Section 80CCD Deduction: NPS Tax Benefits And Limits

Section 80CCD of the Income Tax Act offers tax deductions for contributions made towards pension schemes notified by the central government, primarily the National Pension System (NPS). It is designed to encourage long-term retirement savings while helping taxpayers reduce their taxable income.

As a sort of retirement savings scheme, section 80CCD deductions apply to both salaried and self-employed individuals who contribute to NPS accounts.

It is divided into three parts, 80CCD(1), 80CCD(1B), and 80CCD(2). Each of these covers a different type of contribution. Understanding how these deductions work can help taxpayers make better use of available benefits and avoid missing additional savings opportunities.

80CCD(1): Deduction For Employee/Self-Employed NPS Contribution

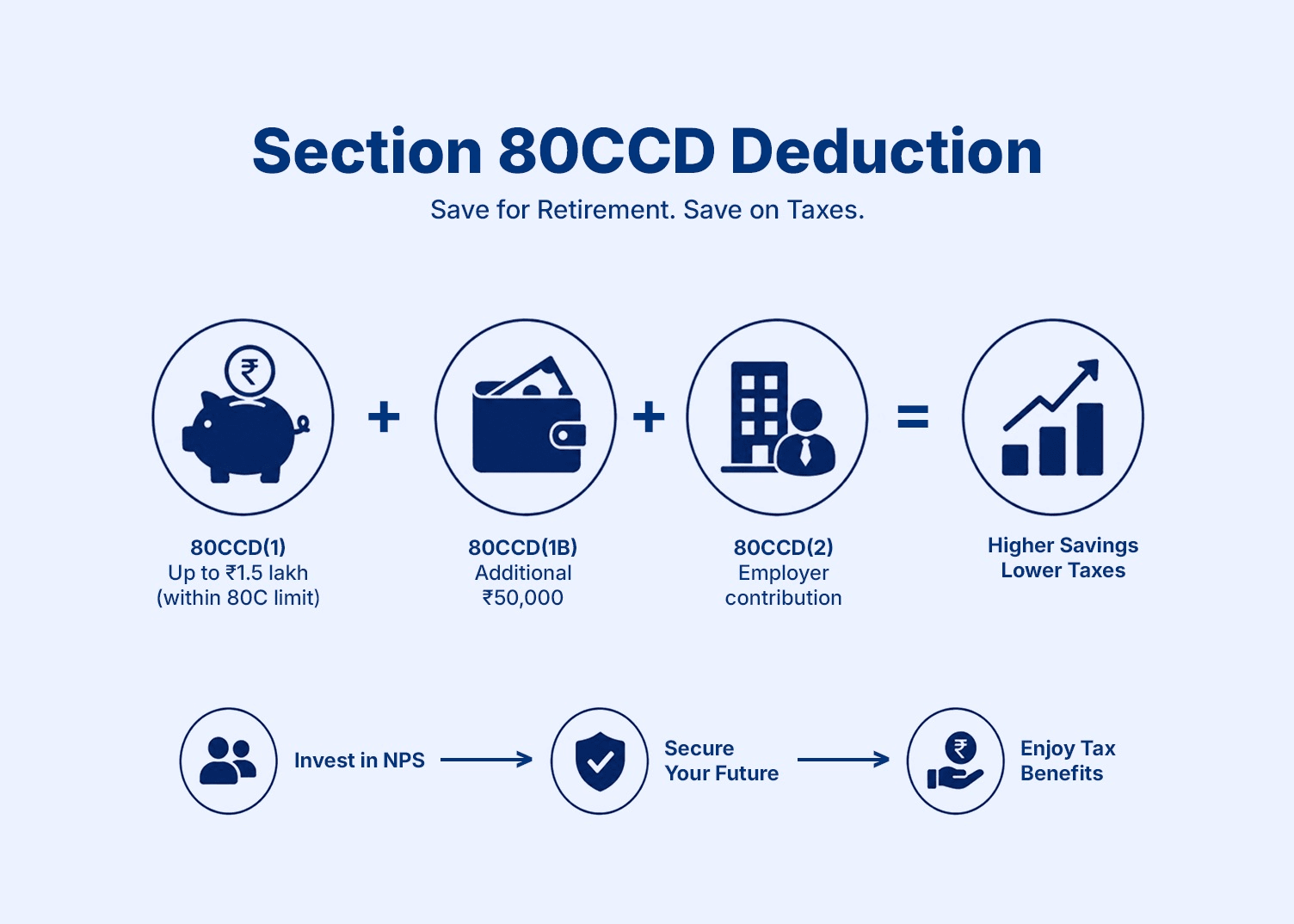

Section 80CCD(1) covers contributions made by an individual to their NPS account. This will include both salaried and self-employed individuals.

