Annualised Yield: Meaning, Formula And Calculation With Examples

The growing sophistication of the Indian investment landscape has led to a wide array of securities, catering to unique investor needs. This expansion of investment opportunities is not limited to the market-linked assets but has penetrated the fixed-income securities market as well. The growing asset option in the fixed-income or debt category has created a need for a parameter of comparative research that can be uniformly applied across varying assets to standardise them and aid analysis.

One such metric is the annualised yield. It helps understand a key feature of these assets, that is, their fixed return. This blog decodes annualised yield in detail, through its meaning, formula, benefits, and more, to ensure an efficient investment decision-making process.

What Is Annualised Yield?

The standard annual return that an investor can anticipate from their fixed-income or debt security investment, taking into account factors like interest payments, price changes, and the time to maturity, is called annualised yield. It is the total return earned, expressed as a percentage, that helps comparatively analyse assets with different maturities or payment frequencies.

For instance, different bonds can have different maturity periods. Furthermore, it is not always necessary that a bond will be bought at issuance and held till maturity. In such a scenario, annualised yield helps standardise returns from varying bond fundamentals, whilst factoring in dynamic market conditions.

Let us take a look at its formula, along with an example, to get an illustrative and nuanced understanding of what annualised yield is and how it aids investment analysis.

Formula And Calculation

There are two annualised return formulas that can help compute the analysed yield.

1. Annualised Yield: It primarily helps standardise returns across different holding periods by converting any investment return into a yearly equivalent return. The formula for it is as follows.

For example, Mr A invested INR 10,000 in a bond. After 9 months, his return from the bond stands at INR 10,900. Therefore, the absolute return is INR 900 or 9%, but his annualised yield will be as follows.

This means that although the investment grew at 9% for 9 months (absolute return), if it had been growing at the same rate for one year, the yield would be approximately 12.1%.

2. Annual Percentage Yield: It is the compounding-based version of annualised yield. When interest is paid multiple times in a year, and each subsequent yield rate is levied on the principal along with the accumulated interest earnings from previous periods, the actual annual return is higher than the nominal rate declared. Given below is its formula.

Where,

r = Nominal annual interest rate, expressed in terms of decimals. For instance, 6% p.a. Interest becomes 0.06.

n = Number of compounding periods in a year. The table illustrates the value of n for different compounding tenures.

| n | Compounding |

| 1 | yearly compounding |

| 2 | Half-yearly compounding |

| 4 | Quarterly compounding |

| 12 | Monthly compounding |

For example, suppose Mr A invested in an FD that offers 8% interest compounded quarterly. Discussed below is his annual percentage yield.

Therefore, although the FD has a declared annual return of 8%, the actual effective yearly return is 8.24% because of compounding.

Although annualised yield can be used to compare different fixed-income securities or debt assets, let us scrutinise its use in two particular assets, that is, the FD and bond yield calculation in India.

Annualised Yield In Bonds And FDs

Annualised yield measures the effective annual return on investments like bonds and fixed deposits (FDs), accounting for compounding over a year.

- In the Case of Fixed Deposits

If the FD interest is compounded more than once a year, the actual return exceeds the annual rate of return declared. For instance, a 5% nominal rate compounded quarterly has an APY of 5.095%. As the compounding frequency increases, the actual yield derived from an investment also increases. The opposite holds when compounding frequency falls.

- In the Case of Bonds

Different bonds can have different coupon rates, maturity periods, price levels, and so on. Therefore, the yields of different bonds, which have different holding periods, are often converted into a yearly equivalent to aid comparison and optimal investment decision-making.

This leads us to the particular use cases of annualised yield, which must be explored to understand its advantages.

Why Annualised Yield Matters For Investors

Discussed here are different scenarios where annualised yield helps investors analyse investment options.

