Best Investment Plans For Senior Citizens In India 2026 – Highest Safe Returns And Monthly Income

Introduction: Why Investing After 60 Needs A Different Lens

After 60, investing stops being about aggressive wealth creation and starts being about protecting what is already earned while generating reliable income. For most retirees, the best investment for senior citizens is therefore the one that keeps capital safe, pays on time, and at least tries to keep pace with inflation, not the one with the flashiest return on a brochure.

Rising healthcare costs, longer life expectancy and lower risk appetite make a stable senior citizen income plan essential, so that monthly expenses are covered without constantly worrying about market crashes1.

In India, 2025–26 is a favorable period for conservative investors, with relatively high interest rates on government-backed schemes and special senior citizen FDs, creating a strong base for safe investments for retirees. A practical retirement investment plan for seniors usually combines four buckets: government-backed schemes for safety, post office options for assured pay-outs, bank/NBFC deposits for flexibility, and a small allocation to low-risk mutual funds for gradual growth.

Because safety is non-negotiable, the natural starting point is government-backed schemes, which then become the core around which FDs, post office products and conservative mutual funds are added.

Government-Backed Schemes: Core Of A Senior Citizen Income Plan

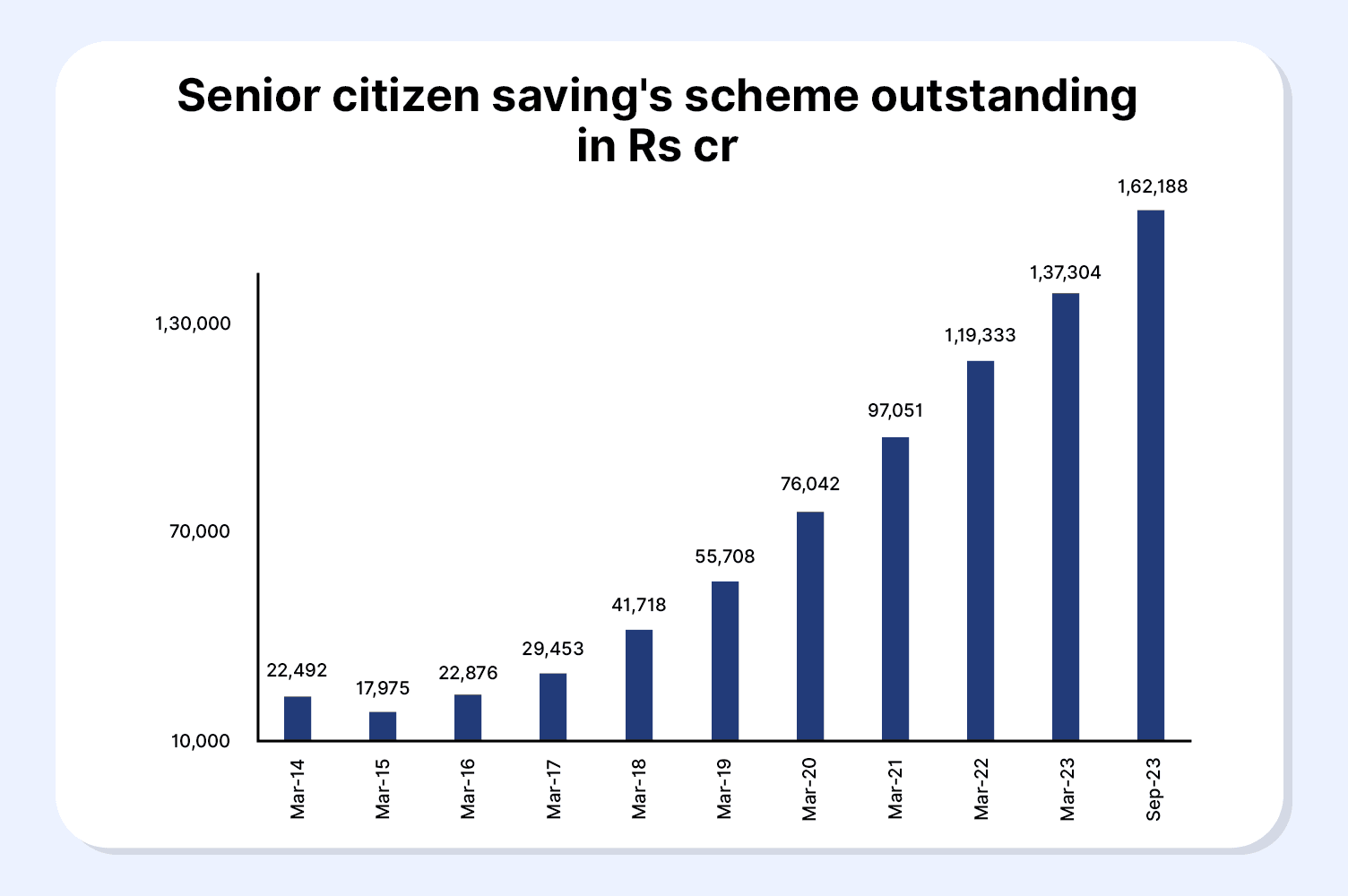

Government-backed schemes are the unbeatable foundation for safest investment options for elderly India—offering sovereign guarantee, stable rates, and clear exit rules. For retirees, three stand out: high-yield SCSS, pension-style PMVVY, and monthly-payout POMIS. Zero market risk, pure reliability. Next: SCSS at 8.2% p.a.2.

Source: Business standard3

1. Senior Citizen Savings Scheme (SCSS)

The Senior Citizen Savings Scheme (SCSS) is the top pick for the best investment for senior citizens, blending high 8.2% p.a. returns (Q2 FY 2025-26) with ironclad government security. The limit's now INR 30 lakh—ideal for couples to anchor retirement income needs. Quarterly payouts deliver steady cash flow without market volatility, reviewed every quarter for competitive rates. Perfect for seniors prioritizing safety and reliable income over risky bets4.

