Debt Fund vs FD: Which Is Better For Investing in 2026?

Should you lock your money into an FD when banks are still offering around 6% to 7%, or keep it in a debt mutual fund where returns can move with the bond market? That is the real Debt fund vs FD question for 2026.1Both are seen as low risk investments, but they do not work the same way.

A fixed deposit gives a known rate, while a debt fund gives flexibility, market-linked returns and different tax treatment. To understand which option fits better, start with how both products actually work.

What Is A Debt Fund?

A debt mutual fund mainly invests in fixed-income instruments such as treasury bills, government securities, certificates of deposit, commercial papers and corporate bonds.

Under SEBI’s mutual fund classification, debt funds are grouped by where they invest and how long they hold securities. Here are some of the major types of debt funds:

Type of debt fund | What it usually invests in |

Overnight fund | Securities maturing in 1 day |

Debt and money market securities maturing within 91 days | |

Ultra-short term fund | Debt and money market instruments with 3 to 6 months Macaulay duration |

Short term fund | Debt and money market instruments with 1 to 3 years Macaulay duration |

At least 80% in AA+ and above rated corporate bonds | |

Banking and PSU debt fund | At least 80% in debt instruments of banks, PSUs, public financial institutions and municipal bonds |

At least 80% in government securities |

Debt fund returns are market-linked. They can move with interest rates, bond prices and the credit quality of securities in the portfolio. For example, as of 8 July 2026, liquid funds delivered 6.14% over one year and 6.80% over three years, while corporate bond funds delivered 5.13% over one year and 7.19% over three years.2

What Is A Fixed Deposit?

A fixed deposit is a bank deposit where the investor locks money for a chosen tenure and earns a fixed interest rate. The return is known at the time of booking, which makes FDs simpler for conservative investors.

For example, SBI offers 6.25% for one year to less than two years for general customers below INR 3 crore.3 Therefore, if someone invests INR 1 lakh for one year at 6.25%, he/she will know upfront that the annual interest will be around INR 6,250 before tax.

Why Do Investors Compare Them?

Investors compare FD vs debt fund because both are used for relatively low risk investments, but their returns are built differently. An FD locks the interest rate on the day of investment. A debt fund value moves with bond yields, interest-rate expectations and the securities held in the portfolio.

In June 2026, the RBI kept the repo rate unchanged at 5.25%. This means FD rates may remain broadly steady unless banks revise their deposit rates separately.4 Debt funds, however, can still move based on bond-market conditions, inflation expectations and the fund’s maturity profile. So, the choice is not only between two return numbers. It is between a known return and a market-linked return.

Here is a return snapshot to frame the debate between debt fund returns and fixed deposit returns.

| Return view | Liquid funds | Corporate bond funds | Banking and PSU funds | Major bank FD range |

| 1-year return / rate | 6.14% | 5.13% | 5.07% | ~6.25% -6.5% |

| 3-year return / mid-tenure rate | 6.8% | 7.19% | 7.03% | ~6.25% - 6.6% |

| 5-year return/ long-tenure rate | 6.06% | 6.1% | 6.06% | ~6% - 6.25% |

The table shows that FDs currently look competitive on one-year returns because the rate is fixed upfront. Debt funds become more relevant when investors need liquidity, diversification or a longer holding period where bond-market returns may change.

Therefore, the debt fund vs fixed deposit decision should not stop at the headline return.

To make a fair choice, investors need a complete comparison.

Debt Fund vs FD: Complete Comparison

The real difference between a debt fund vs fixed deposit becomes clearer when returns, risk, liquidity and taxation are seen together.

| Factor | Debt fund | Fixed deposit |

| Returns | Market-linked. Example: Liquid funds show 6.14% one-year return, corporate bond funds 5.13% and credit risk funds 8.08%.5 | Fixed at booking. Example: SBI offers 6.25% to 6.4% across key 1-3 year slabs, while Canara Bank offers 6.25% for one year and 6.60% for 555 days.6 |

| Risk | Carries interest-rate, credit and liquidity risk. Returns can move up or down. | Lower risk when held with a scheduled bank, but deposit insurance applies only up to the specified limit per depositor per bank. |

| Liquidity | Usually redeemable on business days, though exit loads may apply in some categories. For example, Bandhan Liquid Fund charges an exit load from Day 1 to Day 6, starting at 0.007% on Day 1 and becoming nil after that. | Premature withdrawal is allowed in most callable FDs but may reduce the effective rate. For example, SBI charges a 0.50% penalty for premature withdrawal of FDs up to INR 5 lakh. |

