Bullet Repayment Bonds In 2026: Meaning, Features, Benefits And Risks Explained

A bullet repayment bond is a type of debt security that pays periodic interest but repays the principal amount only upon the maturity of the bond.

Throughout the lifespan of the bond, say 5 years or 30 years, the issuer pays fixed or variable interest to the bondholder. The interest payment dates are preset.

On the day of maturity, the issuer pays back the entire principal bond amount as a lump sum, which brings the term “bullet repayment” into effect. This concludes the obligations of the bond.

Issuers like corporations or the government use bullet repayment bonds as they do not have to worry about the periodic principal payments during the life of the bond. This allows them to utilise the capital free for their operations.

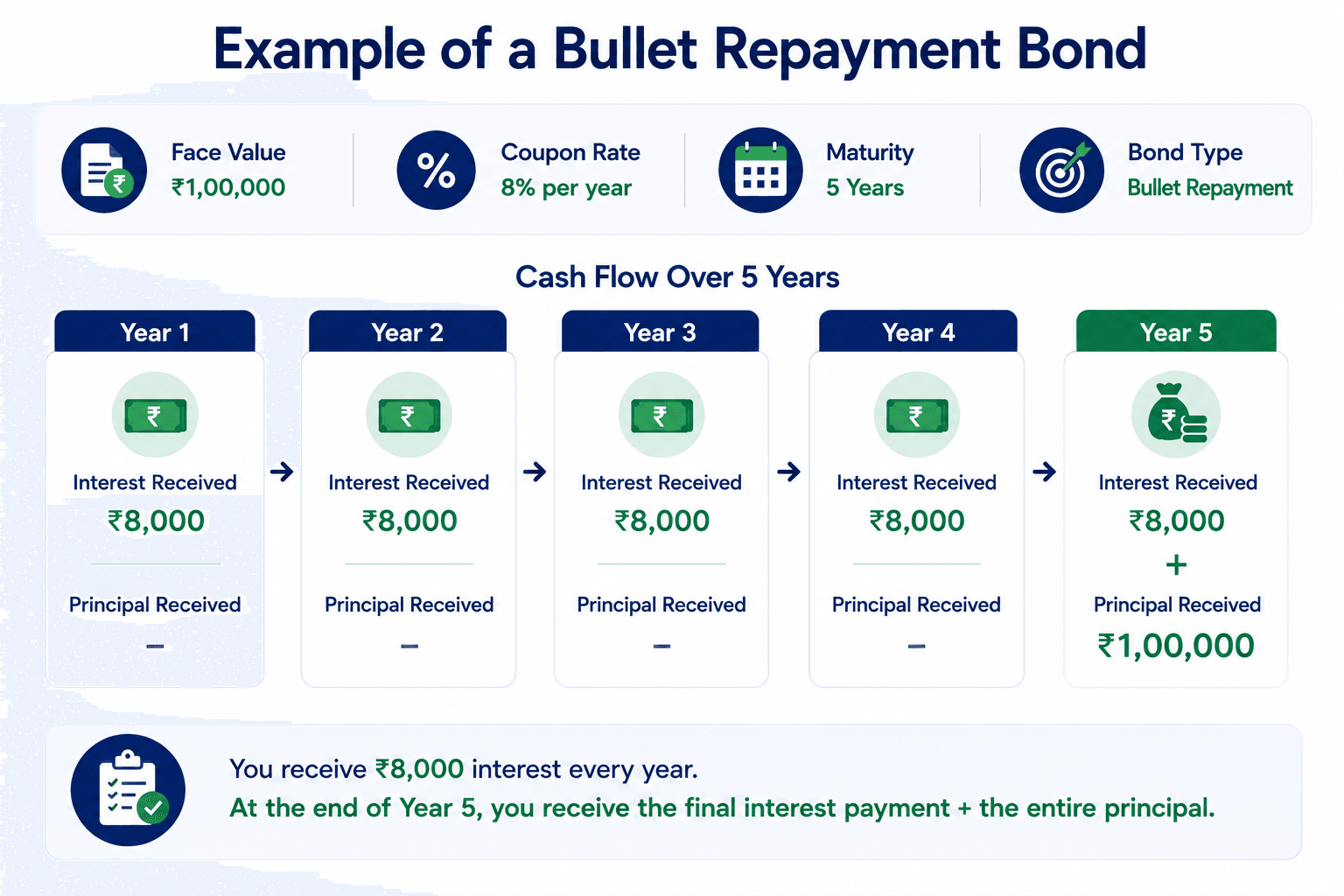

Suppose an investor purchases a bullet repayment bond with a face value of INR 1,00,000, a coupon rate of 8% per year, and a maturity period of five years.

The investor receives annual interest payments of INR 8,000 throughout the tenure. However, unlike an amortising bond, the principal remains outstanding until the maturity date. At the end of the fifth year, the investor receives both the final interest payment and the entire principal amount.

| Year | Coupon Received | Principal Received |

| 1 | INR 8,000 | — |

| 2 | INR 8,000 | — |

| 3 | INR 8,000 | — |

| 4 | INR 8,000 | — |

| 5 | INR 8,000 | INR 1,00,000 |

Unlike amortising bonds, the principal remains outstanding until maturity.

