Bond Amortization: How It Works, Methods And Examples

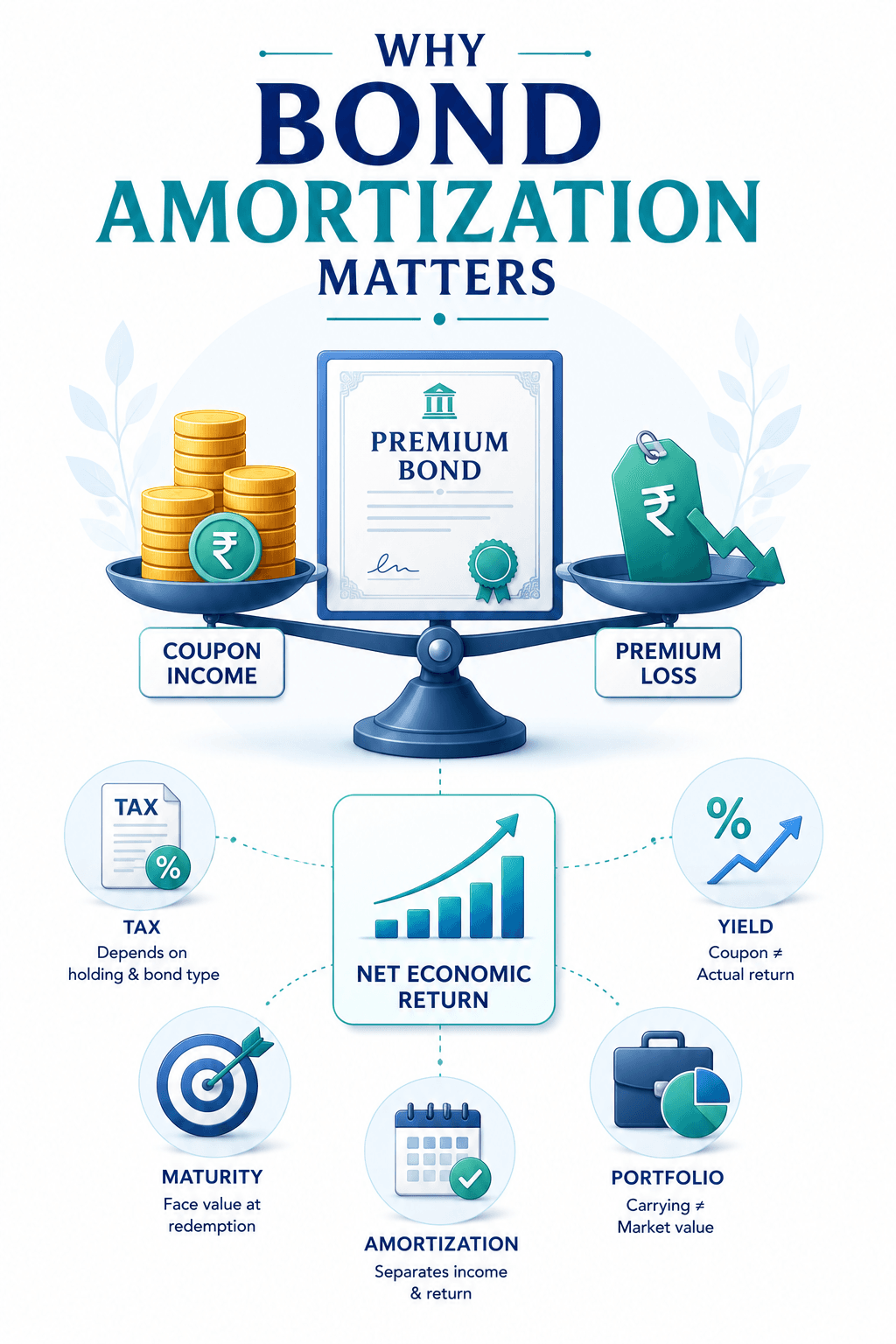

A bond does not always trade at the amount its issuer will repay at maturity. Bond amortization explains how the gap between purchase price and face value is recognised over the remaining term. Crucially, the coupon alone does not reveal the investor’s actual return. An amortized bond schedule separates cash interest, effective yield and carrying value from daily market-price changes.

Bond Amortization: What Does It Mean?

Bond amortisation is the gradual adjustment of a bond’s carrying value towards the amount repayable at maturity. When an investor pays more than face value, the excess reduces over time. When the price is lower, the difference is added gradually.

