Equity Mutual Fund Taxation: How Are Equity Mutual Funds Taxed In India?

Equity mutual fund taxation rules trigger upon selling or transferring units rather than at the time of purchase.

However, the purchase or allotment date is important because it marks the beginning of the holding period.

Under the Income Tax Act, 2025, effective from 1 April 2026:

- Units held for up to 12 months are treated as short-term.

- Units held for more than 12 months are treated as long-term.

These rules generally apply to equity-oriented funds that invest at least 65% of their proceeds in listed shares of domestic companies.1 Tax applies only to the gain earned, not the full redemption amount.

The tax treatment varies based on how long the units were held and whether the investor redeems units or receives an IDCW payout.

How Equity Mutual Funds Are Taxed?

The tax on equity mutual funds changes according to the holding period and how investors receive money from the scheme.

Transaction | Holding period | Tax treatment in 2026 |

| Redemption | Up to 12 months | STCG taxed at 20% |

| Redemption | More than 12 months | LTCG taxed at 12.5% on aggregate eligible gains exceeding INR 1.25 lakh |

| IDCW distribution | Not applicable | Taxed at the investor’s applicable slab rate |

These are base rates. The final tax payable may be higher after adding the applicable surcharge and 4% health and education cess.2 The following scenarios show how the rules work in actual transactions.

Selling Within The Short-Term Holding Period

A redemption made before completing 12 months places the resulting gain in the short-term category. Where Securities Transaction Tax applies, Section 196 taxes it at 20%. 3

Suppose an investor purchases equity mutual fund units for INR 2 lakh and redeems them for INR 2.30 lakh after 11 months. As the investor redeemed the units before completing one year, the profit falls under STCG.

Particulars | Amount |

Purchase value | INR 2,00,000 |

Redemption value | INR 2,30,000 |

Short-term capital gain | INR 30,000 |

Tax at 20% | INR 6,000 |

Health and education cess at 4% | INR 240 |

Total tax payable | INR 6,240 |

This STCG on equity funds calculation assumes that no surcharge applies. Tax is charged only on the INR 30K gain, not on the full redemption value of INR 2.30 lakh.

Selling After The Long-Term Holding Period

For units retained beyond one year, LTCG on equity mutual funds applies. The 12.5% tax is charged only on aggregate eligible long-term gains exceeding INR 1.25 lakh in the tax year.4

The exemption limit applies to the investor’s total eligible LTCG for the year. It is not available separately for each mutual fund scheme.

Scenario 1: LTCG Below INR 1.25 Lakh

Suppose an investor earns total eligible LTCG of INR 1.10 lakh during the tax year. Since the gain remains within the exemption limit, no LTCG tax applies.

Particulars | Amount |

Total eligible LTCG | INR 1,10,000 |

Exempt amount | INR 1,10,000 |

Taxable LTCG | Nil |

Tax at 12.5% | Nil |

Health and education cess at 4% | Nil |

Total tax payable | Nil |

Scenario 2: LTCG Above INR 1.25 Lakh

Suppose the investor earns total eligible LTCG of INR 1.60 lakh during the tax year. Only the INR 35,000 exceeding the exemption limit is taxable.

Particulars | Amount |

Total eligible LTCG | INR 1,60,000 |

Annual exemption limit | INR 1,25,000 |

Taxable LTCG | INR 35,000 |

Tax at 12.5% | INR 4,375 |

Health and education cess at 4% | INR 175 |

Total tax payable | INR 4,550 |

These calculations assume that no surcharge applies.

Tax Treatment Of The IDCW Option

IDCW stands for Income Distribution cum Capital Withdrawal. Under this option, the mutual fund distributes part of the scheme’s available surplus to investors. The fund house decides whether and when to make the distribution.

An IDCW payment is not an additional return. The scheme’s NAV generally falls after the distribution because money moves out of the fund.

For example, suppose an investor holds 1000 units of a scheme with an NAV of INR 20. The total investment value is INR 20,000.

If the fund declares IDCW of INR 1 per unit:

Particulars | Amount |

Units held | 1000 |

IDCW per unit | INR 1 |

IDCW received | INR 1,000 |

NAV before IDCW | INR 20 |

Indicative NAV after IDCW | Around INR 19 |

The investor receives INR 1,000, but the value of the remaining units may fall to around INR 19,000. Actual NAV movement may differ because of market changes and applicable adjustments.

Unlike profits from redeeming units, IDCW is not treated as a capital gain. For resident investors, it is added to taxable income under “income from other sources” and taxed at the applicable slab rate.

The mutual fund deducts TDS at 10% when aggregate covered IDCW income exceeds INR 10,000 during the tax year.5 TDS is an advance deduction. The final tax liability depends on the investor’s applicable slab rate.

From 1 April 2026, investors also cannot claim a deduction for interest expenses against taxable income received from mutual fund units.

The basic mutual fund capital gains tax rules are straightforward, but certain situations creates nuanced approach. These situations show how the rules apply in practice.

