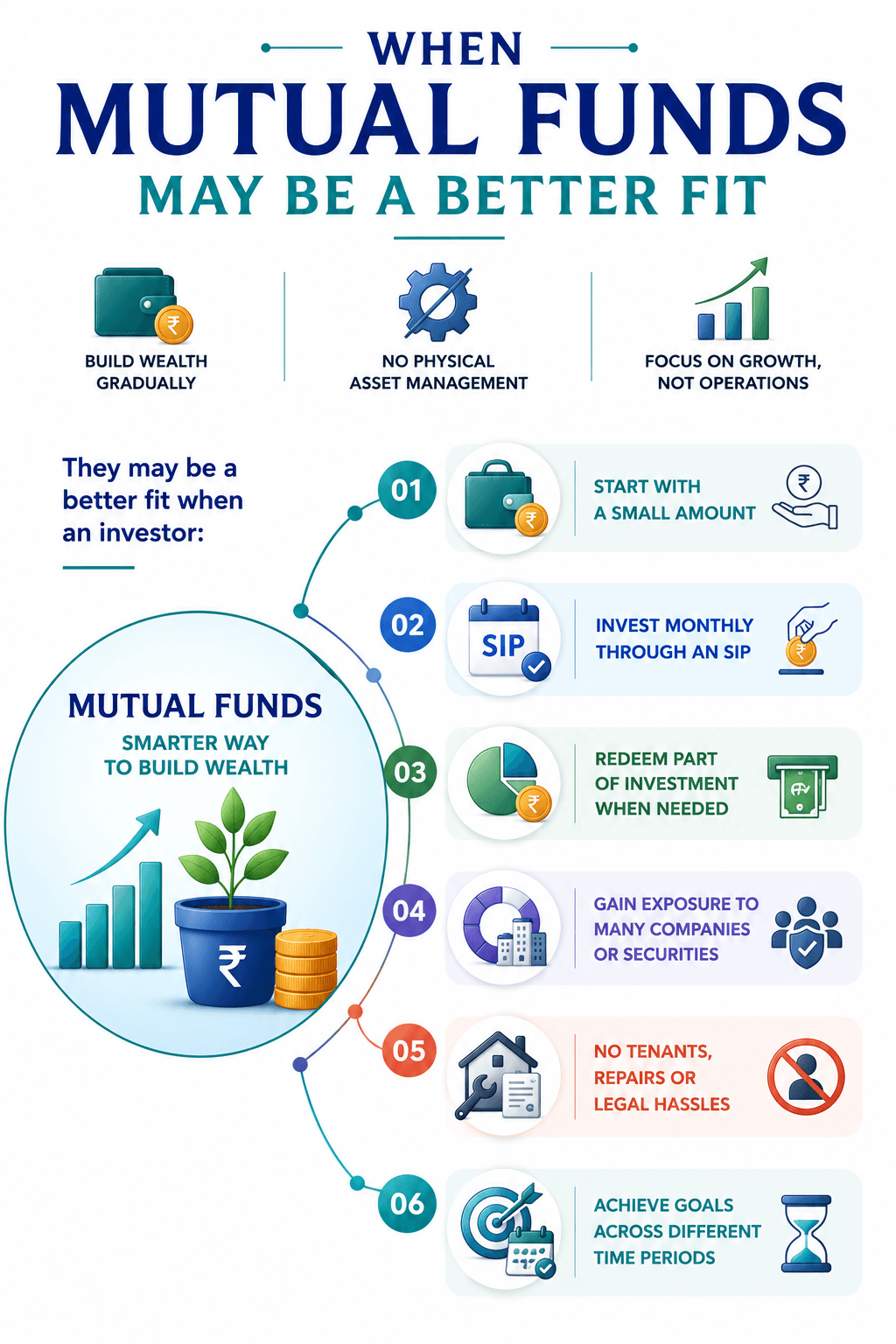

When Mutual Funds May Be A Better Fit

Mutual funds may suit investors who want to build wealth gradually without managing a physical asset.

They may be a better fit when an investor:

- Wants to begin with a smaller amount

- Plans to invest monthly through an SIP

- Needs the option to redeem part of the investment

- Wants exposure to several companies or securities

- Does not want to handle tenants, repairs and legal documentation

- Has financial goals spread across different time periods

Mutual funds also make portfolio adjustments easier. An investor can allocate money among equity, debt and hybrid schemes instead of depending on one property market.

However, convenience does not mean stable returns. Investors still need sufficient time and the ability to tolerate market declines.

The choice between mutual funds vs real estate does not always require selecting only one. Investors with adequate capital can use both for different purposes.

Can You Invest In Both?

Combining the two assets can reduce dependence on one return source, provided the property does not consume the entire portfolio.

The following examples are illustrations. They show how investors might divide long-term growth capital after maintaining emergency savings and adequate insurance.

Investor type | Mutual funds | Property exposure | Possible approach |

Young professionals | 70% | 30% | Build equity investments first while creating a separate property down-payment corpus. |

Families | 55% | 45% | Maintain mutual funds for education and retirement while building equity in a residential property. |

High-net-worth individuals | 50% | 50% | Combine diversified funds with selected residential or commercial properties that generate income. |

These percentages are not fixed recommendations. Income stability, existing property ownership, loans, financial goals and expected expenses should determine the final allocation.

A young professional with an uncertain work location may prioritise mutual funds. A family planning to remain in one city may give property a larger share. A high-net-worth investor may hold several assets without depending heavily on one building.

Consider an investor with INR 25 lakh and a 10-year horizon. To make the comparison clearer, assume no home loan.

For the mutual fund option, assume an annualised return of 10%.

After 10 years:

INR 25 lakh x 10% annual growth = ~INR 64.84 lakh

Now assume the investor purchases a property for INR 25 lakh. The property appreciates by 5% annually.

After 10 years:

Estimated property value = approximately INR 40.72 lakh

Assume the property also generates gross rent equal to 4% of its original value. That produces INR 1 lakh annually, or INR 10 lakh over 10 years, assuming rent remains unchanged.

Property value plus gross rent = ~INR 50.72 lakh

Under these assumptions, the mutual fund amount is about INR 14.12 lakh higher. However, the property figure excludes vacancy, maintenance, taxes and transaction costs. The mutual fund figure also excludes taxes and scheme expenses.

The result could change if property prices rise faster, rents increase or the investor uses affordable leverage. Mutual fund returns may also fall below the assumed 10%. The example shows why assumptions matter more than broad claims about which asset always performs better.

Diversification Beyond Traditional Assets

Mutual funds and property do not need to form the entire investment portfolio. Fixed-income investments can add another source of returns.

Corporate bonds allow investors to lend money to a company for a defined period. In return, the issuer generally pays interest at a stated coupon rate and repays the principal at maturity.

Bonds may complement equity mutual funds by adding scheduled interest payments. They can also reduce the need to depend entirely on property rent for income.

Grip Invest offers curated fixed-income products, including corporate bonds, SDIs and corporate FDs, with returns of up to 12.5% p.a. Sign up today!

FAQs On Mutual Fund Vs Property Investment

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001