Reinvestment Risk Explained: What It Means and How Investors Can Manage It

Many investors concentrate on the fluctuations of the markets yet neglect to consider how to manage the cash they receive after their money is returned. When a bond or deposit pays interest, that money must then be reinvested into an appropriate investment.

If there is less available to invest in the future than there was in the past, then the wealth created through reinvesting may not be as much as originally anticipated. Understanding reinvestment risk will help investors to create portfolios that align more closely with their long-term income requirements.

The media focuses on the volatility of prices, while the news reports do not give sufficient attention to the more gradual changes that occur regarding the investment landscape and to how much better or worse the future investment prospects could be.

Fixed-income investors often believe that today's rates will remain constant for the next several years.

What Is Reinvestment Risk?

There is a risk of reinvesting cash flows at lower returns. Bonds, fixed-interest securities, and certificates of deposits (CDs) provide a variety of cash flow options to investors, including interest payments, coupon payments (a regular payment of interest), and maturing principal amounts (the total amount invested in a CD/Fixed Income security).

As interest rates fall, safer investment options yield much less income than previously offered to investors. Reinvestment is an easy way to understand this risk because it is a risk associated with an earlier purchase at a higher interest rate, and time passing has created a different interest rate landscape.

Think of a bond that was purchased at an attractive interest rate during a period with higher interest rates. By the time this bond matures (or reaches its full value), the current interest rate environment has significantly declined.

In other words, if the investor had intended to purchase similar bonds after their bond matured, it would be much more difficult to find a similar investment with the expected level of income.

The difference between what the initial expected return and what the actual return on the investment will be at the time of maturity demonstrates the reinvestment risk factor in action.

Where Reinvestment Risk Shows Up Most

Investors face reinvestment risk if their investment pays them periodically or if their investment matures on a set schedule. This risk is of particular concern for people who rely on steady income from interest payments that help them pay bills and meet financial goals.

For this reason, understanding the concept of reinvestment risk is essential for those individuals who depend on having a steady source of income from interest. Take a look where it shows up the most:

- As mentioned previously, investors face opportunities to reinvest every time they receive an interest payment from an investment.

- A product that pays out more frequently exposes an investor to more opportunities to make reinvestment choices.

- The investments that subscribe to this philosophy typically have relatively shorter maturities which subject them to more frequent reinvestment decisions.

Bonds and Fixed Income Instruments

Many bonds enable investors to receive periodic coupon payments as a means of generating reinvestment risk. The moment an investor receives a coupon payment, they must come up with a new place to deposit that money.

Fixed deposits, non-convertible debentures (NCDs) and most debt mutual funds, are also subject to the same fixed income risks. When fixed income investments mature and the investor redeems the proceeds of that investment, the investor will likely want to invest those proceeds into another investment in order to maintain a steady income level.

If interest rates drop and the new investment is paying a lower yield than the original investment, then the investor's total income level will decline.Therefore, they may not be able to achieve their financial goals.

