SBI Senior Citizen FD Rates In 2026: Schemes, Returns And Tax Impact

Introduction: Why Senior Citizen FD Rates Matter

Financial planning for senior citizens in India revolves around stability, predictable income, and capital protection. After retirement, regular cash flows from safe investments become crucial because pensions and other sources often cover only part of living expenses.

Fixed deposits, especially those from large public sector banks like SBI, remain a preferred choice due to their assured returns, transparent terms, and strong perceived safety.

Fixed deposits have traditionally fulfilled this requirement. Their assured returns, fixed tenure, and straightforward structure make them a popular choice among retirees. Fixed deposits offered by major public sector banks, in particular, continue to be widely preferred due to their perceived safety, transparent terms, and long-standing trust.

State Bank Of India’s Fixed Deposits For Senior Citizens

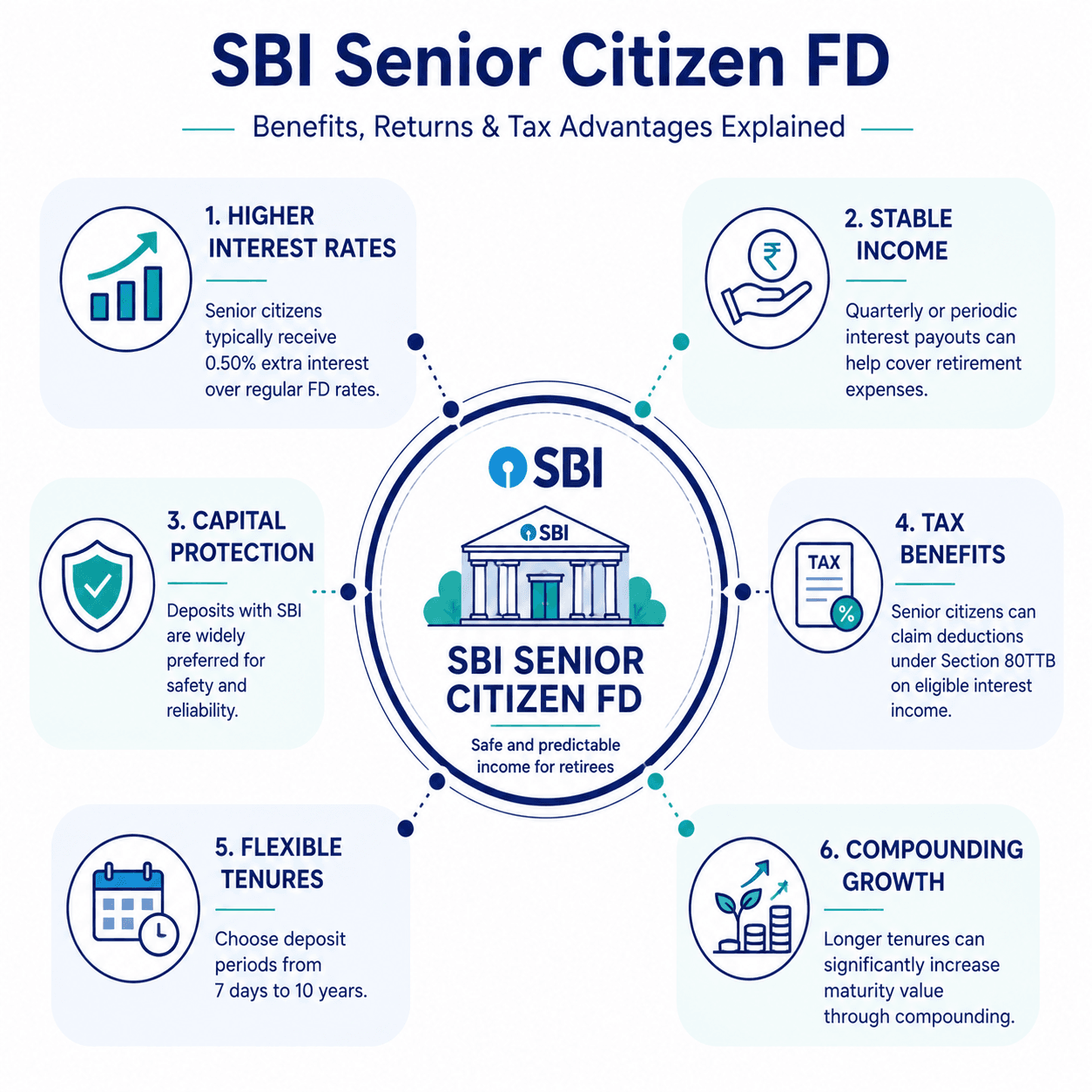

State Bank of India, the largest bank in the country, is generally considered one of the safest banks to keep FDs with. What makes SBI especially attractive for retirees is its special senior citizen pricing. Regularly, SBI senior citizen FD rates are higher than standard public rates; therefore, retirees can earn more interest on the same deposit amount.