| Taxation | Debt funds that fall under specified mutual funds are covered by Section 50AA. If acquired on or after 1 April 2023, their gains are treated as short-term capital gains and taxed as per the investor’s income tax slab. | Interest earned from fixed deposits is treated as income from other sources. It is added to the investor’s total income and taxed as per the applicable slab. For bank FDs, TDS applies if annual interest exceeds INR 50,000 for regular investors and INR 1,00,000 for senior citizens.7 |

| Lock-in period | No fixed lock-in for most open-ended debt funds. | Tenure is chosen upfront. Tax-saving FDs carry a five-year lock-in. |

| Inflation protection | Better scope if yields move favourably, but not guaranteed. | Limited, because the rate is fixed and post-tax return may fall below inflation. |

Note: The comparison highlights that neither option is universally better. Fixed deposits generally offer greater certainty, while debt funds provide more flexibility and diversified exposure to fixed-income securities.

The appropriate choice depends on whether the investor values predictable returns, liquidity, inflation protection or portfolio diversification.

When Should You Choose A Debt Fund?

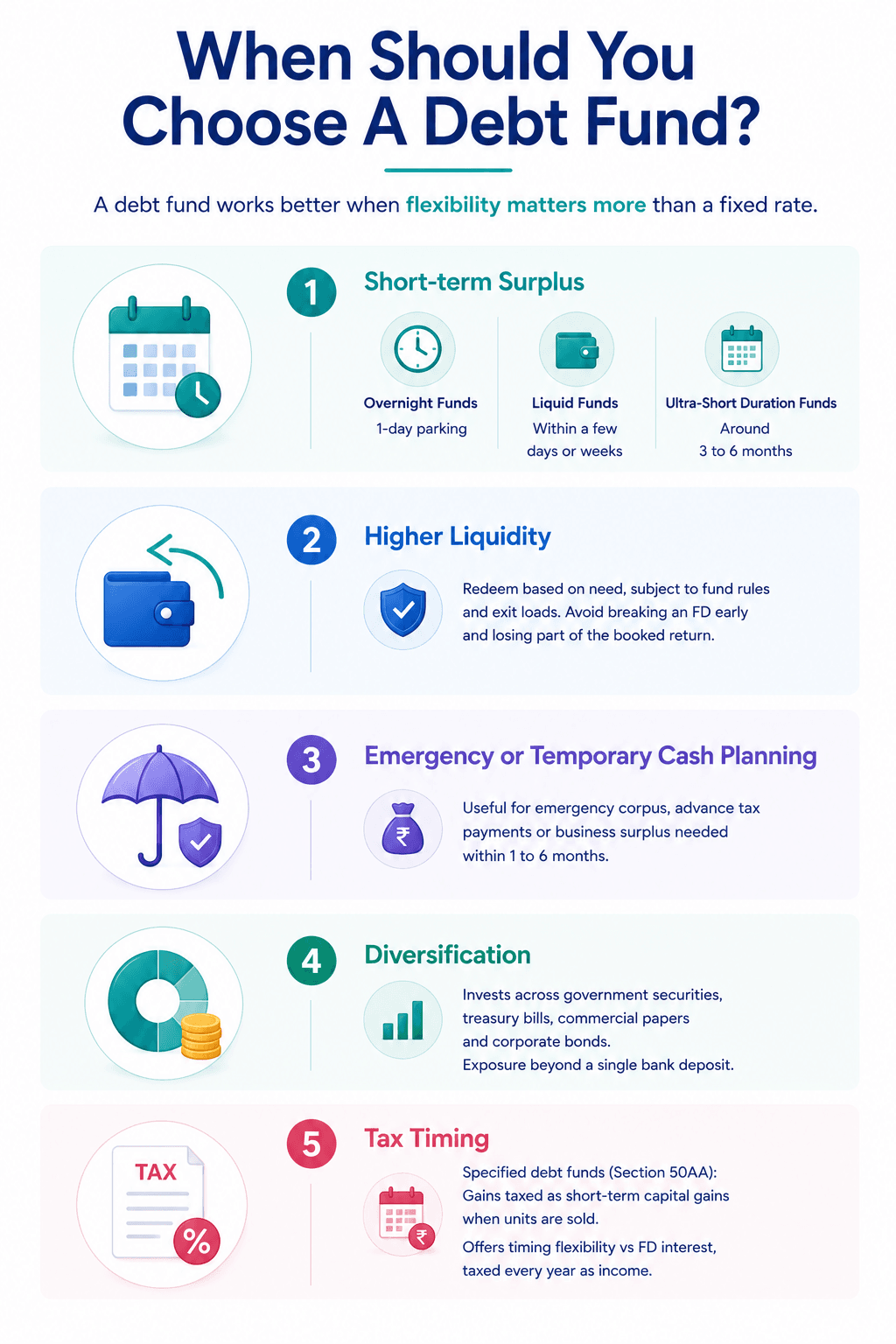

A debt fund works better when flexibility matters more than a fixed rate.

1. Short-term surplus: You may choose a debt mutual fund for parking short-term surplus if the money may be needed soon. For example, Investors can use overnight funds for 1-day parking, liquid funds for money needed within a few days or weeks, and ultra-short duration funds for around 3 to 6 months.

2. Higher liquidity: Debt funds can be redeemed based on need, subject to fund rules and exit loads. This helps investors avoid breaking an FD early and losing part of the booked return.

3. Emergency or temporary cash planning: Debt mutual funds can be useful for emergency corpus, advance tax payments or business surplus that may be needed within 1 to 6 months.

4. Diversification: Debt funds invest across different fixed-income instruments such as government securities, treasury bills, commercial papers and corporate bonds. This gives investors exposure beyond a single bank deposit.

5. Tax timing: For specified debt funds covered under Section 50AA, gains are taxed as short-term capital gains when units are sold. This may offer timing flexibility compared with FD interest, which accrues every year and is taxed as income.

When Is A Fixed Deposit A Better Choice?

An FD is better when certainty matters more than flexibility. Here are the main situations where it may work better:

- Known maturity value: A fixed deposit gives the rate at the time of booking.

- Near-term goals: FDs suit goals with a clear timeline, such as school fees due in 6 to 12 months, a house rent deposit, wedding expenses or money needed within 1 to 3 years.