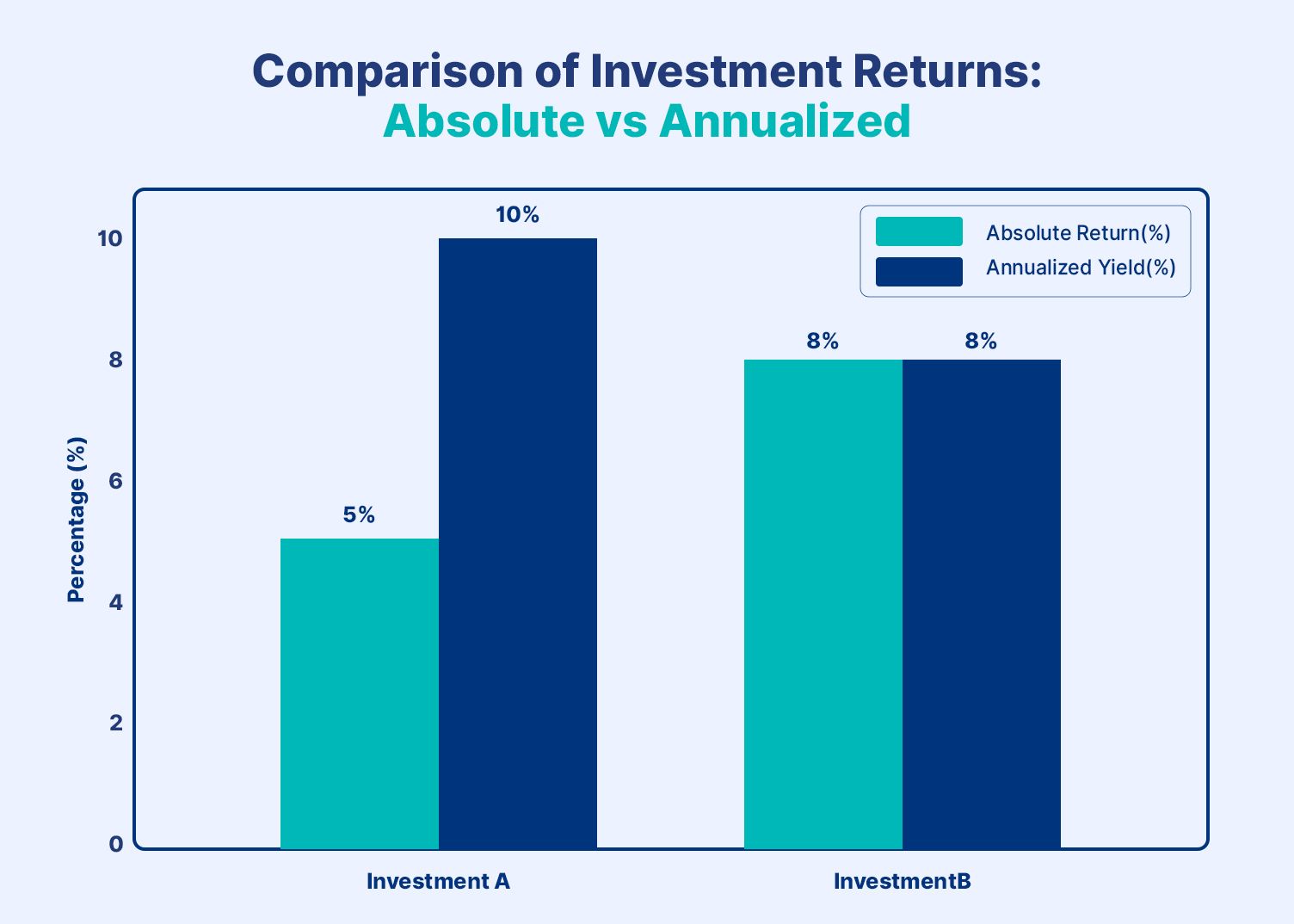

1. Comparing Investments Held for Different Time Periods

Investments can be held for different durations. Therefore, given the varying returns across different tenures, absolute return cannot decode which investment performed better.

