FDR: Meaning, Types, Benefits And How Fixed Deposit Receipts Work

For conservative portfolios, fixed-income investments have long served as their financial foundation, providing consistent earnings and helping preserve capital. Out of various sources available, fixed deposits have remained a trusted avenue for retail and institutional investors alike.

However, when an investor deposits their capital in a bank for a predetermined tenure, they receive a document known as an FDR (Fixed Deposit Receipt) as proof of their deposit. FDR acknowledges the deposit and serves as documentary proof.

Understanding the FDR meaning, its functions, features and different forms can help investors in multiple ways. It also serves as a useful record for maintaining financial documentation and, in some cases, availing a loan against the fixed deposit.

FDR: What Is A Fixed Deposit Receipt?

In banking parlance, the FDR full form is Fixed Deposit Receipt. An FDR is an official document issued by a bank or an eligible deposit-taking NBFC acknowledging the receipt of a fixed deposit for a specified tenure.

A fixed deposit receipt typically includes key details such as the depositor's name, deposit or receipt number, principal amount, tenure, interest rate, deposit date, maturity date, maturity amount, and nominee details, where applicable.

Although the terms FD and FDR are often used interchangeably, they are not the same. An FD is the fixed deposit account that earns interest on the amount invested, whereas an FDR is the document issued as proof of that deposit.

The FDR may be issued in physical or digital form and serves as documentary evidence of your investment.

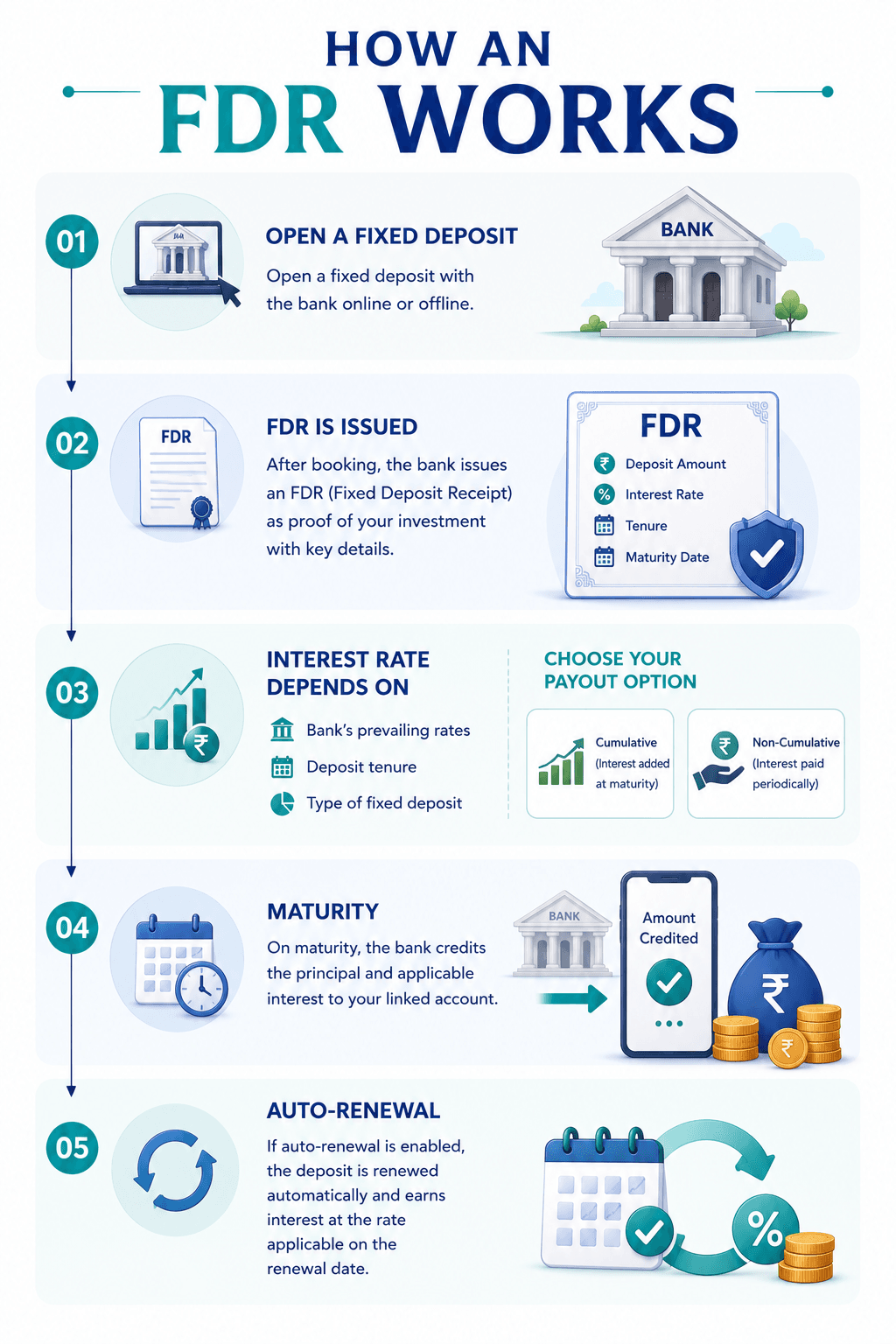

How Does An FDR Work?

An FDR is issued when you open a fixed deposit with a bank, either online or offline. The document records the key details of the deposit, including the deposit amount, interest rate, tenure, maturity date, and other relevant information.

