Types Of Investment In India: A Beginner’s Guide To Building Wealth

For a beginner, the number of investment options can feel confusing. Stocks, bonds, mutual funds, fixed deposits, gold, and government schemes all serve different purposes. Some aim for growth. Some focus on safety. Some help with a regular income.

A sensible choice depends on more than the expected gain. It should fit the investor’s objective, time frame, liquidity needs and tolerance for uncertainty.

This beginner investment guide explains the main types of investment, helping readers compare them with better judgment.

What Is An Investment?

At its simplest, investment means placing money in an asset or financial product with the aim of earning income, capital appreciation, or both.

A fixed deposit can pay interest on INR 1lakh held with a bank. Company shares may deliver gains through price movement and dividends. Gold, by contrast, depends largely on market demand and prevailing rates.

The reason this matters is inflation. As everyday costs rise, the same amount buys less over time. Well-chosen assets can help protect purchasing power, although every route carries some level of risk.

Once you understand why investing matters, the next step is to know the main investment options in India.

Major Types Of Investment

Every investment does not solve the same financial need. Some help preserve capital. Some aim for long-term wealth creation. Some offer liquidity, while others lock your money for years.

Here are the different types of investment beginners should understand.

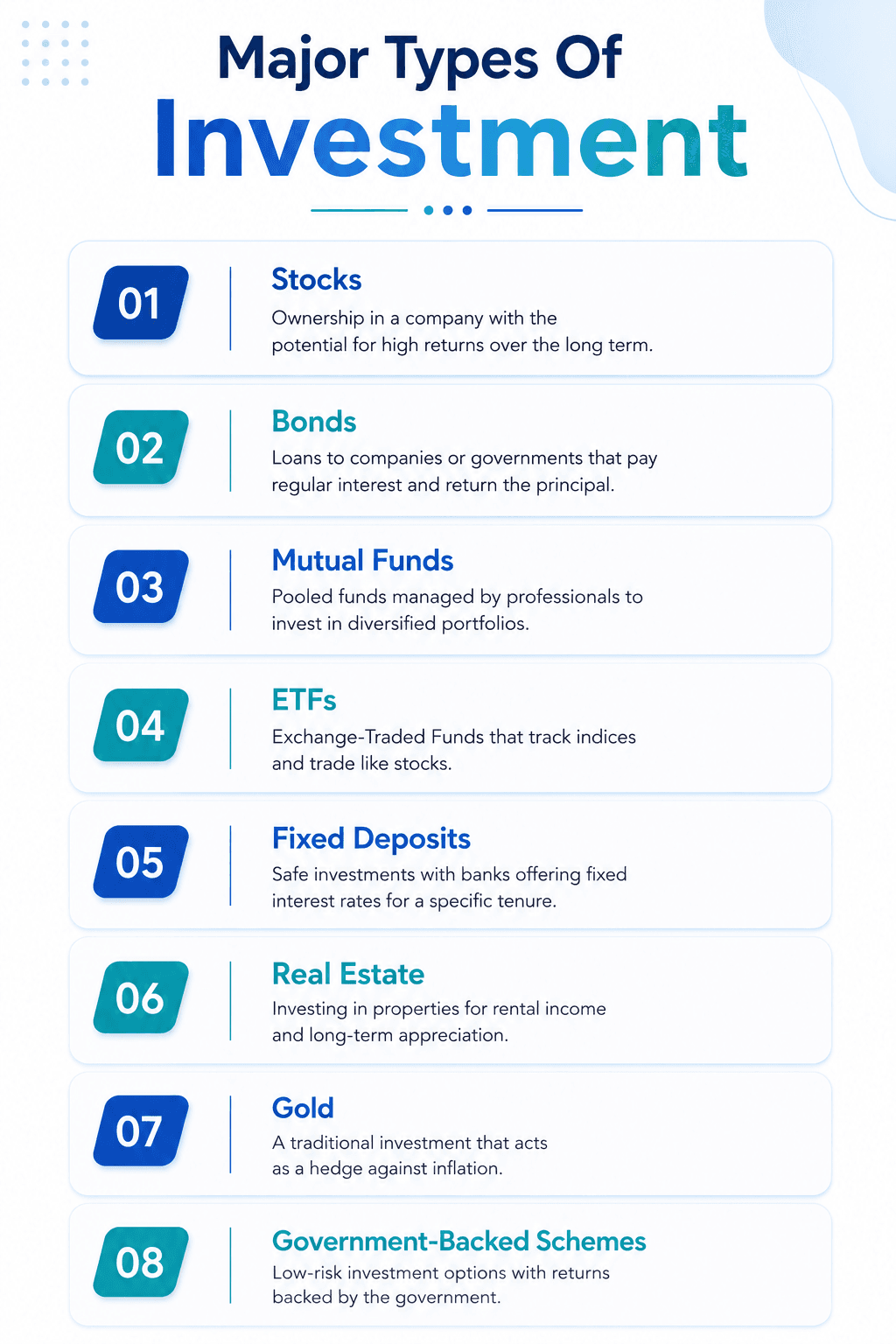

1. Stocks

Listed shares give a person fractional ownership in a business. Their value changes with earnings, sector outlook, investor demand and broader economic conditions.

The upside can appear when sentiment supports the stock. As of 29 May 2026, Paytm had gained about 29.23% over the previous 12 months. An INR 50,000 holding that moved in line with that gain would be worth around INR 64,615 before costs and taxes.1

The drawdown can be equally sharp when expectations weaken. Infosys closed at INR 1,159.75 on the same date, 32.88% below its 52 week high of INR 1728.2 An investor who bought near that peak would have seen INR 50K reduce to about INR 33,560.

Listed shares can support long term wealth creation, but they suit those who can remain patient through volatility.

Factor | What it means |

Return type | Market-linked |

Risk level | High |

Liquidity | Usually high for listed stocks |

Best used for | Wealth creation and growth |

2. Bonds

A bond is a lending instrument. The person investing provides funds, while the borrower may be the Government, a company, or a financial institution.

Scheduled payouts are usually made on fixed dates, and the original amount comes back at maturity. This structure gives clearer income visibility than listed shares, although the outcome still depends on the borrower’s financial position.