Knowing how the SBI FD interest rates senior citizens work, what schemes are offered, how taxation is levied, and how inflation impacts real returns is crucial for anyone wanting to ensure that their retirement income is sufficiently stable and sustainable.

| Tenure | General Public (% p.a.) | Senior Citizen (% p.a.) |

| 7–45 days | 3.05% | 3.55% |

| 46–179 days | 4.90% | 5.40% |

| 180–210 days | 5.65% | 6.15% |

| 211 days–<1 year | 5.90% | 6.40% |

| 1–<2 years | 6.25% | 6.75% |

| 2–<3 years | 6.45% | 6.95% |

| 3–<5 years | 6.30% | 6.80% |

| 5–10 years | 6.05% | 7.05% |

| 444 Days (Amrit Vrishti) | 6.60% | 7.10% |

SBI Senior Citizen FD Rates Explained

SBI offers fixed deposits with a diverse range of tenures, from 7 days to 10 years. Senior citizens (persons aged 60 years and above) are allowed higher interest rates, as a matter of course, on all fixed deposits compared to those of normal customers. Most of the time, the advantage is about 0.50% per annum over the standard SBI FD rates, although that extra may vary during certain periods and promotional offers.

Under the regular SBI senior citizen fixed deposit scheme, interest rates generally range from around 3.55% for very short tenures to about 7.05% for long-term deposits of 5 to 10 years.

For instance, a one-year FD paying approximately 6.25% to the general public may pay around 6.75% to senior citizens. On special tenures such as the 444-day “Amrit Vrishti” deposit, senior citizens often receive rates above 7%, reflecting SBI’s attempt to attract long-term retail funds.