- A premium bond trades above face value. An investor may pay INR 10,500 for a bond that will repay INR 10,000. The INR 500 gap is the premium.

- A discount bond trades below face value. An INR 10,000 bond bought for INR 9,500 carries an INR 500 discount.

- An at-par bond is purchased at its face value. Since there is no difference between the purchase price and repayment amount, it generally requires no premium or discount amortisation.

These price differences often arise because the coupon differs from prevailing market yields. Credit quality, tenure, liquidity and demand can also influence the price. A high-coupon bond may trade at a premium when comparable yields fall. A lower-coupon bond may move to a discount when yields rise.

Amortisation exists because the issuer normally repays only the face value at maturity. The premium or discount must therefore be adjusted across the remaining periods to reflect the bond’s effective return and carrying value accurately.

The table below shows how each purchase position moves towards the face value by maturity.

Purchase position | Initial carrying value | Movement over time | Value at maturity |

Premium | INR 10,500 | Falls gradually | INR 10,000 |

At par | INR 10,000 | Broadly unchanged | INR 10,000 |

Discount | INR 9,500 | Rises gradually | INR 10,000 |

The price gap sets the starting point. The next step is seeing how each period changes the recorded value.

How Bond Amortization Works?

The process starts with one basic comparison ‘Did the investor buy the bond above, below or at face value?’

Five figures help explain the calculation:

- Purchase price: The amount paid for the bond, excluding separately identified accrued interest where applicable.

- Face value: The principal the issuer promises to repay, subject to the bond’s terms and credit risk.

- Cash interest: The coupon payment, usually calculated on face value.

- Interest income: Opening carrying value multiplied by the effective interest rate.

- Carrying value: The recorded value after adjusting for the premium or discount during the period.

For bond premium amortization, the cash coupon is generally higher than effective interest income. The difference reduces carrying value.

For bond discount amortization, effective interest income exceeds the coupon, so the carrying amount rises.

This movement is not the same as market performance. A bond’s quoted price can change as yields, liquidity and issuer risk change. The carrying value follows a calculated schedule when the instrument qualifies for amortised-cost measurement. IFRS 9 uses the effective interest method to calculate amortised cost and allocate interest revenue.

With these components clear, investors can compare the two main calculation methods.

Methods Of Bond Amortization

Two methods are commonly discussed, although they calculate the periodic adjustment differently.

Basis | Effective interest method | Straight-line method |

Calculation | Applies effective yield to opening carrying value | Divides the total difference equally |

Periodic adjustment | Changes each period | Remains constant |

Time value of money | Recognised | Not fully recognised |

Accuracy | Reflects actual yield more closely | Provides an approximation |

Common use | Amortised-cost financial reporting | Simple illustrations where permitted |

Effective interest method

The effective interest method calculates interest income using the opening carrying value and the bond’s effective interest rate.

Interest income = Opening carrying value × Effective interest rate

For example, assume a bond has:

- Opening carrying value: INR 10,500

- Effective interest rate: 8%

- Annual coupon received: INR 1,000

The interest income for the year is:

INR 10500 x 8% = INR 840

The difference between the INR 1000 coupon and INR 840 interest income is INR 160. This amount adjusts the carrying value for the period.

The closing carrying value becomes:

INR 10500 - INR 160 = INR 10,340

The next year’s calculation begins with INR 10,340. Since the opening value changes, the interest income and adjustment also change each period.

Straight-line method

The straight-line method divides the total premium or discount equally across the remaining periods.

Suppose a bond has an INR 500 difference between its purchase price and face value, with five annual periods remaining.

Annual adjustment = INR 500 / 5 = INR 100

The carrying value changes by INR 100 each year. The amount remains the same throughout the bond’s remaining term.

This method is easier to understand. However, it does not calculate interest income using the changing carrying value.

Bond Amortization vs Bond Depreciation

| Aspect | Bond Amortization | Bond Depreciation |

| What it reflects | Planned accounting adjustment | Market price movement |

| Basis | Based on purchase premium or discount | Based on interest rates and demand |

| Predictability | Predictable | Can change daily |

| Duration | Continues until maturity | May reverse if market conditions change |

A bond can depreciate in the market even while its carrying value continues to move according to its amortisation schedule. The two concepts serve different purposes and should not be confused.

Why Investors Should Understand Bond Amortization?

The schedule separates the coupon received from the economic return earned.

- Tax implications: Accounting amortisation does not automatically create a tax deduction. Interest from taxable bonds is generally added to taxable income.

