5 Year Tax-Saving FD: Benefits, Section 80C Tax Savings And Should You Invest?

Want to lower your tax burden without exposing yourself to market risk? You should check out the 5-year tax-saving FD. This financial tool offers a combination of the benefits of fixed returns and taxation, which is why it has become quite popular amongst conservative investors and first-time taxpayers.

The 5-year tax-saving FD refers to a fixed deposit scheme of banks, which attracts a deduction of up to INR 1.5 lakh in accordance with Section 80C of the Income Tax Act, but only if you choose the old tax regime. With a mandatory lock-in period of five years, you will not be able to withdraw your funds before the end of that term.

This tax-saving FD can be invested in by any resident individual or Hindu Undivided Family (HUF). However, does it suit your requirements?

Here, we'll explore the features of the 5-year tax savings FD and its advantages over other Section 80C investment schemes.

Who Can Invest In A 5-Year Tax-Saving FD?

A 5-year tax-saving FD is available only to eligible resident individuals and Hindu Undivided Families (HUFs). It is not available to companies, partnership firms, or non-resident Indians (NRIs), although eligibility may vary depending on the bank's policies and applicable regulations.

Before investing, remember that:

- The deduction under Section 80C is available only under the old tax regime.

- The deposit must remain invested for a mandatory lock-in period of five years.

- Premature withdrawals are generally not permitted during the lock-in period.

Understanding these conditions can help you determine whether a tax-saving FD aligns with both your tax planning and liquidity needs.

How It Compares With Other Section 80C Investments?

The 5-year tax-saving FD is just one investment that falls within Section 80C and provides tax savings. This form of investment guarantees returns, but there are other investments that provide higher growth, increased liquidity, or more tax benefits. These aspects have been explained below to help you understand what works best for you as an investor.

1. Public Provident Fund (PPF)

Public Provident Fund is a savings scheme by the government, and the period is fixed at 15 years. PPF provides tax-free interest along with tax-free maturity value and can be used for wealth creation through investments. However, since the lock-in period is longer, investors looking for liquidity may find it difficult.

2. Equity-Linked Savings Scheme (ELSS)

The Equity-Linked Savings Scheme (ELSS) is another popular tax-saving option, which is a mutual fund investing mostly in equities. ELSS has the shortest lock-in period among major Section 80C options, which is three years. This scheme provides potential for high returns along with increased risks.

3. National Savings Certificate (NSC)

Another government-guaranteed investment, NSC, has a tenure of five years. It is a good investment instrument due to its assured returns and the low risk involved. Unlike a 5 Year Tax-Saving FD, it is a compounding plan and is eligible under Section 80C till maturity, but not in the last year.

4. Employees Provident Fund (EPF)

It is a retirement savings plan for salaried individuals. Both the deposits and interest are exempt from taxes based on existing laws. The EPF is perfect for creating your retirement corpus, but cannot be opted for by all investors.

5. Sukanya Samriddhi Yojana (SSY)

SSY is a financial plan for a girl child. The SSY has good returns guaranteed by the government, with good taxation benefits. But only parents or legal guardians of an eligible girl child can avail of the same.

| Investment | Lock-in | Risk | Liquidity | Return Potential | Tax Treatment |

| 5 Year Tax-Saving FD | 5 years | Low | Low | Fixed | Investment eligible under Section 80C; interest taxable |

| PPF | 15 years | Very Low | Partial withdrawals after specified years | Moderate | Exempt-Exempt-Exempt (EEE) |

| ELSS | 3 years | High | Moderate after lock-in | High (market-linked) | Investment eligible under Section 80C; LTCG tax applicable beyond limits |

| NSC | 5 years | Low | Low | Fixed | Investment eligible under Section 80C; interest taxable, with reinvestment benefits until maturity |

| EPF | Until retirement (with certain withdrawal provisions) | Very Low | Limited | Moderate | Tax benefits are subject to the prevailing rules |

| Sukanya Samriddhi Yojana | Up to maturity or eligible withdrawal | Very Low | Limited | Moderate to High | Exempt-Exempt-Exempt (EEE) |

What Should You Check Before Investing In A 5-Year Tax-Saving FD?

Although tax-saving FDs are relatively straightforward, comparing a few factors before investing can help you choose the most suitable option.

| Factor | Why It Matters |

| Interest rate | A higher rate can improve your overall returns over five years. |

| Interest payout option | Choose cumulative or non-cumulative based on whether you need periodic income or compounded returns. |

| Taxation of interest | Interest earned is taxable according to the applicable tax rules, even though the investment qualifies for a Section 80C deduction. |

| Lock-in period | Premature withdrawal is generally not allowed before five years. |

| Deposit insurance | Check the applicable deposit insurance coverage offered under prevailing regulations. |

| Bank credibility | Consider the financial strength, customer service, and overall reliability of the bank. |

Comparing these factors alongside tax benefits can help investors make a more informed decision rather than choosing a tax-saving FD solely based on the advertised interest rate.