Tax Situations Investors Often Overlook

The equity mutual fund tax calculation can become more detailed when investors use SIPs, switch schemes, redeem only part of their units or start regular withdrawals. Each transaction must be examined separately.

SIP Investments And FIFO

Every SIP instalment is treated as a separate purchase. Each instalment has its own allotment date, cost and holding period.

When an investor redeems units, the First In, First Out, or FIFO, method applies. This means the units purchased earliest are treated as redeemed first.

Suppose an investor makes the following purchases:

Purchase date | Units purchased | Purchase NAV | Investment cost |

January 2025 | 100 | INR 100 | INR 10,000 |

January 2026 | 100 | INR 110 | INR 11,000 |

In September 2026, the investor redeems 150 units at an NAV of INR 140. FIFO applies as follows:

Units redeemed | Units selected under FIFO | Type of gain | Capital gain |

First 100 units | January 2025 purchase | Long-term | INR 4,000 |

Next 50 units | January 2026 purchase | Short-term | INR 1,500 |

Total | 150 units | Mixed gains | INR 5,500 |

The first 100 units were held for more than 12 months. The next 50 units were held for less than 12 months.

If the investor has no other eligible LTCG, the INR 4,000 long-term gain remains within the INR 1.25 lakh exemption. The INR 1,500 short-term gain is taxable at 20%, resulting in base tax of INR 300.

Switching Between Mutual Fund Schemes

A switch from one scheme to another is not tax-neutral. The switch-out is treated as a redemption from the original scheme.

The amount invested in the new scheme is treated as a fresh purchase. It receives a new acquisition cost and allotment date.

Suppose an investor switches units worth INR 1.80 lakh after investing INR 1.50 lakh ten months earlier.

Particulars | Amount |

Cost of units in the original scheme | INR 1,50,000 |

Value on the switch date | INR 1,80,000 |

Short-term capital gain | INR 30,000 |

Base tax at 20% | INR 6,000 |

Cost of units in the new scheme | INR 1,80,000 |

The investor may owe tax even though the money did not enter a bank account. The holding period for the new scheme starts from the switch date.

Redeeming Only Part Of The Investment

A partial redemption does not make the entire withdrawal taxable. Tax applies only to the gain included in the units redeemed.

Suppose an investor buys 1,000 units at INR 100 each. After the NAV rises to INR 130, the investor redeems 300 units.

Particulars | Amount |

Units redeemed | 300 |

Redemption value at INR 130 per unit | INR 39,000 |

Cost at INR 100 per unit | INR 30,000 |

Capital gain | INR 9,000 |

Although the investor receives INR 39,000, only INR 9,000 is the capital gain. The remaining INR 30,000 represents the original investment cost.

FIFO decides which units are redeemed when purchases were made on different dates. The holding period of those selected units then determines whether the INR 9,000 is short-term or long-term.

Tax Implications Of Systematic Withdrawals

A Systematic Withdrawal Plan, or SWP, allows investors to withdraw a fixed amount at regular intervals. Each withdrawal is treated as a separate redemption.

Suppose an investor originally purchases units at INR 100 each. When the NAV reaches INR 120, an SWP instalment of INR 12,000 is processed.

Particulars | Amount |

SWP amount | INR 12,000 |

NAV on the withdrawal date | INR 120 |

Units redeemed | 100 |

Cost of redeemed units | INR 10,000 |

Capital gain | INR 2,000 |

Tax applies only to the INR 2,000 gain, not the full INR 12,000 withdrawal. If the units were held for up to 12 months, the gain is short-term. Units held for more than 12 months may produce LTCG.

Where an investor has purchased units through several SIP instalments, different SWP payments can produce a mix of short-term and long-term gains.

Now, these situations show where tax can arise during routine mutual fund transactions. The next is to use this interpretation while planning redemptions and other investment decisions.

How To Make Tax-Efficient Mutual Fund Decisions

Tax efficiency begins with planning the transaction rather than calculating the bill after redemption.

Plan The Holding Period

Check which units FIFO will select. Waiting until units cross 12 months may reduce the rate from 20% to 12.5%, but liquidity needs and market risk should come first.

Time Redemptions Carefully

Review eligible LTCG already booked during the tax year. Where appropriate, redemptions may be spread across different tax years to use the INR 1.25 lakh annual threshold.

However, delaying a necessary withdrawal may expose the investment to further market movements. Tax savings should be weighed against that risk.

Maintain Complete Records

Keep consolidated account statements, capital-gain reports, SIP dates, purchase NAVs and redemption details.

Units acquired on or before 31 January 2018 require extra attention because grandfathering rules may affect their cost of acquisition.6 For eligible units, the calculation may consider the fair market value as of 31 January 2018 instead of relying only on the original purchase price.

Investors should therefore retain the original purchase records, the NAV or fair market value on 31 January 2018 and the final redemption details. Missing information can lead to an incorrect capital gains calculation.