- Listed bonds held for more than 12 months generally attract 12.5% long-term capital gains tax without indexation.

- Shorter holdings are taxed at the applicable slab rate.

- Gains on unlisted bonds transferred, redeemed or matured on or after 23 July 2024 are treated as short-term under Section 50AA, irrespective of the holding period. Tax treatment can vary by instrument and investor.

- Yield calculation: A premium bond can have a coupon above its yield to maturity because part of the coupon offsets the premium lost by redemption. A discount bond works in the opposite direction.

- Portfolio reporting: Carrying value, market value and redemption value are different measures. Mixing them can overstate income or create a misleading loss.

- Maturity planning: Redemption may equal face value, not the purchase amount. Investors should include the premium or discount when matching bonds with future goals.

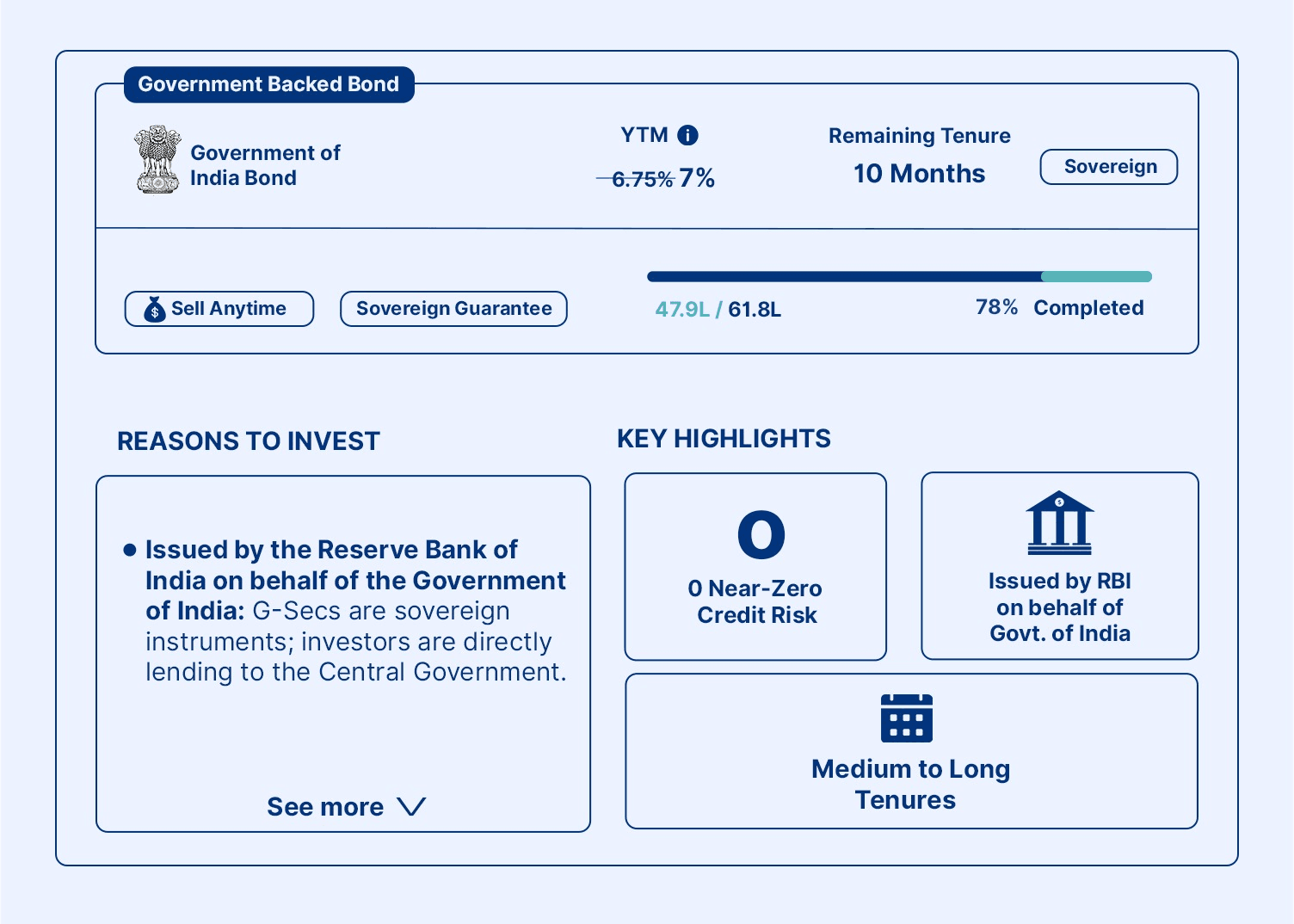

Let us understand this with an example of a government bond:

The bond shown is a Government of India security carrying a 7.02% annual coupon. It matures on 27 May 2027 and pays interest semi-annually.

