Professional Tax In India: Meaning, Slab Rates And Rules (2026)

Professional tax is a state-level levy on income earned through salary, employment, profession, trade or business. In professional tax India rules, the amount is usually small, but it affects regular salary deductions and employer compliance.

This PT tax is not the same as income tax. It depends on the state professional tax law, the employee’s salary bracket, and the applicable professional tax slab.

Professional Tax: Meaning And Who Needs To Pay It?

To understand the levy properly, it is important to start with its legal base and practical use.

Professional tax is a statutory levy imposed by state governments or local bodies on earnings from employment, business or professional activity. Article-276 of the Constitution permits its collection on professions, trades, callings and jobs, with the annual amount capped at INR 2500 for each person.1

The word “professional” can be misleading. It does not only cover doctors, lawyers, consultants or chartered accountants. A salaried employee to a self-employed person also comes under professional tax rules if the state law applies.

States levy this tax because it gives them a local revenue source. The amount collected may support state or municipal functions, depending on how the relevant law is framed. The tax is easier to collect from salaried employees because employers deduct it from monthly salaries and remit it to the state.

Moreover, professional tax applies only in states that levy it. If a person works in a state where the law does not impose it, there may be no PT tax deduction in the salary slip.

How Professional Tax Works in Practice?

For most salaried employees, professional tax is one of the smallest deductions on a monthly salary slip. The employer calculates the applicable amount based on the state's professional tax slab, deducts it from the employee's salary and deposits it with the respective state government. Employees usually do not need to make a separate payment unless they are also liable as self-employed professionals under the relevant state law.

Who Is Liable To Pay Professional Tax?

Liability depends on the person’s work status, income level and state of employment.

For salaried employees, the employer usually deducts the applicable amount from salary. In Karnataka, for example, the law says the employer must deduct tax payable by a salary or wage earner before salary is paid, and the employer remains liable to pay it on behalf of employees.

For self-employed persons, the responsibility is different. They may need to obtain enrolment and pay the tax directly through the state portal. Karnataka’s law separates employer registration from enrolment by persons who are liable but are not salaried employees covered by employer deduction.

The following groups may fall under the levy, depending on the state:

- Salaried employees in private or government jobs

- Employers responsible for salary deductions

- Freelancers and consultants

- Doctors, lawyers, architects and accountants

- Traders, shop owners and business entities

- Companies, firms, LLPs and partners where state law provides

Professional Tax Rates Across States

The rates are not uniform across India, so taxpayers should check the state where they work or operate.

The Constitution sets the upper limit at INR 2,500 per person per year, but states decide slabs, exemptions and payment cycles. Some states use monthly salary slabs. Others, such as Kerala and Tamil Nadu, may follow half-yearly income slabs. This is why two employees with the same salary can see different deductions in different states.

Here are a few of the state-wise professional tax rates as of 8 July 2026:

State | Salary or income slab | Professional tax amount | Payment pattern |

Maharashtra

| Men: less than or equal to INR 7500 monthly | Nil | Monthly |

Men: INR 7501 - INR 10000 | INR 175 per month (pm)2 | Monthly | |

Men: > INR 10000 | INR 200 pm, INR 300 in February | Monthly | |

Women: less than or equal to INR 25000 | Nil | Monthly | |

Women: > INR 25000 | INR 200 pm, INR 300 in February | Monthly | |

Karnataka | Salary or wages of INR 25000 and above | INR 200 pm, INR 300 in February 3 | Monthly |

Telangana

| Less than or equal to INR 15000 | Nil | Monthly |

INR 15001 - INR 20000 | INR 150 pm | Monthly | |

> INR 20000 | INR 200 pm 4 | Monthly | |

West Bengal | Existing salaried slab above INR 40000 | INR 200 pm 5 | Monthly |

Kerala | Half-yearly income of INR 125000 and above | INR 1,250 per half year 6 | Semi-annual |

Gujarat | Monthly salary above INR 12000 | INR 200 pm 7 | Monthly |

Note: The comparison highlights that professional tax is not a uniform national levy. Two employees earning the same salary may pay different amounts depending on the state where they are employed. This makes the employee's work location just as important as the salary level when calculating professional tax.

Here is how the calculation works. If an employee in Maharashtra earns INR 60K per month, the professional tax slab is above INR 10,000. The deduction is INR 200 for 11 months and INR 300 in February. The annual total becomes INR 2500.

This is also why the February salary slip may show a slightly higher PT tax deduction in some states.

Professional Tax and Income Tax: What Is The Difference?

The two taxes often appear together in salary discussions, but they work very differently.

| Point of comparison | Professional tax | Income tax |

| Levying authority | State government or local authority | Central Government |

| Legal basis | Article 276 and state laws | Income Tax Act |

| Applicability | Depends on state and income slab | Applies based on taxable income |

| Calculation | Fixed slab or state-specific rate | Slab-based income computation |

| Maximum limit | INR 2,500 per year | No such fixed cap |

| Salary treatment | Deducted from salary where applicable | TDS may be deducted from salary |

| Deduction benefit | Allowed as a professional tax deduction from salary income | Separate income-tax rules apply |

The professional tax deduction under income tax is important. The Income Tax Department states that professional tax paid by an employee through salary deduction is allowed as a deduction from taxable salary income. Even if it is paid in advance during the year, it can be deducted from salary income.

Section 16 also refers to deduction of tax on employment within the meaning of Article 276.

Therefore, professional tax reduces take-home salary first. Later, the amount paid can reduce taxable salary income while calculating income tax.

Common Misconceptions About Professional Tax

- Professional tax is not the same as income tax.

- It is not charged only on doctors or lawyers.

- Paying professional tax does not replace income tax.

- The maximum professional tax payable is capped at INR 2,500 per year under Article 276.

