50 Lakh FD Interest Per Month: How Much Income Can You Earn

The eventual aim of investments is to generate consistent income and attain predetermined financial goals. Irrespective of risk-taking ability, any investor would want the principal corpus to be secure and invested in an asset that can generate a fair amount of monthly income to help reach financial milestones such as retirement planning, higher education, or children’s marriage (or other goals).

In this context, Fixed Deposit has been a highly reliable investment for investors across categories.

If you are looking for a consistent, secure, and predictable income and have a fair bit of investment at your disposal, you might ask: What will I gain from a 50 lakh FD interest per month?

The answer depends on a variety of factors: the effective interest rate on the FD, the investor's tax bracket, payout options, FD tenure, etc. Let us break down the actual numbers and evaluate whether a INR 50 lakh FD can truly support your financial goals.

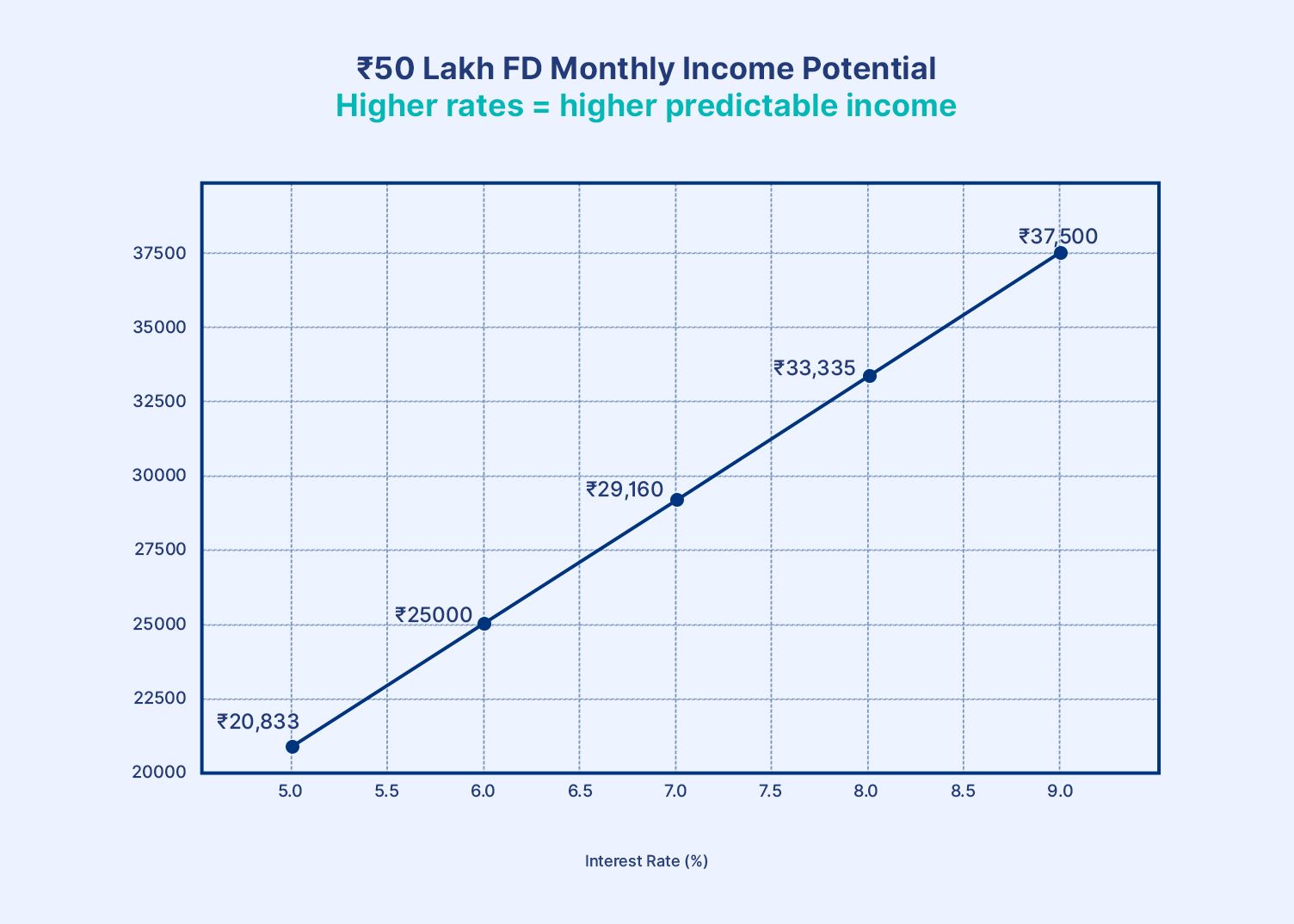

Figure 1.0: Approx. Monthly Income from INR 50 Lakh FD

Monthly Interest On INR 50 Lakh FD

1. Basic Calculation Explanation

You can simply compute the annual interest by multiplying the principal by the effective annual interest rate. The resulting annual interest is divided by 12 to obtain the monthly interest.