The return illustration uses 5 units.

Step 1: Calculate the total face value

Each unit has a face value of INR 100.

Total face value = 5 units x INR 100 = INR 500

The Government of India will repay this INR 500 principal amount at maturity.

Step 2: Calculate the coupon payments

The annual coupon rate is 7.02%.

Annual interest = INR 500 x 7.02% = INR 35.10

Since the bond pays interest twice a year:

Semi-annual interest = INR 35.10 / 2 = INR 17.55

The expected payments are:

Payment date | Interest | Principal | Total payment |

27 November 2026 | INR 17.55 | Nil | INR 17.55 |

27 May 2027 | INR 17.55 | INR 500 | INR 517.55 |

Total | INR 35.10 | INR 500 | INR 535.10 |

Step 3: Compare the coupon rate and YTM

The bond offers:

- Coupon rate: 7.02%

- Yield to maturity: 7%

The coupon rate exceeds the YTM by 0.02% points. This suggests that the bond may trade at a small premium to its face value.

The difference is limited because the coupon rate and YTM are nearly identical.

Step 4: Identify the premium

Assume the bond’s clean purchase price is marginally above INR 500 because its coupon exceeds the prevailing yield.

For illustration, suppose the investor pays a clean price of INR 500.10.

Bond premium = INR 500.10 - INR 500 = INR 0.10

This INR 0.10 premium must gradually reduce before maturity because the investor will receive only INR 500 as principal repayment.

Accrued interest, if any, should be treated separately. It forms part of the dirty price paid to the seller but does not represent a bond premium.

Step 5: Apply bond premium amortisation

The effective interest method calculates interest income using the bond’s opening carrying value and effective yield.

Assuming two remaining semi-annual periods, the periodic yield is:

Semi-annual yield = 7% / 2 = 3.5%

Period | Opening carrying value | Effective interest income | Coupon received | Premium amortised | Closing carrying value |

First period | INR 500.10 | INR 17.50 | INR 17.55 | INR 0.05 | INR 500.05 |

Second period | INR 500.05 | INR 17.50 | INR 17.55 | INR 0.05 | INR 500.00 |

During the first period:

Effective interest income = INR 500.10 x 3.5% = approximately INR 17.50

The investor receives INR 17.55 as cash interest. The difference of around INR 0.05 represents premium amortisation.

The carrying value consequently falls from INR 500.10 to approximately INR 500.05. After the second adjustment, it reaches the INR 500 redemption value.

Common Mistakes Investors Make While Understanding Bond Amortization

Some common misconceptions include:

- Assuming coupon rate equals actual return

- Ignoring the purchase price while calculating returns

- Confusing amortised cost with market value

- Believing premium bonds generate higher yields than discount bonds

- Comparing bonds only on coupon instead of Yield to Maturity (YTM)

Understanding these differences helps investors compare fixed-income investments more accurately.

When Does Bond Amortization Matter?

Most retail investors hold bonds until maturity and mainly focus on coupon income and redemption value. In such cases, daily amortisation calculations may not affect investment decisions directly.

However, bond amortisation becomes more relevant when investors:

- Purchase bonds at a premium or discount in the secondary market

- Compare coupon rate with Yield to Maturity (YTM)

- Maintain a diversified bond portfolio

- Review financial statements prepared using amortised-cost accounting

- Sell bonds before maturity

Understanding when amortisation matters helps investors interpret bond returns more accurately instead of relying only on the coupon rate.

Using Bond Amortization To Make Better Investment Decisions

Understanding bond amortisation helps investors see how coupon income, purchase price and maturity value affect actual returns. The next step is to apply that understanding while building a diversified fixed-income portfolio.

Corporate bonds offer a range of yields, tenures, coupon frequencies and credit profiles. This allows investors to diversify across issuers, sectors and maturities instead of relying on a single investment.

Grip Invest provides access to curated fixed-income opportunities, including corporate bonds, enabling investors to compare instruments based on yield, tenure, credit rating and risk appetite. A well-diversified portfolio can help reduce concentration risk while creating a more balanced and predictable income stream.

FAQs On Bond Amortization

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001