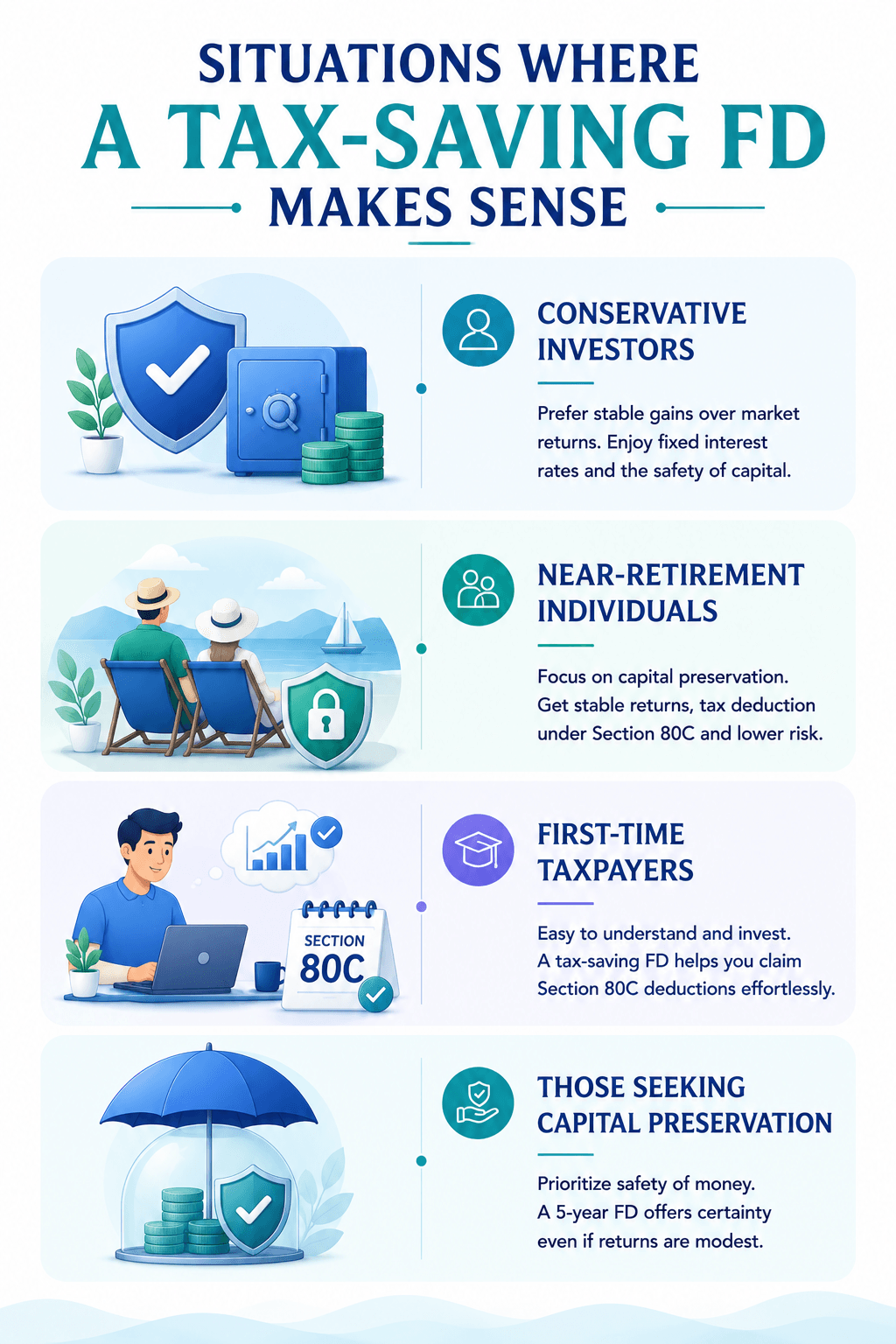

Situations Where A Tax-Saving FD Makes Sense

Not every investor will find a 5-year tax-saving FD an excellent option. There are instances when the investment tool proves to be very beneficial for certain types of investors.

1. Conservative investors

Investors who would rather stick with stable gains than market-based returns can choose a tax-saving FD. In comparison with equity-related schemes like ELSS, it guarantees fixed rates of interest and safekeeping of the investment.