The framework is simple and enables an investor to estimate fixed-deposit income and understand how rate changes affect earnings.

2. Income at Different Interest Rates

Depending on the effective rate of interest, here is how much you can earn from a INR 50 lakh FD per month:

Interest Rate | Annual Interest | Monthly Income |

6% | INR 3,00,000 | INR 25,000 |

7% | INR 3,50,000 | INR 29,167 |

8% | INR 4,00,000 | INR 33,333 |

Here, the 50 lakh FD monthly interest at 7 percent is close to INR 29167 compared to INR 25000 at 6% rate of interest. The implication is that a small increase in the interest rate can help raise monthly income to a sustainable level.

Moreover, FD returns India depend upon various issuers such as banks, financial institutions, and corporate FDs. Each category has different interest rates and risk levels that suit a class of investors.

How FD Monthly Interest Works

1. Monthly Payout vs Cumulative FD

Fixed Deposits are broadly classified into cumulative and non-cumulative deposits. For Cumulative FDs, interest is compounded for each compounding period and is paid at maturity. For non-cumulative fixed deposits, interest is paid periodically. In the long term, the total returns on cumulative deposits are higher than those on non-cumulative deposits. However, an investor needs to wait a certain period before receiving interest.

Hence, if you are looking for regular cash flows, you should choose a non-cumulative alternative.

2. Monthly Income Option

If you have chosen the monthly payout or non-cumulative option, there is an option to choose the time at which the interest is credited to your account. It can be monthly, quarterly or annually, depending on the terms and conditions of the fixed deposit.

Many investors compare options such as SBI 50 lakh FD monthly payout, HDFC 50 lakh FD interest per month, or ICICI 50 lakh FD monthly returns to evaluate consistency and reliability across banks. You can choose a quarterly or monthly option, depending on your lifestyle requirements.