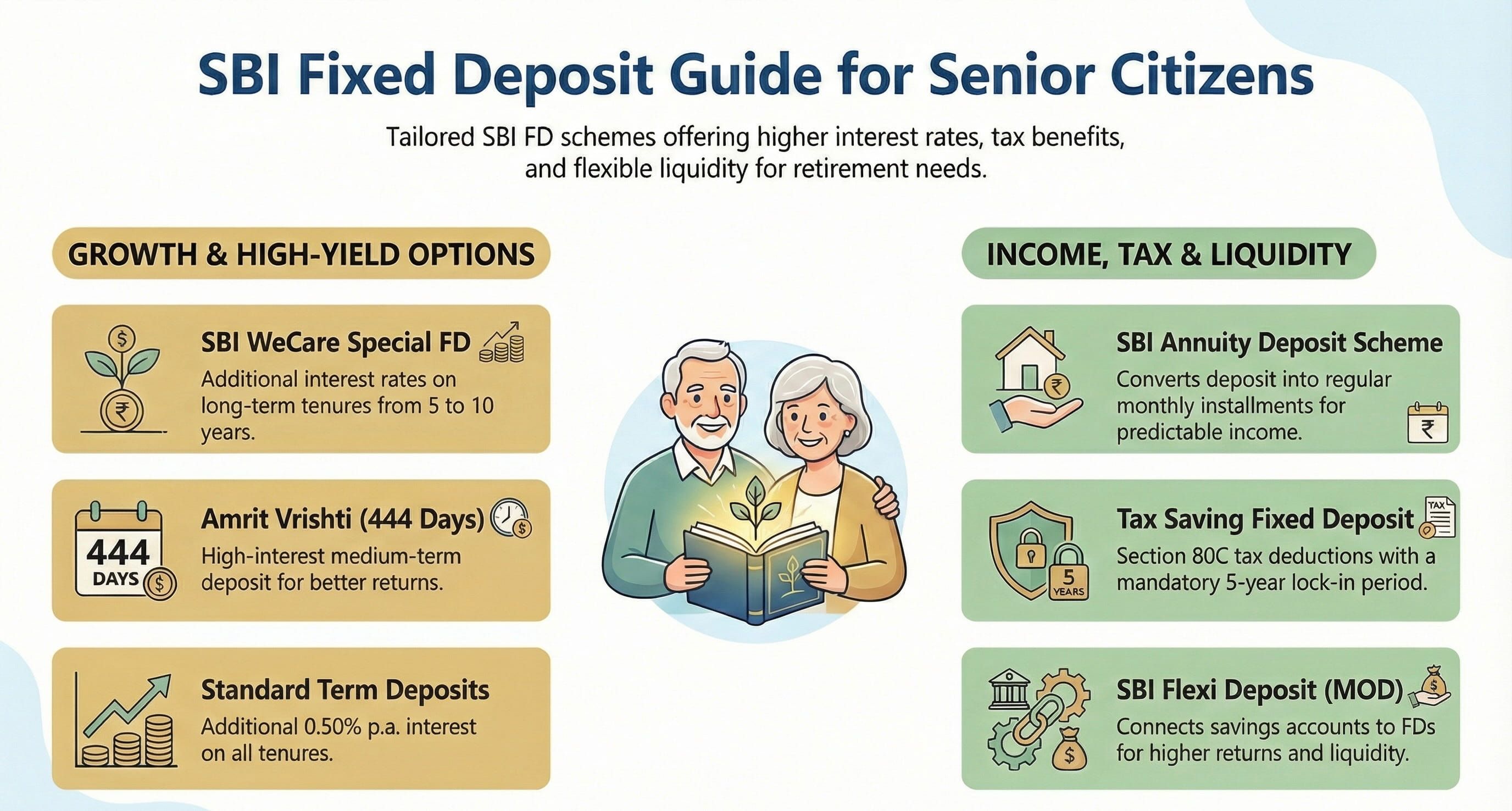

In addition to standard senior citizen deposits, SBI also periodically introduces enhanced schemes such as the SBI WeCare FD scheme. This product has been designed to offer extra interest on top of the usual senior citizen rates, particularly for longer tenures of 5 to 10 years.

As one of the best FD for senior citizens, WeCare options, interest rates might be approximately 7. 40% to 7. 60% per year, subject to the prevailing market situation.

Suppose the normal SBI senior citizen FD rate for a five-year deposit is 7.05%, the SBI WeCare FD scheme might offer about 7.50% for the same duration. With a 10 lakh deposit, this difference alone can boost annual interest income by around 4,500.

Tenure-Wise Returns For Senior Citizens

Understanding SBI senior citizen FD rates becomes clearer when translated into actual rupee returns. Suppose a retiree invests INR 10 lakh into a one-year SBI senior citizen FD at 6.75%. Over one year, the interest earned would be INR 67,500 before tax. If the individual chooses quarterly payouts, the income stream becomes predictable, which suits those funding regular household or medical expenses. Considering the recent changes in the tax slabs, it can be an excellent investment option for senior citizens who do not want to take too many risks on investments.

Now consider a longer investment horizon. A INR 10 lakh deposit placed into a five-year SBI senior citizen FD at approximately 7.05% would generate annual interest of about INR 70,500. Over five years, the total simple interest would exceed INR 3.5 lakh, while compounding could raise the maturity value to close to INR 13.9 lakh.

Tenure choice should probably be consistent with one's liquidity needs. Quick fixed deposits are perfect for your emergency fund, whereas medium-term fixed deposits can be used for income planning. Long-term fixed deposit returns India, especially with a scheme like SBI WeCare, is a perfect choice for capital preservation and the benefit of compounding of interest.

Before locking your funds, you may use SBI FD calculator to help determine, by entering the principal

Types Of SBI FD Schemes 2026

SBI offers multiple fixed deposit options tailored to different investment needs. For senior citizens, understanding these variants helps optimise returns while maintaining safety.

1. Regular Term Deposits

Standard fixed deposits with tenures ranging from 7 days to 10 years. Senior citizens earn higher interest rates (typically +0.50% p.a.) across all tenures.

2. SBI WeCare Senior Citizen FD

A special scheme for senior citizens offering additional interest over regular senior citizen rates, usually applicable on longer tenures (5 to 10 years).

3. Amrit Vrishti FD (444 Days)

A special tenure deposit designed to capture medium-term liquidity at attractive rates. Senior citizens receive a higher rate than the general public.

4. Tax Saving Fixed Deposit

A 5-year lock-in FD eligible for deduction under Section 80C (up to ?1.5 lakh). Senior citizen rates apply, though premature withdrawal is not allowed.

5. SBI Annuity Deposit Scheme

Designed to provide regular monthly income by splitting the deposit into instalments, suitable for retirees seeking predictable cash flows.

6. SBI Flexi Deposit (MOD)

Links savings accounts with FDs, allowing excess balances to earn FD returns while retaining liquidity.

Taxation Rules On Senior Citizen FD Interest

While SBI senior citizen FD rates are attractive, it is crucial to understand how interest is taxed:

Interest from fixed deposits is fully taxable under “Income from Other Sources” and is added to the senior citizen’s total income.

Section 80TTB of the Income Tax Act allows individuals aged 60 or more to claim a deduction of up to INR 50,000 per financial year on interest from bank FDs, RDs, and savings accounts (including post office deposits).