1. Falling Interest Rate Environments

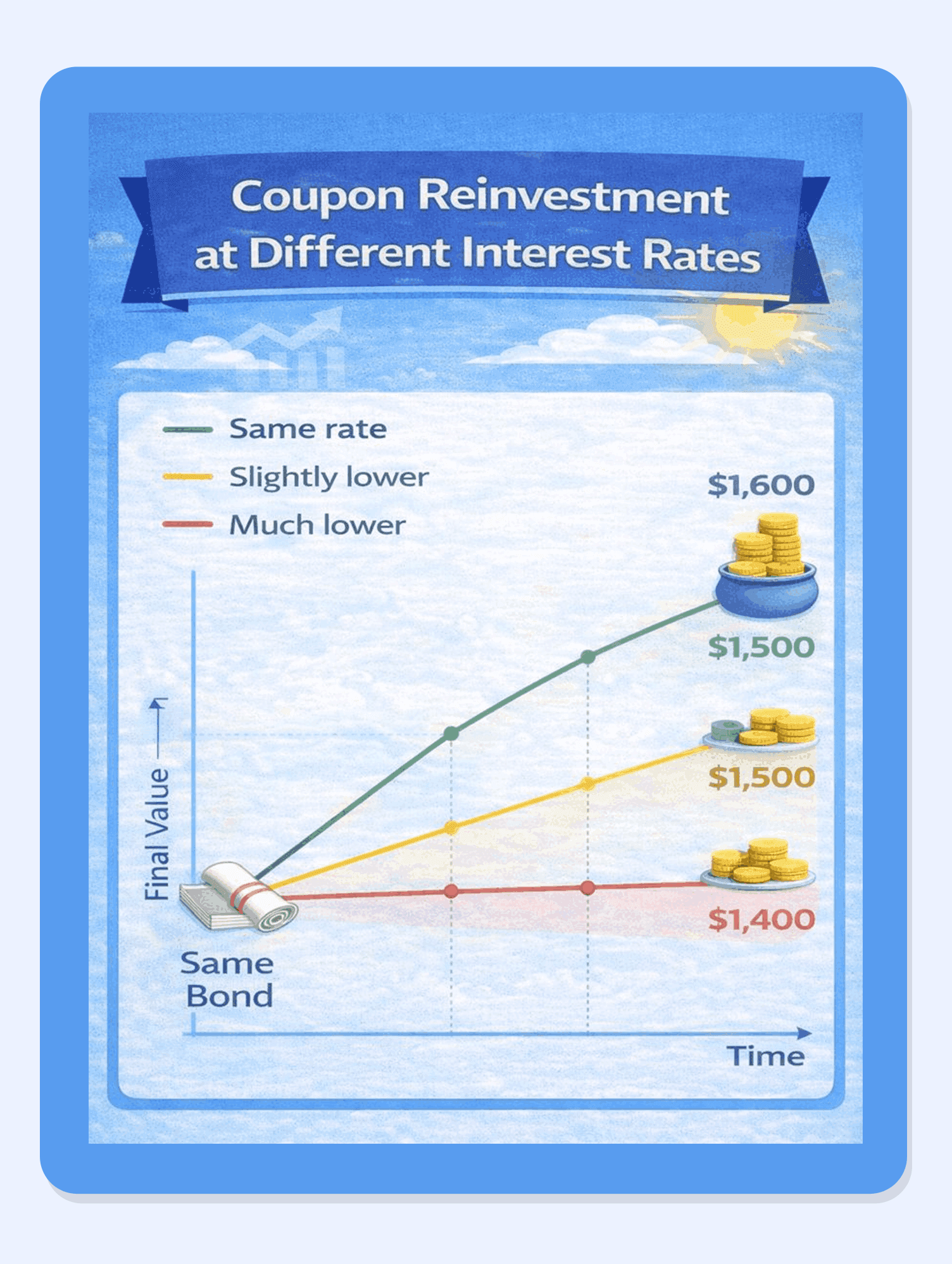

The risk of reinvesting money into bonds has become clearer as interest rates have continued to drop across the economy. The attractiveness of older bonds with a higher yield (or coupon rate) is diminished when those existing cash flows are not producing similar comparable cash flows upon maturity.

The majority of these investors with a significant number of short- and medium-term investment vehicles will see cash returned at lower interest rates through the period of lower interest. Each time cash is returned and reinvested, the investor will find that the current reinvestment opportunities will be less attractive than the original investments.

After years of continuously receiving cash back to reinvest, this slow erosion of income can add up to a significant dollar amount of otherwise safe fixed income investments.

Why Reinvestment Risk Can Hurt Returns

Reinvestment risk will ultimately affect investors because it alters the projected total returns of investments as calculated in the past. Most fixed income calculators include automatic assumptions that coupons and maturities will be reinvested at the original yields on the investments.

If current fixed interest rate yields decrease significantly compared to the investment calculations, then the actual returns will be below what was projected. This is why it is important to understand the background and impact of reinvestment risk so that investors can treat projected returns as estimates versus providing guaranteed returns over money invested.