Interest under SCSS is paid quarterly, which suits retirees who need regular cash flows rather than annual lump sums.

Deposits qualify for Section 80C tax deduction up to INR 1.5 lakh, but the interest is fully taxable and subject to TDS once the total interest in a year crosses INR 50,000 for senior citizens. With a tenure of 5 years, extendable by 3 more years, SCSS can lock in attractive rates for a reasonably long period, which is useful when interest cycles may fall in future.

2. Pradhan Mantri Vaya Vandana Yojana (PMVVY)

PMVVY for senior citizens works more like a pension product offered by LIC but is effectively a government-backed retirement income plan. For FY 2025-26, the interest rate is around 7.4% per annum, translating to about 7.66% on a monthly payout basis, with a fixed 10-year policy term.

The scheme allows a maximum investment of INR 15 lakh per senior citizen, and the investor can choose monthly, quarterly, half-yearly, or annual pension payouts5.

Unlike SCSS, PMVVY does not offer 80C deduction on the invested amount, and the pension is fully taxable as income.

However, the predictability is a big plus: once locked in, the rate remains the same for the entire 10 year period, making PMVVY a strong pillar in long-term monthly income plans for retirees India. A practical structure is to use SCSS for higher immediate yield and PMVVY for long-term stability beyond the first 5–8 years of retirement.

3. Post Office Monthly Income Scheme: Simple Monthly Cash Flow

The Post Office Monthly Income Scheme is one of the most senior-friendly products because it directly answers the question, “Which investment gives monthly income?” As of 2025, the Post Office MIS interest rate stands at 7.4% per annum, payable every month, with a standard maturity period of 5 years. No TDS is deducted on the interest, which is helpful for tax planning, though the income itself is taxable as per slab.

The maximum investment limit under POMIS is typically INR 9 lakh for a single account and INR 15 lakh for a joint account, which can generate a meaningful monthly payout at current rates.