Factors That Affect Monthly Income

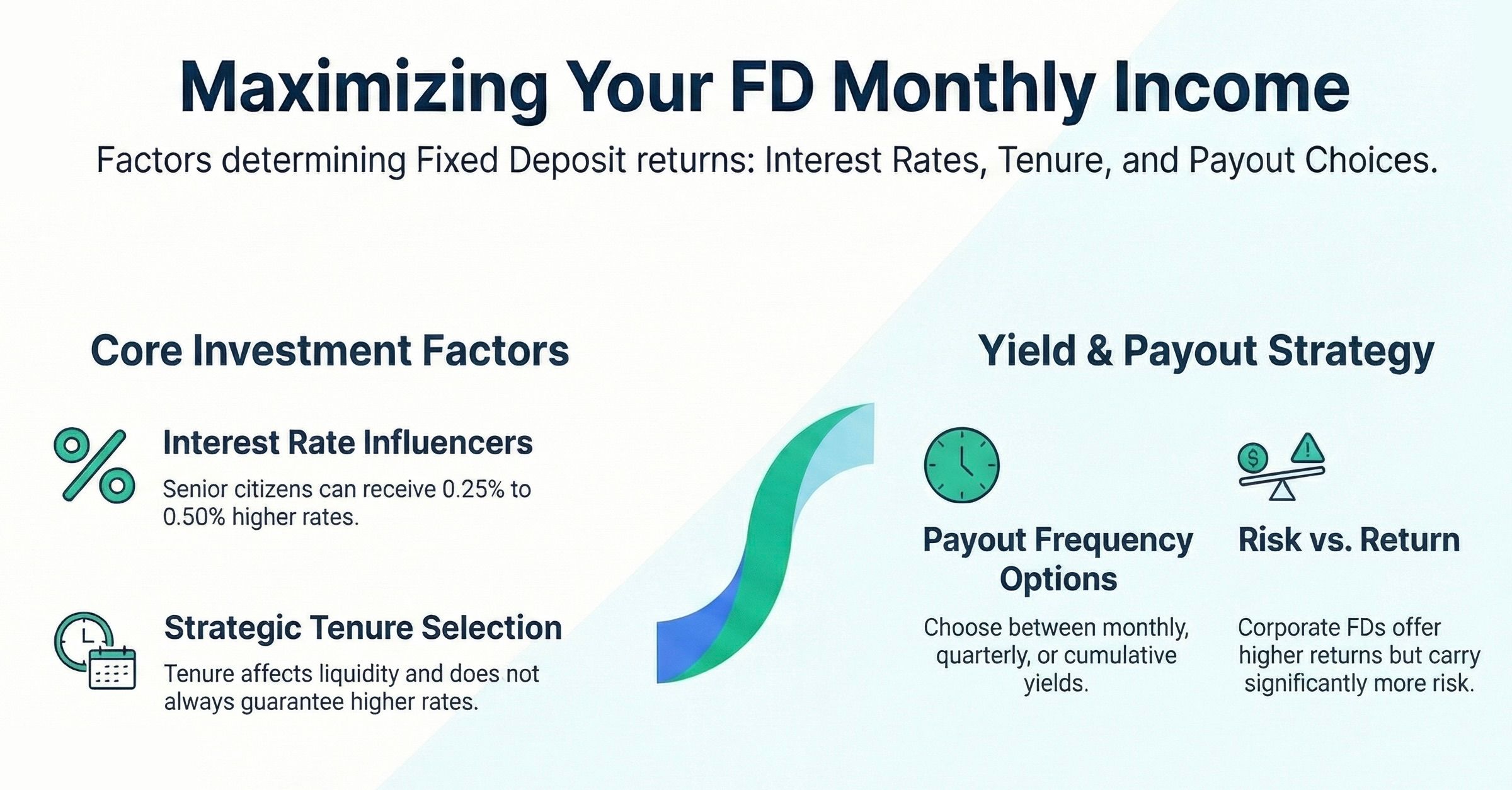

1. Interest Rates

As shown in Figure 1.0, a slight change in the interest rate can result in an increase (or decrease) in an individual's effective monthly income. You should also remember that 50 lakh FD interest for senior citizens is slightly higher (0.25-0.50%), which could have a critical impact on the interest income (monthly).

It is also crucial to select the best bank for 50 lakh FD monthly income. There are multiple options available, and you can also consider other financial institutions and corporate FDs, as those could offer a higher return, but the risk undertaken is also higher.

2. Tenure

Tenure plays a critical role in determining returns. While longer tenures may offer higher rates, they also reduce liquidity. However, it is not a rule that a higher tenure would always result in a higher rate of interest. You should check the effective ROI for your chosen tenure before making the investment decision.

3. Interest Payout Frequency

With Fixed Deposits, you can get regular income through monthly payouts. You also have the option to opt for a quarterly payout, which can increase yield potential. Further, there is a cumulative option with a greater compounding benefit.

Is FD Enough For Passive Income?

1. Inflation Impact

FDs are critical for providing stable, risk-free returns and could be an excellent addition to your portfolio. However, you must consider the impact of inflation, as it reduces the actual ROI and returns on your fixed deposit. So, if the economy posts higher inflation numbers, it simply means the actual purchasing power of your income remains unchanged, and attaining the long-term financial goals could be difficult.

2. Taxation

The tax on 50 lakh FD interest income depends on your income slab, and if you fall in, for instance, a 30% tax slab, the real return from your fixed deposit could be considerably lower than your anticipation. It is always advisable to consult your tax advisor and financial planner regarding the actual impact of income tax on your investments.

3. Diversification Angle

It is quite common to use FDs as a base layer in a portfolio. FDs can easily complement high-yield investments and provide consistent returns while maintaining stability. You can also use a 50 lakh FD calculator online, which helps compare scenarios across interest rates and tenures.

Conclusion

Having a fixed deposit as part of your portfolio and long-term investment plans can be an excellent idea. If you have a INR 50 lakh fixed deposit, it is possible to earn a monthly income between INR 25000 and INR 33000, depending on the ROI, tenure, and other terms and conditions of the deposit. You can consider banks, financial institutions, and corporate FDs for your fixed deposit needs. You can combine FDs with other high-yield, low-risk fixed-income securities, such as bonds and debentures, that you can find on the Grip Invest platform.

FAQs 50 Lakh FD Interest Per Month

1. How much interest does INR 50 lakh FD generate monthly?

A INR 50 lakh FD can generate around INR 25,000-INR 33,000 per month, depending on the interest rate (typically 6%–8%). Higher rates lead to higher monthly payouts.

2. Which bank gives the highest FD interest?

Interest rates vary across banks and NBFCs. Generally, small finance banks and NBFCs offer higher rates than large public sector banks, but investors should balance returns with safety and credibility.

3. Is FD good for a monthly income?

Yes, FDs are suitable for a stable and predictable monthly income, especially for conservative investors. However, returns may be limited after inflation and taxes, so they are often used alongside other income-generating investments.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001