The main risks are credit risk and interest rate risk. Credit weakness may delay payment or lead to default. Rate sensitivity can affect the traded value when market yields rise or fall.

For example, in January 2026, Adani Enterprises launched a secured public issue of non-convertible debentures. The five-year option carried an annual coupon of 8.9%. On an INR 1lakh allotment, that rate would translate into INR 8,900 a year before tax, subject to timely payment and issue terms.

Factor | What it means |

Return type | Interest income and possible price movement |

Risk level | Low to medium, depending on issuer |

Liquidity | Varies by bond |

Best used for | Regular income and portfolio stability |

3. Mutual Funds

A mutual fund is a pooled investment vehicle that combines money from several people and places it across shares, bonds, money market instruments, or a mix of holdings. A professional manager runs the portfolio according to the scheme’s stated objective.

This structure suits people who may not want to study individual securities themselves. The risk profile changes across categories. Like, equity-oriented plans usually see wider market swings, while debt funds tend to be steadier, though credit quality and interest rate changes still matter.

For example, a mid-Cap mutual fund category delivered a one year average return of 8.69% as on 28 May 2026. An INR 1,00,000 investment moving in line with that category average would have become about INR 1,08,690 before costs, tax and scheme-level charges.

Selection works best when the chosen category aligns with the investor's goal, holding period, and comfort with uncertainty.

| Mutual fund type | Risk level | Return nature |

| Equity funds | High | Market-linked |

| Debt funds | Low to medium | Interest-rate linked |

| Hybrid funds | Medium | Mix of equity and debt returns |

| Index funds | Medium to high | Tracks a market index |

4. ETFs

Exchange-traded funds are pooled investment vehicles listed on stock exchanges. They can be bought and sold during market hours in the same way as listed shares.

Many such products follow a defined basket, such as the Nifty 50, a sector, a commodity, or a broader asset class. A Nifty 50-linked ETF, for example, aims to reflect the movement of Nifty 50, so its price generally rises or falls in line with the underlying basket.

These instruments usually carry lower expense ratios than many actively managed schemes. A demat account and a trading account are required to invest in them.

Factor | What it means |

Return type | Market-linked |

Risk level | Depends on the underlying asset |

Liquidity | Depends on trading volume |

Best used for | Low-cost diversified exposure |

5. Fixed Deposits

A fixed deposit lets a person place a lump sum with a lender for a chosen tenure. The agreed payout is known at the time of booking.