How Bullet Repayment Differs From Other Bond Structures?

This is how bullet repayment bonds differ from other bond structures:

- Bullet repayment: As discussed above, a bullet bond pays regular interest during its life, but the principal is repaid only once on the bond maturity date. This means the issuer can use the amount until it matures, which is why people like to invest in these fixed-income investment options.

- Amortising bonds: These bonds pay both interest and part of the principal at regular intervals throughout the bond period. This approach reduces the repayable amount at bond maturity.

- Callable bonds: These bonds provide a right to the issuer to repay the principal before the maturity date, but not an obligation. Compared to this, bullet bonds are usually non-callable.

- Sinking fund bonds: These bonds require the issuer to keep some money aside or repay part of the principal before maturity. Similar to amortising bonds, these bonds reduce the principal repayment amount before maturity.

Here is a comparison table of bullet bonds vs amortising bonds:

Features | Bullet Bonds | Amortising Bonds |

| Principal Repayment | Paid entirely as a single lump sum at maturity. | Repaid over the bond life through periodic payments. |

| Periodic Payments | Periodic payments only cover the interest. | The payments include interest and a part of the principal. |

| Cash Flow Profile | Predictable interest payments with a large cash outflow/inflow at the very end. | The cash flow changes as the principal balance decreases. |

| Refinancing / Issuer Risk | The issuer must either have sufficient cash reserves or be able to refinance the massive principal amount at maturity. | The principal is already paid off by the time the bond matures. This eliminates the “balloon payment” or refinancing risks. |

| Investor/Credit Risk | Higher credit risk over the life of the bond since the entire principal is held until the very end. | Lower credit risk as the principal is continuously paid back over time. |

| Reinvestment Risk | Lower reinvestment risk, as there is no large principal to reinvest before maturity. | Higher reinvestment risk, since investors receive regular principal payments that they must reinvest. |

What Should Investors Check Before Investing In A Bullet Repayment Bond?