Avoid Unnecessary Tax Events

Before switching, starting an SWP or changing investment options, review tax and exit load together. Unplanned transactions may create avoidable gains even when the money remains invested.

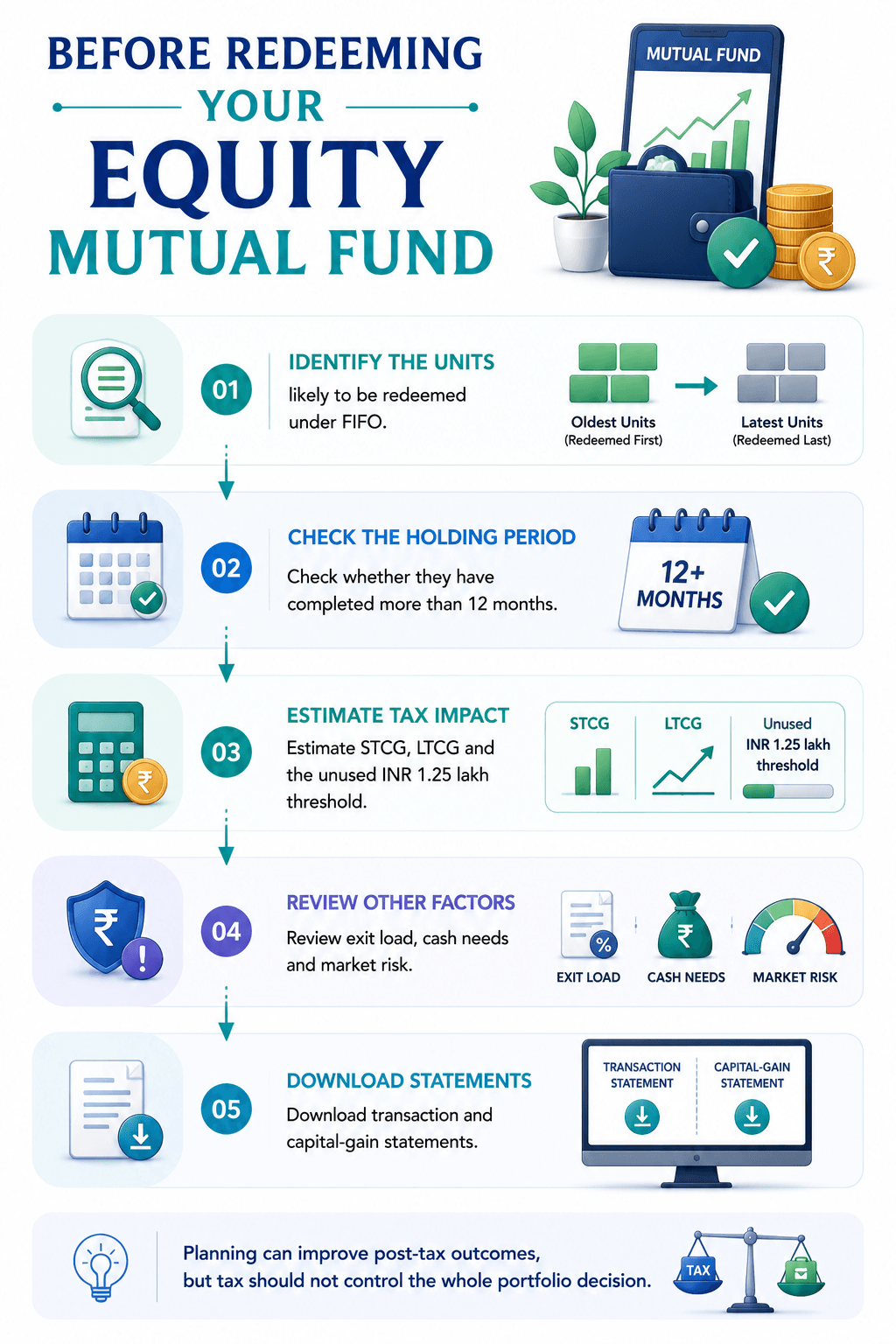

Before Redeeming Your Equity Mutual Fund

- Identify the units likely to be redeemed under FIFO.

- Check whether they have completed more than 12 months.

- Estimate STCG, LTCG and the unused INR 1.25 lakh threshold.

- Review exit load, cash needs and market risk.

- Download transaction and capital-gain statements.

Planning can improve post-tax outcomes, but tax should not control the whole portfolio decision.

Tax Efficiency Is Only One Part Of Investing

Taxation affects post-tax returns, but investors must also examine how an investment fits into their broader portfolio.

A lower tax bill does not make an unsuitable fund suitable. Investors should assess diversification, volatility, investment horizon, liquidity and their financial objectives.

Equity funds may support long-term growth, while fixed-income products can serve income and stability needs.

You can find fixed-income opportunities corporate bonds on Grip Invest, offering yields of up to 12.5% p.a. Sign up today to compare available opportunities based on their returns, tenure and credit rating!

FAQs On Equity Mutual Fund Taxation

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001