For instance, investment A has delivered 5% return in 6 months, while investment B has delivered 8% return in 12 months. Given their varying tenure, it is unfair to compare 5% and 8%. Therefore, these absolute returns can be converted into yearly terms to aid comparison. The annualised yield of A and B is 10% and 8%, respectively.

Thus, though B has higher absolute returns, A performed better on a yearly basis.

2. Evaluating Bonds Bought or Sold Before Maturity

Investors often buy bonds in the secondary market or sell them early before maturity. Annualised yield helps calculate the effective yearly return for the actual holding period. For instance, Mr C bought a bond and sold it after 8 months with a 4% gain. To gauge its overall performance, Mr C can use the annualised yield. In this case, the annualised yield of 6% per year shows the real earning speed of the investment.

3. Comparing Different Asset Classes

A well-balanced portfolio often contains different kinds of assets. Annualised yield not only aids the comparison of investments within an asset class, but also helps compare different assets in general. It converts returns from different assets, like bonds, fixed deposits, debt funds, or short-term instruments, into one common annual metric, enabling meaningful comparison.

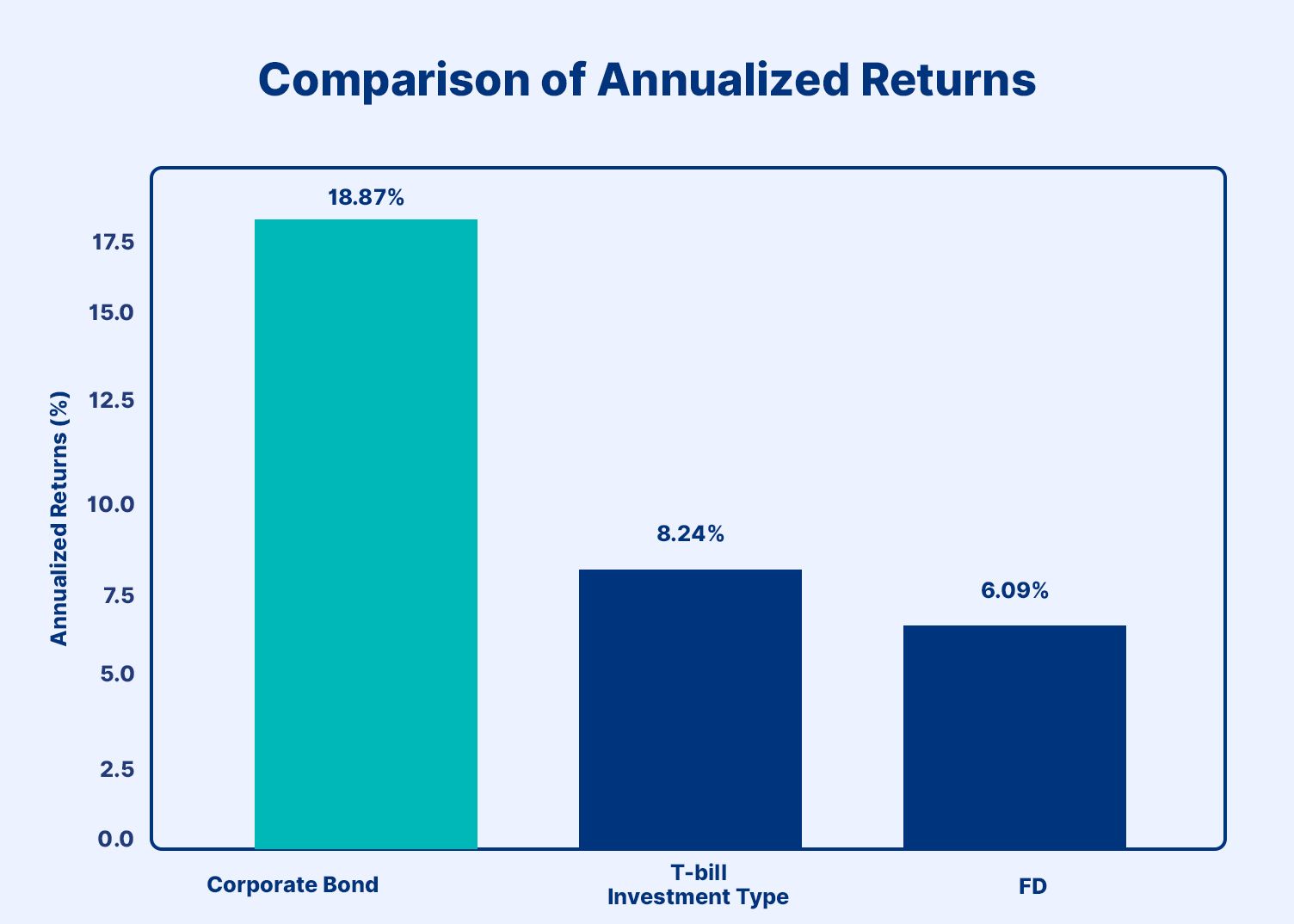

For example, Mr K wants to choose one among the following assets

- A treasury bill gave 2% return in 3 months,

- A corporate bond with 9% absolute return in 6 months, and

- A high-yield FD caries 6% interest per annum compounded half-yearly.

Therefore, he uses annualised yield to convert the returns into a yearly equivalent. The graph below shows the result.

Thus, Mr K chose to invest in the corporate bond.

4. Measuring Investment Performance Consistently

Portfolio performance tracking requires returns to be expressed on a yearly basis to understand whether investments are meeting the targets. For example, if a financial goal requires a 10% yearly return, an investment giving 7% in 6 months, that is approximately 14% annualised yield, indicates a performance above the target.

Despite these benefits, there are certain common mistakes that investors must avoid to ensure optimal utilisation of annualised yield.

Common Mistakes While Calculating

Discussed below are the common mistakes that must be avoided while calculating annualised yield.