| Factor | Why It Matters |

| Credit rating | Indicates issuer's repayment capability |

| Yield to Maturity (YTM) | Shows expected annual return if held to maturity |

| Coupon rate | Determines periodic interest income |

| Maturity date | Should align with your investment goals |

| Liquidity | Check whether the bond can be sold before maturity |

| Security | Secured vs unsecured bond |

| Interest payment frequency | Monthly, quarterly, semi-annual or annual |

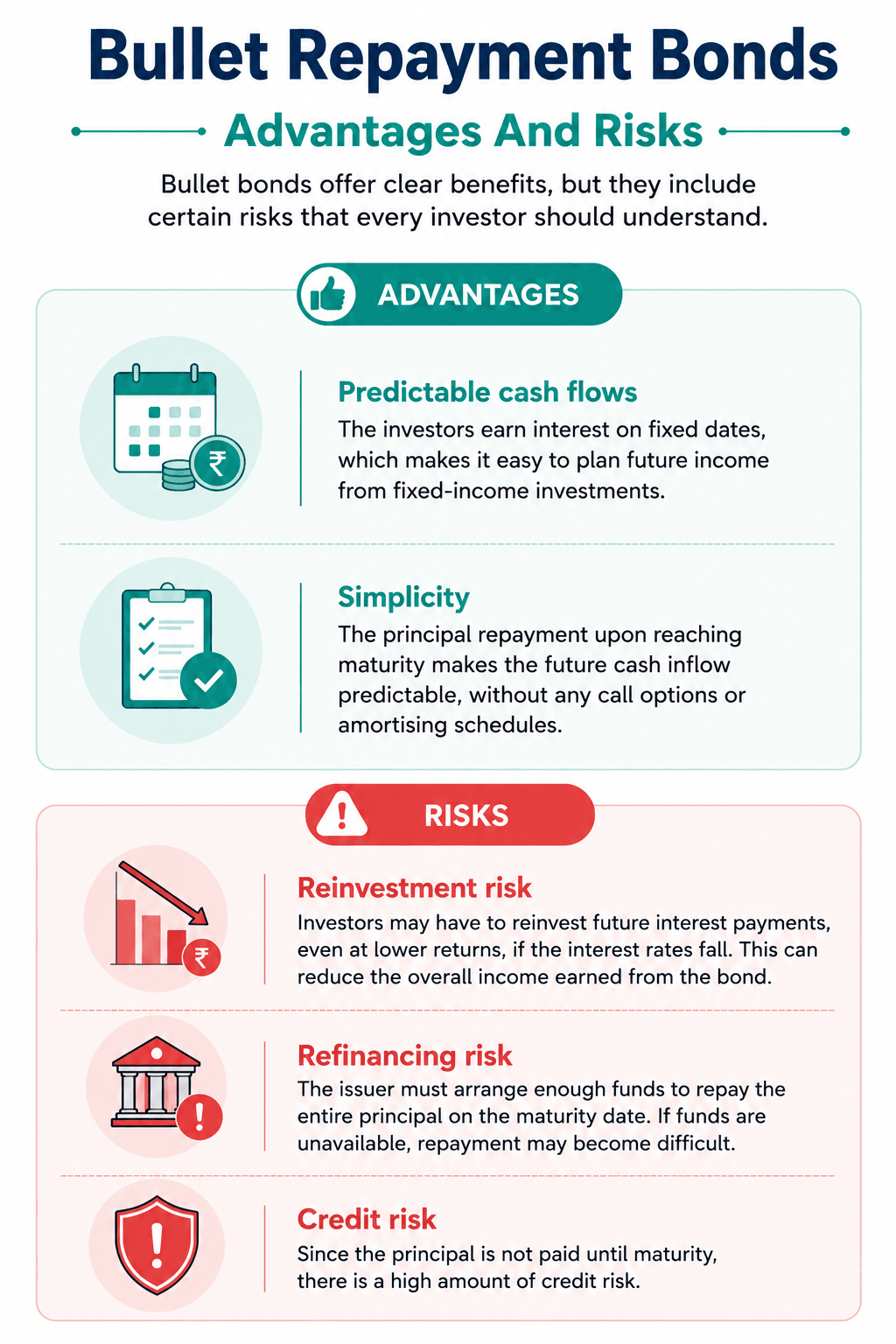

Advantages And Risks Of Bullet Repayment Bonds

Bullet repayment bonds offer clear benefits, but they include certain risks that should be understood by the investors. Let us discuss them briefly!

Advantages

- Predictable income: Fixed coupon payments can help investors plan regular cash flows.

- Simple repayment structure: The principal is repaid in one lump sum at maturity, making the repayment schedule easy to understand.

- Lower principal reinvestment risk: Since the principal is returned only at maturity, investors do not need to reinvest partial principal repayments during the bond's tenure.

- Suitable for goal-based investing: Investors with a known future financial goal may align the bond's maturity with that objective.

Risks

- Credit risk: If the issuer faces financial difficulties, coupon or principal repayments may be delayed or defaulted.

- Interest rate risk: Rising market interest rates can reduce the bond's market value before maturity.

- Liquidity risk: Some bullet repayment bonds may have limited trading activity, making it difficult to sell them quickly in the secondary market.

- Refinancing risk: Issuers must arrange sufficient funds to repay the full principal amount on the maturity date.

Taxation Of Bullet Repayment Bonds

The tax treatment of a bullet repayment bond depends on how the investor earns returns from the investment.

- Coupon income: Interest received from the bond is generally taxed according to the investor's applicable income tax provisions.

- Sale before maturity: If the bond is sold in the secondary market before maturity, any capital gain or loss may be taxed based on the applicable tax rules.

- Principal repayment at maturity: The repayment of the bond's face value itself is generally not taxable, although the overall tax treatment may depend on the purchase price and prevailing tax regulations.

Since tax rules may change over time and vary based on individual circumstances, investors should refer to the latest tax provisions or consult a qualified tax professional before investing.

When Are Bullet Repayment Bonds Suitable?

These bonds can be suitable for those with particular goals and investment timelines.

- Investor profiles: A bullet bond can be suitable for individuals who prefer to receive regular income and a redemption at maturity. In most cases, insurance companies, pension funds and mutual funds invest in these bonds.

- Investment horizon: These bonds are more suited when your investment horizon and bond maturity period match. Additionally, bullet bonds can be less suitable for those who want liquidity because you must hold the bond till maturity.

- Interest rate expectations: Bullet bonds can perform quite well when the interest rates are at a peak or are expected to drop. Locking in a fixed coupon allows investors to continue earning the same interest even if market rates decline later. However, in the case of rising rates, bullet bonds can face a higher risk of interest-rate.

Checklist Before Investing In A Bullet Repayment Bond

Before investing, consider verifying the following:

- Credit rating of the issuer

- Coupon rate and payment frequency

- Yield to Maturity (YTM)

- Maturity date and investment horizon

- Whether the bond is secured or unsecured

- Secondary market liquidity

- Credit outlook and financial position of the issuer

- Offer document and key risk disclosures

Reviewing these factors can help investors assess whether the bond aligns with their return expectations, liquidity needs, and risk tolerance.

Exploring Fixed-Income Opportunities

Bullet repayment bonds can play a useful role in a diversified fixed-income portfolio when their repayment structure aligns with an investor's financial goals. However, investment decisions should not be based solely on the coupon rate. Evaluating the issuer's credit quality, liquidity, maturity profile, and overall portfolio allocation can help investors make more informed decisions.

If you are looking to diversify your fixed-income investments, you can consider options such as corporate bonds, SDIs, lease-based investments, and other income-generating opportunities on Grip.

These can offer regular payouts and help in spreading risk across different asset classes. Visit Grip Invest today for more information!

FAQs On Bullet Repayment Bonds In 2026

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001