Its main strength is predictability. This makes it easier to plan near term goals or preserve capital. The trade-off is that inflation and taxation can reduce the real value of the income received.

For example, INR 1 lakh placed at 7% per annum for one year would generate INR 7000 before tax. The final amount may differ based on the depositor’s slab and withdrawal terms.

Factor | What it means |

Return type | Fixed interest |

Risk level | Low for scheduled bank FDs |

Liquidity | Medium, with possible premature withdrawal penalty |

Best used for | Capital safety and predictable returns |

6. Real Estate

Real estate includes residential property, commercial property, land, and real estate investment products. Returns may come from rental income, price appreciation, or both.

A residential unit bought for INR 50 lakh, for instance, may provide a monthly rental cash flow. Its worth can also rise when the neighbourhood develops, infrastructure improves, and buyer interest strengthens.

This route can help with long-term asset creation, but it usually needs substantial upfront capital. Exit can also take time, as selling a physical asset is often slower than liquidating listed instruments.

Factor | What it means |

Return type | Rent and price appreciation |

Risk level | Medium to high |

Liquidity | Low |

Best used for | Asset ownership and rental income |

7. Gold

Precious metals like gold are often used to reduce dependence on a single asset class. They may become relevant during inflationary periods, currency weakness, or broader financial stress. Exposure can come through jewellery, coins, bars, ETFs, mutual funds, or regulated linked instruments.

Unlike income bearing avenues, this asset does not provide interest or rent. Gains mainly depend on bullion rates, exchange rate changes and domestic buying trends.

The recent five-year trend shows the scale of appreciation. The 24 karat rate in India stood at INR 48,406 per 10 grams on 28 May 2021 and reached INR 156,231 per 10 grams on 29 May 2026.

This marks a rise of INR 107,825 for every 10 grams before GST, making costs, storage expenses, or product-level fees.

Factor | What it means |

Return type | Market-linked price movement |

Risk level | Medium |

Liquidity | High for ETFs, medium for physical gold |

Best used for | Diversification and inflation protection |

8. Government-Backed Schemes

Sovereign-backed savings instruments provide a formal route to preserve capital and earn declared interest.

These instruments generally appeal to people who value stability over market-dependent gains. Each option still needs careful review, as lock in periods, eligibility rules, and premature exit limits can affect access to funds.

Scheme | Return rate (% per annum) (April to June 2026) | Key use |

Public Provident Fund | 7.10% | Long-term tax-efficient savings |

National Savings Certificate | 7.70% | Fixed return savings |

Senior Citizens Savings Scheme | 8.20% | Income for senior citizens |

Sukanya Samriddhi Yojana | 8.20% | Savings for a girl child |

Post Office Time Deposit | 6.9% - 7.5% | Fixed income savings |

Types Of Investment Based On Risk

Uncertainty can show up in different forms while investing. The holding may lose worth, income may fluctuate, or funds may not be available when they are needed.

Classifying wealth creation investments by risk profile gives readers a clearer frame for evaluation. It also helps them avoid choosing a product only because the expected gain looks attractive.

- Low-Risk Investments

Safe investment plans usually focus on capital safety and stable returns. Examples include fixed deposits, government-backed schemes, savings accounts, and short-term government securities.

These options may work for emergency reserves, near-term needs, and people who prefer lower volatility. They provide better visibility, though the earning potential usually remains modest compared with market-linked assets.

- Medium-Risk Investments

Balanced investments aim to improve earning prospects while keeping some protection against sharp market swings. Common examples include hybrid funds, precious metals, highly rated corporate bonds, and select debt-oriented schemes.

These choices may suit people seeking more than traditional savings products, without relying entirely on listed equities.

Review the details before investing. The label alone may not show the credit profile, asset mix, exit terms, liquidity limits, or possible fluctuations.

- High-Risk Investments

Aggressive investments can deliver stronger gains, but they also expose investors to sharper declines. Common examples include listed shares, equity mutual funds, sector focused schemes, small-cap portfolios, and thematic strategies.

These choices may fit long term objectives where short-term volatility is manageable. They require discipline and are usually unsuitable for funds needed within the next few years.

Types Of Investment Based On Time Horizon

The holding period shows how long a person can keep capital aside before using it. This matters because the same product may support one purpose and create avoidable strain in another.