1. Absolute Return vs Annualised Return: Often, investors confuse the absolute returns stated with the annualised return. This occurs particularly in the case of investments like FDs that have a per annum rate given, which, if compounded quarterly or semi-annually, has a distinct annualised return.

2. Ignoring the Exact Holding Period: Inability to convert the holding period, given in monthly terms, into a yearly value can cause arithmetic errors. For example, using 6 instead of 0.5 years in the formula for a 6-month holding period causes inaccurate results.

3. Comparing Investments Without Annualising Them: Investors often compare a 3-month return with a 1-year return directly, which gives misleading conclusions. Therefore, investors must always annualise the returns before comparing them.

4. CAGR vs Annualised Return: A unique relationship exists between the compound annual growth rate and annualised return. While mathematically they are similar concepts, their usage has a slight difference. CAGR measures the annual growth rate over multiple years, assuming profits are reinvested. Therefore, unlike annualised yield, CAGR is meaningful when the investment spans over more than one year; using it for, say, a 3-month holding period is technically incorrect.

Annualised return helps investors compare fixed-income opportunities on a like-for-like basis, making smarter allocation decisions easier. To simplify your fixed-return investing journey further, explore Grip Invest, a one-stop platform offering a curated range of assets such as high-yield FDs, corporate bonds, and other fixed-income instruments with yields of up to 12.5% YTM, all in one place.

Visit Grip Invest Today!

FAQs On Annualized Yield

1. What is annualised yield in simple terms?

Annualised yield is the yearly equivalent return of an investment. It shows how much an investment would earn in one year if it continued growing at the same rate, even when the actual holding period is shorter or longer than a year.

2. Is annualised return the same as CAGR?

Not exactly. CAGR is a type of annualised return used for multi-year investments, showing the smoothed yearly growth rate over several years. Annualised return, however, can be calculated for any holding period, even less than one year.

3. How to calculate annualised yield for bonds?

Annualised yield is calculated using the following formula.

Annualised Yield =(Ending Value/Beginng Value)1/Years Held-1

For bonds, the ending value includes interest earned plus price gain or loss, and the result is converted into a yearly return based on the holding period.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001