For example, a joint POMIS investment of INR 15 lakh at 7.4% can generate about INR 9,250 per month, forming a stable component of a senior citizen income plan without market-linked risk6. Many retirees combine POMIS with SCSS so that quarterly SCSS interest and monthly POMIS interest together meet routine expenses like utilities, groceries, and medicines.

Also Read: Your Comprehensive Guide To The ELSS Scheme For Tax Savings And Wealth Creation

Senior Citizen FDs And Bank Products

1. Senior citizen fixed deposit rates 2025

Bank and NBFC deposits remain one of the best investment plans for senior citizens in India 2026 because they are easy to understand, liquid, and widely accessible. Senior citizen fixed deposit rates 2025 are generally 0.50–0.75% points higher than regular rates, with many banks and NBFCs offering about 6.5%–8.75% per annum for senior citizens depending on tenure and issuer rating. Some leading private banks and high-rated NBFCs run special senior citizen FDs with promotional rates for medium tenures like 3–5 years, which can be attractive if the issuer is financially strong.

The best FD for senior citizens India should be chosen based on more than just rate: deposit insurance coverage, issuer’s credit rating, penalty for premature withdrawal, and whether monthly or quarterly interest payout is allowed. For retirees wanting monthly income, non-cumulative FDs with monthly payout are more suitable than cumulative ones, which are better for those still in the accumulation phase. Tax-saver FDs with 5year lock-in can provide 80C benefit but sacrifice liquidity, so they should be used only for a portion of the portfolio.

2. Senior citizen deposits with NBFCs and SDPs

Some NBFCs and fintech platforms now offer senior-focused fixed-income products like senior citizen bonds India, secured debt plans (SDPs), or curated bond baskets. Yields can be higher than traditional FDs—often in the 8%–10% range—but these carry issuer and credit risk, so they must be evaluated carefully, prioritizing AAA or AA-rated issuers with strong balance sheets. For conservative retirees, such instruments should be capped at a small portion of the overall portfolio, while the bulk stays in SCSS, POMIS, PMVVY, and bank FDs.

3. Safe market-linked options: Low-risk mutual funds

While capital protection is critical, putting 100% of money in fixed-rate products can make it hard to beat inflation over a 20-year retirement. That is why some of the best investments for senior citizens strategies include a limited allocation to senior citizen mutual funds, such as conservative hybrid funds, short-duration debt funds, or monthly income plans.

Conservative hybrid funds typically invest 75%–90% in debt and 10%–25% in equity, aiming to deliver modest growth with lower volatility than pure equity funds. Historically, such funds have delivered around 7%–9% annualized over long periods, but returns are not guaranteed and can be negative in the short term.

Therefore, these are better suited for the “growth bucket” of retirement investment plans for seniors 2025 onwards, not for essential monthly expenses. Systematic withdrawal plans (SWPs) from suitable debt or conservative hybrid funds can supplement, but not replace, guaranteed income from SCSS and PMVVY.

4. Tax-saving investments for seniors India

Tax planning is a critical part of evaluating the best investment for senior citizens because high interest income can push retirees into higher tax brackets. SCSS qualifies for 80C deduction, and so do 5-year bank tax-saver FDs and certain life insurance premiums, but PMVVY and Post Office MIS do not give 80C benefit on investment. Interest from SCSS, FDs, and POMIS is taxable, while some mutual fund categories enjoy more favorable capital gains treatment if held beyond specific periods.

Senior citizens can also benefit from higher basic exemption limits and specific provisions like deduction for health insurance premium and higher TDS thresholds on interest. At the portfolio level, using a mix of tax-efficient mutual funds for growth and taxable fixed-income for stability can optimize post-tax returns without compromising safety.

Also Read: SBI Senior Citizen FD Rates Guide

How To Structure A Sample Portfolio (Hypothetical)

Consider a 65-year old retiree with INR 50 lakh to invest and a goal of creating a predictable monthly income while keeping risk low. A possible allocation (illustrative, not advice) to balance safe investments for retirees and limited growth exposure could look like this:

- 30% (INR 15 lakh) in SCSS for high, government-backed quarterly income at 8.2% p.a.