2. Near-retirement individuals

With a near-retirement age, capital preservation becomes much more important than profit-making. A tax-saving FD scheme provides stable returns on investment, a tax deduction under Section 80C FD, and relatively low risks.

3. First-time taxpayers

In case you recently became employed and are looking for ways to invest money, an FD becomes a perfect solution. With no special requirements related to financial education, a tax-saving FD can provide you with the possibility to benefit from Section 80C deductions.

4. Those seeking capital preservation

When you are primarily interested in keeping the invested amount safe, a 5-year fixed deposit becomes an appropriate choice for you. Despite the fact that it might not bring higher interest rates compared to inflation rates, its certainty appeals to many investors.

Situations Where Another 80C Investment May Be Better

Although the 5-year tax-saving FD has its own pros, in certain scenarios, other forms of Section 80C investment might be a better choice.

- Long investment horizon: For those who are planning to invest for long-term financial goals that are 10 to 20 years in the future, investments that include PPF or EPF would be the better option.

- Inflation-beating goals: When it comes to creating wealth in the long run, the investor should go for ELSS. Though the return cannot be guaranteed by the ELSS scheme, it can provide returns that beat the rate of inflation, as historically, equity returns have outdone the inflation rate.

- Need for liquidity: If liquidity is required in the near future from the savings account of an investor, he can choose a form of investment which allows premature withdrawal, such as PPF after a certain period.

- Higher risk tolerance: When an investor wants to take on risk to earn higher returns in the market, ELSS is a good choice, as it combines tax savings with long-term capital appreciation.

Decision Framework Which Section 80C Investment Matches Your Goal?

If Your Goal Is… | Consider |

Guaranteed returns with low risk | 5 Year Tax-Saving FD |

Long-term retirement savings | PPF or EPF |

Higher long-term wealth creation | ELSS |

Saving for a girl child's future | Sukanya Samriddhi Yojana |

Stable returns with government backing | NSC |

How Inflation Can Affect Tax-Saving FD Returns?

A tax-saving FD provides fixed returns, but investors should also consider the impact of inflation over the five-year investment period.

If inflation remains higher than the post-tax return generated by the deposit, the purchasing power of the investment may decline over time. While tax-saving FDs can help preserve capital and provide predictable returns, investors pursuing long-term wealth creation may also consider diversifying across other suitable asset classes based on their risk tolerance and financial goals.

Common Mistakes To Avoid When Investing in a Tax-Saving FD

While a tax-saving FD is considered a relatively simple investment, a few common mistakes can reduce its effectiveness as part of your financial plan.

- Investing only for tax savings: Saving tax should complement your financial goals rather than drive your entire investment decision.

- Ignoring the taxability of interest: Although the investment qualifies for a deduction under Section 80C, the interest earned is generally taxable.

- Overlooking inflation: Fixed returns may not always keep pace with inflation over longer periods.

- Locking in funds without assessing liquidity needs: Since premature withdrawals are generally not permitted, investors should avoid using money that may be needed during the five-year tenure.

- Ignoring portfolio diversification: Relying entirely on tax-saving FDs may limit long-term wealth creation if other suitable asset classes are overlooked.

Tax Saving Is Only One Part Of Financial Planning

It becomes necessary for an investor to reduce his or her tax liability, but this must not be the sole consideration while making investments. The right investment option must also match one’s financial requirements, risk tolerance levels, need for liquidity, and investment period.

For instance, while a 5-year tax-saving FD may guarantee high returns along with Section 80C deductions, it may not offer the growth or flexibility required by certain investors. Portfolio creation often involves not only investing in tax-saving plans but also creating investments for wealth generation and income.

Once your 80C limit has been exhausted, you can diversify your portfolio with fixed income securities. Corporate Bonds, Corporate FDs, and other fixed income investments can generate regular income while also providing diversification in terms of issuing companies and maturities.

Grip Invest offers such fixed-income investments, which can help you create a diversified portfolio by investing in various investments other than bank FDs.

Conclusion

A 5-year tax-saving FD might suit you well, especially if you seek capital protection, guaranteed returns, and Section 80C benefits. However, which investment works also depends on how aligned it is with your financial goals, risk tolerance, and requirement for liquidity. Therefore, you should thoroughly analyse the relevance of different Section 80C options before investing and make sure they contribute to the achievement of your financial goals rather than just offer tax savings.

After reaching the limit of your Section 80C scheme, diversify the rest of your investments with other fixed-income options such as corporate fixed deposits and corporate bonds to maximise your income while maintaining balanced risk exposure.

If you are interested in broadening your scope beyond regular tax-saving investment opportunities, do not hesitate to look through the selection of fixed-income investment options available on Grip Invest.

FAQs On 5 Year Tax-Saving FD

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001