An equity fund, for instance, may be considered for retirement planning. The same route may not work for school fees due next year, where access and stability become more important.

1. Short-Term Investments

For needs due within 3 years, the focus should remain on easy access and capital protection. Suitable avenues may include savings accounts, fixed deposits, liquid funds, short-duration debt funds, and treasury bills.

Capital required soon should not chase aggressive market returns. Preservation usually carries more weight than appreciation in this phase

2. Medium-Term Investments

For a 3 to 5 year window, people may look for a measured balance between steadiness and moderate gains. Possible choices include bank deposits, debt-oriented schemes, hybrid funds, gold, and selected sovereign-backed products, depending on lock-in rules.

Planning becomes important as the target date approaches. The allocation may need easier exit options and lower fluctuations near withdrawal.

3. Long-Term Investment Options

When the objective is more than 5 years away, growth-oriented assets may have a larger role. These can include equity mutual funds, listed shares, index funds, and PPF.

A longer runway can help absorb short-term market swings, although it does not remove uncertainty. Consistent allocation and limited switching can support compounding over time.

How To Choose The Right Investment Type?

The selection process should begin with intent. A person should first decide whether the capital is meant for income, expansion, emergency use, or a planned expense.

Each requirement points to a different route. Once the intended role is clear, comparing suitable choices becomes easier.

Near-term priorities usually need stable financial investment types with easier withdrawal. Distant targets may allow greater exposure to growth-oriented assets.

Age

Life stage affects earning years, family responsibilities, and the ability to absorb losses. A younger person may have more time to recover from market declines.

Someone closer to retirement may prefer steadier cash flow and lower fluctuations. Still, age alone should not decide the allocation, as income, dependents, liabilities, and future expenses also matter.

Risk Tolerance

Comfort with uncertainty shows how much variation a person can handle without making rushed decisions. This matters because market-linked instruments rarely move in a straight line.

A 10% fall may feel manageable to one person and stressful to another. The chosen portfolio should reflect this behavioural comfort, not only the expected gain.

Liquidity Needs

Ready access becomes important when funds may be required at short notice. Emergency reserves should stay in liquid investments.

Longer term pools can accept some lock-in or lower exit flexibility. Real estate may appreciate over time, but a quick sale can be difficult.

Expected Returns

Greater earning potential usually comes with wider uncertainty. Fixed return products provide visibility, although their upside may remain limited.

Market-linked instruments may support wealth creation over time, but they do not provide assured outcomes. A balanced mix is often more practical than pursuing the highest possible gain.

The suitable choice should match the role assigned to the capital.

Building A Balanced Investment Portfolio

A balanced portfolio does not depend on one investment type. It combines different wealth creation investments so that one weakness does not affect the entire plan.

For example, equity can support long-term growth. Fixed-income products can add stability. Gold can offer diversification. Liquid assets can help during emergencies.

This mix is called asset allocation. It helps investors manage risk without giving up every growth opportunity.

Portfolio role | Asset examples | Purpose |

Growth | Stocks, equity funds, index funds | Long-term wealth creation |

Stability | FDs, bonds, debt funds, government schemes | Lower volatility |

Liquidity | Savings account, liquid funds, short-term FD | Emergency access |

Diversification | Gold, hybrid funds, real estate | Reduce dependence on one asset |

Diversification does not remove risk. It spreads risk across different investments.

A beginner can start by separating money into three buckets: near-term money, medium-term money, and long-term money. Each bucket can then hold suitable investment types.

There is no single best investment for every person. Each option has a role.

Conclusion

Understanding the different types of investment is the first step towards making informed financial decisions. Each investment option serves a different purpose. Stocks and equity funds can help with long-term growth, while bonds, fixed deposits, and government-backed schemes may offer greater stability and predictable income. Gold and real estate can add diversification, helping reduce dependence on a single asset class.

Rather than searching for the "best" investment, focus on choosing options that align with your financial goals, time horizon, liquidity needs, and comfort with risk. A well-balanced portfolio that combines different asset types is often more effective than relying on any one investment alone.

If you're looking to diversify beyond traditional investment options, Grip Invest offers curated fixed-income opportunities such as corporate bonds and other investment products designed to help investors earn predictable returns while building a balanced portfolio.

FAQs On Types Of Investments

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001