- For salaried employees, the deduction is available for contributions of up to 10% of salary, where salary includes basic pay and dearness allowance.

- For self-employed individuals, the deduction can be claimed for contributions of up to 20% of gross total income.

Beyond these, there is an overall limit of INR 1.5 lakh under this section, which is shared with Sections 80C and 80CCC. This means that the overall deduction that a taxpayer can claim under the section, along with 80C and 80CCC, cannot exceed INR 1.5 lakh.

For example, if you invest INR 1.2 lakh in life insurance and INR 50,000 in NPS under 80CCD(1), then your total investment would be INR 1.7 lakh.

However, you can only claim INR 1.5 lakh under these sections.

Therefore, you must plan carefully if you have already invested in options such as life insurance, PPF, or tax-saving fixed deposits, as each investment reduces the deduction available.

80CCD(1B): The Extra INR 50,000 Deduction Most People Miss

One of the biggest advantages of investing in NPS is the additional deduction available under Section 80CCD(1B). This provision allows taxpayers to claim an extra 80CCD(1B) INR 50000 deduction for contributions made to their NPS account. This deduction is available over and above the INR 1.5 lakh limit covered under Section 80C and Section 80CCD(1).

This means someone who has already exhausted their Section 80C limit may still reduce taxable income further by contributing to NPS.

For taxpayers looking to maximize retirement savings while lowering tax liability, this is often one of the most useful yet overlooked provisions.

80CCD(2): Employer Contribution Available Under New Tax Regime Too

Section 80CCD(2) applies when an employer contributes to an employee’s NPS account. This benefit is available only to salaried individuals because self-employed taxpayers do not receive employer contributions. Just like 80CCD(1B) INR 50000 deduction, employer contributions can be claimed as a deduction separately from the limits under Section 80C and Section 80CCD(1B).

This makes it an additional tax-saving opportunity for employees whose organisations offer NPS benefits. The employer NPS contribution deduction remains available under the new tax regime, making it relevant even for taxpayers who choose not to claim several traditional deductions.

How 80CCD Interacts With 80C: Avoiding the Overlap Mistake

A common mistake taxpayers make is assuming all NPS contributions qualify separately. Under Section 80CCD(1), the deduction is part of the combined INR 1.5 lakh limit under Sections 80C, 80CCC, and 80CCD(1). If this limit has already been used through other tax-saving investments, there may be little room left for additional deductions here.

However, Section 80CCD(1B) offers a separate deduction of INR 50,000, which can be claimed independently. Understanding this distinction helps taxpayers avoid duplication errors and make better financial decisions.

NPS Tier 1 vs Tier 2: Which Qualifies for Deduction

Before understanding how section 80CCD NPS deduction works under NPS Tier 1 vs Tier 2 accounts, let's first understand what NPS Tier 1 vs Tier 2 accounts are:

NPS Tier 1

NPS Tier 1 is the primary retirement account. It comes with withdrawal restrictions and is meant for long-term retirement savings. Contributions to this account qualify for tax deductions under Section 80CCD. The key features of these accounts are:

- It is a mandatory account if you want to invest in NPS

- It is designed for long-term retirement savings

- It is a lock-in period until age 60

- It has limited withdrawal options before retirement

NPS Tier 2

Unlike an NPS Tier 1 account, an NPS Tier 2 account is a voluntary savings account. It is linked to your Tier 1 account. It offers flexible withdrawals and works like an investment account, but it generally does not provide the same tax benefits. The key features of these accounts are:

- You can open it only if you already have an active Tier 1 account

- It works more like a flexible savings/investment account

- There is no lock-in period

- You can withdraw money whenever you want

Conclusion

Section 80CCD deductions are linked to contributions made towards eligible NPS accounts under government-notified pension schemes. The available tax benefits under Sections 80CCD(1), 80CCD(1B), and 80CCD(2) apply to qualifying NPS contributions made by employees, self-employed individuals, and employers. Before claiming deductions, taxpayers should carefully review their contribution details when filing returns to ensure they are claiming benefits under the correct section.

FAQs On 80CCD Deduction

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001