- Senior citizen income: FDs may suit senior citizens who want predictable interest. Many banks offer around 0.5% extra interest to senior citizens over regular FD rates, which can improve post-retirement cash flow.

- Low monitoring: FDs work well for investors who do not want to track NAV, fund duration, credit rating changes, yield-to-maturity or exit loads.

- Capital certainty: The trade-off is clear. Investors get a fixed return, but they may lose some liquidity and inflation protection compared with other fixed income investments.

Debt Fund vs FD vs Corporate Bonds

Corporate bonds add a third option for investors who want direct exposure to debt securities.

| Factor | Debt funds | Fixed deposits | Corporate bonds |

| Return potential | Moderate and market-linked. | Fixed. | Can be higher than FDs, depending on issuer and rating. |

| Risk | Spread across many securities, but NAV can move. | Lower volatility, especially when held to maturity. | Issuer-specific credit and liquidity risk. |

| Liquidity | Usually better than direct bonds for retail investors. | Premature closure depends on bank rules. | May be limited if the bond is not actively traded. |

| Ideal investor | Wants liquidity and diversification. | Wants certainty and simple returns. | Understands credit rating, maturity and issuer risk. |

Which Option Is Right For You?

The right choice depends on the job your money must do.

Use FDs for goals where capital certainty matters. Use debt funds for short-term parking, flexible withdrawals and portfolio diversification.

For a basic investor, the answer is simple. If you cannot accept any movement in value, FD is easier. If you can accept mild fluctuation for liquidity and possible return flexibility, a debt fund may fit better.

Building A Diversified Fixed Income Portfolio

A balanced fixed-income portfolio need not choose only one product.

A cautious investor may keep emergency money in a savings account or liquid fund, near-term goal money in FDs and a small allocation in high-quality debt funds. A more informed investor may add short-duration funds, corporate bond funds or select listed bonds after checking risk.

In 2026, the Debt fund vs FD choice depends on the role each product plays in a portfolio. FDs can anchor the stable part of the portfolio, while debt funds can help with liquidity, short-term parking and wider fixed-income exposure.

A prudent portfolio can use both in the right proportion.

Before investing in any fixed-income product, compare expected returns with the associated risks, liquidity and taxation. A side-by-side comparison of different fixed-income options can help investors make more informed decisions based on their financial goals.

FAQs On Debt Fund vs FD

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001