- Not every Indian state levies professional tax.

Things Taxpayers Should Know

This levy is small, but errors can still create compliance issues for employers and taxpayers.

1. Registration: Employers generally need a professional tax registration certificate in states where the levy applies. Self-employed persons may need enrolment instead. In Karnataka,8 the law requires employers liable under the Act to obtain registration, while non-salaried liable persons must obtain enrolment.

2. Compliance varies by state: Some states require monthly payments, while others follow half-yearly cycles. Kerala’s official profession tax portal states that the tax is paid on a semi-annual basis and depends on income slabs set by the state government.

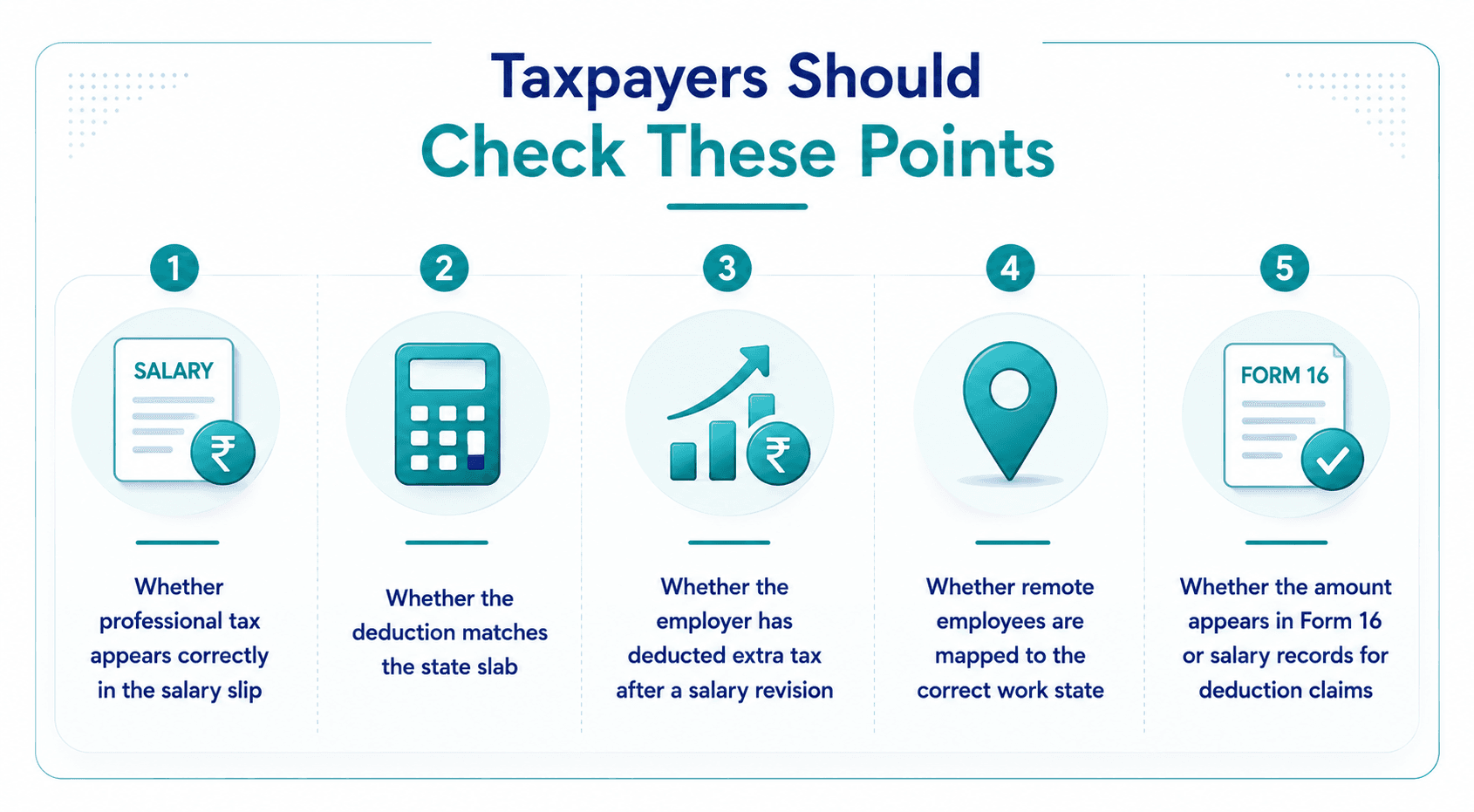

Taxpayers should check these points:

- Whether professional tax appears correctly in the salary slip

- Whether the deduction matches the state slab

- Whether the employer has deducted extra tax after a salary revision

- Whether remote employees are mapped to the correct work state

- Whether the amount appears in Form 16 or salary records for deduction claims

3. Multi-state companies: A business with employees in Maharashtra, Karnataka and Telangana may need to follow three different slab systems. Payroll teams should not use one national rate because professional tax rules are state-specific.

4. Penalties: The penalties vary by state. Therefore, as a rule of thumb, always check the latest state portal, not only old payroll templates.

What Should Employees Do After Understanding Professional Tax?

Professional tax is unavoidable where it applies, but tax planning should not stop there.

For most salaried people, the annual impact is capped at INR 2,500. That is modest compared with income tax, insurance, investments, housing rent, retirement contributions and loan repayments. Still, small deductions add up, and every salary component should be checked.

A tax-efficient portfolio should begin with clarity on salary deductions, taxable income and available deductions. After that, investors can plan across stable income-generating instruments such as corporate bonds, securitised debt instruments and other regulated opportunities.

Platforms such as Grip Invest can help investors explore curated fixed income options based on return expectation, tenure and risk appetite. Sign up today!

FAQs On Professional Tax

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001