Taxation Of SBI Senior Citizen Fixed Deposit Interest (Illustrative)

| Particulars | Amount (INR) |

| Annual interest earned from FDs | 90,000 |

| Deduction under Section 80TTB | UP To 50,000 |

| Taxable interest after deduction | 40,000 |

| Tax payable (if total income within basic exemption limit) | NIL |

If you are a senior citizen or looking for an FD option for your senior citizen family members, we encourage you to consult your tax advisor to understand the pre and post tax implications, especially after the recent tax rate amendments.

Premature Withdrawal Rules For SBI Senior Citizen FDs

- Most SBI fixed deposits allow premature withdrawal, but breaking an FD before maturity usually leads to a lower interest rate and may attract a small penalty.

- Special products such as tax-saving FDs with a 5-year lock-in generally do not permit premature withdrawal except under very limited circumstances.

- Before committing large sums to a long tenure, senior citizens should keep some money in short- or medium-term FDs and maintain a separate emergency fund so that they do not have to break long-term deposits frequently.

Who Are SBI Senior Citizen FDs Suitable For?

SBI senior citizen FDs work best for retirees who:

- Prioritise the safety of capital over high returns.

- Need predictable interest income to cover essential expenses like rent, groceries, or medical bills.

- Prefer dealing with a large, well-known public sector bank with extensive branch and ATM presence.

- Want simple, easy-to-understand products without market-linked volatility.

They may be less suitable as the only investment option for those who:

- Have a long retirement horizon and want higher real returns after inflation.

- Can tolerate some volatility in exchange for better growth through other fixed-income or balanced products.

- Need very flexible liquidity and might have to break FDs frequently, which can reduce effective returns through premature withdrawal penalties.

Inflation Vs FD Returns For Retirees

Simply looking at nominal returns is not enough to measure one's financial security. Inflation gradually diminishes the value of money, so a 7% FD return may not be 7% growth in real terms at all. If inflation hits 5. At 5% on average, the actual return on a 7% FD will be around 1.5%.

This difference is significant for pensioners. Healthcare, household, and lifestyle expenses generally increase faster than inflation. Although SBI senior citizen FD rates are a good option for preserving capital and providing a degree of comfort, they do not necessarily lead to significant wealth creation. When the retirement period stretches to 20 to 30 years, the impact of low real returns can limit financial freedom.

Diversifying Retirement Income

Relying entirely on fixed deposits for retirement income can expose senior citizens to reinvestment risk, particularly during periods of falling interest rates. When FDs mature in low-rate environments, regular income may decline unexpectedly. Diversifying income sources helps address this risk while maintaining a conservative risk profile.

Platforms like Grip Invest enable retirees to complement traditional bank deposits with carefully curated fixed-income products such as high-quality corporate bonds, securitised debt instruments (SDIs), and corporate FDs from reputed issuers. Grip’s bond baskets further simplify diversification by offering theme-based exposure across multiple instruments through a single investment. When combined with bank FDs, these options can help create a more balanced retirement income strategy: one that enhances yield potential, improves cash-flow predictability, and reduces over-dependence on a single asset class.

Conclusion

SBI senior citizen FD rates continue to offer safety, stability, and dependable income, making them a core component of many retirement portfolios. However, long-term financial comfort depends not just on interest rates, but also on tenure selection, taxation, inflation impact, and diversification. While SBI FDs help preserve capital and provide predictable cash flows, combining them with other high-quality fixed-income instruments can improve post-tax returns and reduce reinvestment risk over time.

Grip Invest help retirees go beyond traditional bank deposits by offering access to curated bonds, corporate FDs, and diversified fixed-income baskets, all with clear visibility on yields and maturities—making retirement income planning more balanced and future-ready.

FAQs On SBI Senior Citizen FD Rates 2026

1. Who is eligible for SBI senior citizen fixed deposit rates?

Senior citizen FD rates are available to individuals aged 60 years and above at the time of opening the deposit with State Bank of India. The higher interest rate applies across most regular and special FD schemes.

2. How much extra interest do senior citizens get on SBI FDs?

Senior citizens generally earn about 0.50% per annum more than regular SBI FD rates. On select schemes like SBI WeCare, the additional benefit can be higher, especially for long-term deposits.

3. Is interest earned on SBI senior citizen FDs taxable?

Yes, FD interest is taxable under Income from Other Sources. However, senior citizens can claim a deduction of up to ?50,000 per year under Section 80TTB, which can significantly reduce or even eliminate tax liability for many retirees.

4. Are SBI senior citizen FDs enough to beat inflation?

SBI FDs offer safety and stable income, but after adjusting for inflation, real returns may be modest. Many retirees use SBI FDs for capital protection and combine them with other low-risk fixed-income options to improve overall returns.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001