- 20% (INR 10 lakh) in PMVVY for long-term, 10-year pension at 7.4% p.a.

- 20% (INR 10 lakh) in Post Office MIS at 7.4% p.a. for monthly income.

- 20% (INR 10 lakh) in senior citizen FDs (laddered across tenures) with 7%–8.5% rates for liquidity and flexibility.

- 10% (INR 5 lakh) in conservative hybrid or short-duration debt mutual funds for gradual growth and inflation cushion.

This type of structure answers three big retirement questions: stable monthly income, capital safety, and some inflation hedge, while keeping exposure to market volatility contained. Actual allocations should always be customized based on health, other income sources like pensions, and risk appetite.

| Scheme | Interest rate (% p.a.) | Notes |

| Senior Citizen Savings Scheme (SCSS) | 8.2% | Govt. small savings scheme; Q2 FY 2025-26 rate. |

| Pradhan Mantri Vaya Vandana Yojana | 7.4% | Pension-style scheme via LIC; fixed for 10 years. |

| Post Office Monthly Income Scheme | 7.4% | Monthly interest payout; 5-year tenure. |

| Senior citizen bank/NBFC FDs (range) | 6.5%–8.75% | Typical range across banks/NBFCs for seniors in 2025. |

Source: Paisabazaar7

Conclusion

Retirement planning after 60 isn’t about chasing the highest return—it’s about balance, predictability, and confidence. A thoughtful mix of SCSS, PMVVY, Post Office MIS, senior citizen FDs, and a small slice of low-risk mutual funds creates a stable financial foundation where monthly expenses are covered without stress. The right structure ensures your savings work for you while keeping capital protected for the long term.

If you’re looking to explore regulated, fixed-income options that offer transparency, curated issuers, and steady returns, platforms like Grip Invest help simplify the process. It provides access to well-researched fixed-income opportunities designed for investors who value safety and predictability—making it easier to build a stable and worry-free retirement income plan.

FAQs On Best Investment Plans For Senior Citizens In India 2026

1) Which investment is best for senior citizens who want monthly income?

If the goal is fixed monthly payouts, Post Office MIS and PMVVY are the most direct choices. Senior-citizen FDs with monthly interest payout options can also work well, especially when laddered across different tenures.

2) Are government schemes like SCSS and PMVVY completely risk-free?

Yes. Both are backed by the Government of India, which means the principal and interest are protected. While returns may be lower than market-linked products, the safety and predictability make them ideal core options for retirees.

3) Should senior citizens invest in mutual funds?

A limited allocation can help offset inflation, but it shouldn’t replace guaranteed income products. Conservative hybrid or short-duration debt funds should only be used as the growth portion of a retirement portfolio—not for essential monthly expenses.

References:

1. Upstox, accessed from: https://upstox.com/news/personal-finance/investing/senior-citizen-savings-scheme-7-things-senior-citizens-should-know-about-scss-going-into-2026/article-185761/

2. Policybazaar, accessed from: https://www.policybazaar.com/life-insurance/investment-plans/articles/post-office-monthly-income-scheme/

3. Business standard, accessed from: https://www.business-standard.com/finance/personal-finance/senior-citizen-deposits-total-rs-34-lakh-crore-a-150-growth-in-six-years-124041600326_1.html

4. Bajaj finserv, accessed from: https://www.bajajfinserv.in/investments/senior-citizen-savings-scheme

5. Kotak life, accessed from: https://www.kotaklife.com/insurance-guide/government-schemes/what-is-pradhan-mantri-vaya-vandana-yojana-pmvvy

6. KPIC, accessed from: https://kpic.co.in/post-office-monthly-income-scheme-2025/

7. Paisabazaar, accessed from: https://www.paisabazaar.com/saving-schemes/senior-citizen-savings-scheme/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001