With that knowledge, investors can plan with more realistic income projections into long term financial commitments (i.e., pensions, retirement accounts, insurance policies, annuities) rather than assuming that all assets will generate results as projected.

1. Lower Future Income

Income-focused bond investors experience monthly cash inflow declines due to reinvestment risk. For example, if a retiree relied on the interest from their maturing fixed income securities as part of their regular budget, any loss in new investments will result in less total interest being produced by the same invested capital.

The retiree will then have to either reduce their expenses or potentially increase their risk profile to replace that lost cash inflow. Therefore, both options create uncertainty, which necessitates understanding of fixed income investment risks as soon as possible.

The reliance on short-term products provides an investor with greater opportunity for income risk exposure. In a long-term investment strategy, an investor needs to pay special attention to reinvesting conditions over multiple time frames to determine if his or her return expectation is within that time frame.

2. Mismatch With Long Term Goals

Reinvestment risk can disrupt the investor's long-term goal to raise investing into education funds or purchasing homes. The expectation that a relatively low risk investment will produce a long-term rate of return means that an investor expects to be able to invest at a particular rate of return for an extended time.

If interest rates decline significantly due to a low reinvestment rate, that investor may be unable to reach their long-term goal, resulting in the goal "missing" the target, but there has been no direct loss of principal.

The fundamental difference between a goal and an investment is the reinvestment environment changed and not a failure of the strategy itself. Recognising reinvestment risk will allow investors to appropriately align their investment horizons with their goal timelines.

How Investors Can Reduce Reinvestment Risk

Investors cannot fully eliminate reinvestment risk from their portfolio. However, they can plan, control, and reduce the impact of reinvestment risk in their portfolios through their choices of Fixed Income Structure and Instruments.

The diversification of Fixed Income Securities by both term and income style creates the opportunity to spread reinvestment risk across multiple years, time periods and rate environments.

To help create a well-considered plan for managing reinvestment risk, there are many platforms and companies, such as Grip, that offer curated Fixed Income Products.

Using a laddering technique or staggered investments provides the opportunity to spread out your investment over several time periods.

- Investors may select to utilize various types of bonds or financial instruments whose maturities stagger over time.

- When interest rates are increasing, the later maturing securities will typically receive a higher yield than earlier maturing securities, making it possible to offset some of the lower-earning potential of the earlier-reinvested funds.

- By utilizing the laddering technique an investor will benefit from reducing the risk associated with lower yields when reinvesting.

- In addition to bonds, laddered investments may also be built using fixed income deposits, MLDs or a combination of curated fixed income products.

2. Longer Maturity Instruments

If an investor is looking to minimize how frequently they must decide on reinvesting, selecting longer-dated investments is one way to do so. If an investor has a long-term goal that they want to achieve, they could use longer-tenured securities to match the timing of their investment to their goal.

3. Mixing Predictable Income Assets

When future expenses are on the horizon, investments that deliver steady, scheduled payouts can make cash planning far more manageable and reduce uncertainty.

To understand how these instruments fit into a stable fixed income strategy, explore our current and upcoming pieces on building resilient fixed income portfolios and managing risk effectively.

FAQs On Reinvestment Risks

1. What do you mean by "reinvestment risk" in the case of bond investments?

Reinvestment risk refers to the possibility that the individual coupon payments or proceeds from maturing bonds will not earn the same yield as those that were originally invested in.

2. Is reinvestment risk a bad thing or a good thing?

Reinvestment risk is generally considered a negative thing because it can negatively impact your long-term return on your investment. However, it can also have a positive impact during a rising interest rate period when you may be able to reinvest your proceeds into higher-yielding investments.

References:

1. Bajaj Finserv, accessed from:

https://www.bajajfinserv.in/investments/reinvestment-risk

2. Investopedia, accessed from: https://www.investopedia.com/terms/r/reinvestmentrisk.asp

3. Mstock, accessed from: https://www.mstock.com/articles/how-reinvestment-risk-work

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.