Once the fixed deposit is booked, the bank issues the FDR as proof of the investment. The applicable interest rate depends on factors such as the bank's prevailing rates, deposit tenure, and the type of fixed deposit selected. You may also choose between cumulative and non-cumulative interest payout options based on your financial needs.

Upon maturity, the bank credits the principal and applicable interest to your linked account or automatically renews the deposit if auto-renewal is enabled. The renewed deposit will generally earn interest at the rate applicable on the renewal date.

For example, if you invest INR 5 lakh in a fixed deposit at an annual interest rate of 6% for three years (assuming annual compounding), the maturity amount will be approximately INR 5,95,508.

A table view of the Information mentioned on the FDR

| Information | Purpose |

| Receipt number | Unique reference number assigned to the fixed deposit |

| Depositor name | Helps identify the depositor |

| Deposited amount | The principal amount deposited in the FD |

| Interest rate | Applicable interest rate during tenure |

| Deposit date | Date when the FD begins |

| Maturity date | Date when the FD matures |

| Maturity amount | Amount payable on maturity, including principal and applicable interest |

| Nominee details | Helps facilitate payment to the nominee, where applicable |

| Branch number | To identify the issuing branch |

What Should You Verify on Your FDR?

After receiving your Fixed Deposit Receipt, review the document carefully to ensure all details are accurate.

Check:

| Item | Why It Matters |

| Depositor’s name | Should match your bank records and identity documents. |

| Deposit amount | Confirms the correct investment amount. |

| Interest rate | Ensures the agreed FD rate has been applied. |

| Deposit tenure | Verifies the chosen investment period. |

| Maturity date | Helps you plan withdrawals or renewals. |

| Nominee details | Reduces complications during claim settlement. |

| Auto-renewal instruction | Confirms whether the FD will renew automatically or mature into your account. |

Why Is An FDR Important?

Many investors simply keep an FDR as proof of their fixed deposit. However, the document serves several purposes beyond being a record of the investment.

1. Proof of Investment

The primary purpose of a fixed deposit receipt is to serve as documentary proof of your deposit. It helps you verify important details of the investment and can be useful while resolving any discrepancies with the bank.

2. Loan Against FDR

Many banks allow customers to avail of a loan against their fixed deposit by using it as collateral. Depending on the bank's policy, you may be able to borrow around 75% to 90% of the deposit value without prematurely breaking the FD (depending on the type of FD and the issuing financial institute’s terms and conditions). Such loans often carry lower interest rates than unsecured borrowing, making them a relatively cost-effective financing option.

3. Nomination Benefits

In the event of the depositor's demise, the nominee details recorded against the fixed deposit help the bank process the claim in accordance with applicable procedures. Keeping nomination details up to date can help avoid unnecessary delays.

4. Tax Purposes

Interest earned on fixed deposits is taxable as per the applicable income tax provisions. While the bank FDR can help maintain investment records, taxpayers generally rely on the annual interest certificate, bank statements, and other relevant documents while filing their income tax returns.

5. Digital vs Physical FDR

Most banks now issue digital FDRs through internet banking or mobile banking applications. These digitally authenticated receipts are generally considered equally valid as physical FDRs. They are also easier to access, store, and retrieve whenever required.

What Happens If You Lose Your FDR?

Losing a physical Fixed Deposit Receipt does not usually mean losing the fixed deposit itself because banks maintain records of all deposits.

If your physical FDR is lost, the bank may ask you to:

- Submit a written request.

- Provide identity verification.

- Complete any applicable declaration or indemnity documentation, depending on the bank's policy.

For digital FDRs, customers can generally download another copy through internet banking or the bank's mobile application.

The exact process may vary between banks.

Common Mistakes Investors Make With FDRs

Even experienced investors may overlook important details related to their bank FDR.

- For example, a common error is failing to track the maturity date. If no maturity instructions are provided and auto-renewal is enabled, the bank may renew the fixed deposit at the interest rate applicable on the renewal date, subject to its policy.

- Another common oversight is not updating nominee details after major life events, such as marriage or the birth of a child.

- Some investors also fail to compare interest rates offered by different banks before investing. Even a small difference in interest rates can significantly impact returns over longer investment tenures.

- Some investors do not safely store their physical FDR or save a copy of their digital receipt. Although banks maintain deposit records, obtaining duplicate documents may take additional time.

- Lastly, many investors overlook that premature withdrawal may incur penalties or lower interest, depending on the bank's terms and conditions.

FDR Checklist Before You Invest

- Compare FD interest rates offered by different banks.

- Check the deposit tenure and maturity date carefully.

- Add or update your nominee details, where required.

- Understand the bank's premature withdrawal rules and penalties.

- Keep a secure physical or digital copy of your FDR.

- Review the bank's auto-renewal instructions.

- Understand the tax implications on interest earned.

Beyond Traditional Fixed Deposits

Fixed deposits remain one of the most popular fixed-income investment options in India because they offer predictable returns with relatively lower risk. Investors looking to diversify their fixed-income portfolios may also consider alternatives such as corporate bonds and Corporate Fixed Deposits (CFDs).

Platforms like Grip Invest allow investors to compare corporate bonds and other fixed-income products with traditional FDs based on factors such as credit rating, issuer quality, expected yield, and investment tenure. Comparing different investment options can help investors build a diversified portfolio aligned with their financial goals and risk appetite.

FAQs On Fixed Deposit Receipt

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001