1994 Bond Market Crisis: Causes, Impact, Key Lessons And What Investors Can Learn

The stock market crash during the 2008 financial crisis needs no introduction. Just thinking about it can still make an investor jittery. But how many of you remember or even know about the biggest bond market crisis that happened in 1994?

Let us first give you a fair idea about what had happened, and then explain what led to it and what investors can learn from it.

The Bond Market Crisis Of 1994

After the recession in the early 1990s, the 1994 bond market crisis, or Great Bond Massacre, was a big bomb that dropped on the financial markets. It was a sudden and drastic fall in bond market prices across the developed world. It began in Japan and the United States (US), and spread through the rest of the world. With $1.5 trillion lost in market value across the globe, the crash has been described as the worst financial event for bond investors.

So, in this blog, let us deep dive into various aspects of the 1994 bond market crisis, what all led to it, and what you, as an investor, can learn from this crisis that happened three decades ago.

What Led To This Crisis?

- The 1994 bond market crisis was a significant financial event that caused widespread disruptions in global financial markets, particularly affecting, of course, the bond market. Basically, the bond market crisis was mainly triggered by a combination of factors, including monetary policy changes, a shift in investor sentiment, and the economic environment.

- If we look at the year before the crisis, i.e. in 1993, the bond market was enjoying a relatively bullish run following a recession that plagued many industrialised countries a few years earlier. To give you a fair idea about what was happening at that time, the long term interest rates were nearing 30-year lows throughout much of Europe, with France and Germany's rates being even lower than the US's at that time. European investors had predicted that short-term rates would continue to decline into 1994 and bring with them shrinking long-term rates, which would thus enhance their leverage on current bond holdings.

- However, the twist came prior to the crash, when some financial analysts in the US forecasted a hike in the yields of 30-year treasury bonds, which would be prompted by the Fed (US’ central bank) raising interest rates to combat inflation. This was in contrast to what investors were expecting, right? Fast forward to January 1994, the President of the Standard & Poor's (S&P) Index at that time, Leo O'Neill, warned that overconfidence in the economy would spread through the markets. He said so because he had noticed that, despite the majority of junk bonds issued by the corporate sector earning upgrades for the first time since 1980, the dollar value of those that had been downgraded actually exceeded these by more than $110 billion.

That is why his prediction worried that any contractionary moves by the US central bank would significantly depress the returns on bond funds. At the same time, other analysts were offering a more optimistic outlook, arguing that inflationary pressures were relatively absent and failed to manifest despite the economy's recent recovery.

What Happened Next? Who Proved To Be Right?

Well, the crash happened in early 1994.

- Although bond prices in Japan had started plummeting just a month earlier, the immediate trigger of the crash in the US occurred at the Federal Open Market Committee (FOMC) on February 3 and 4, 1994. That committee was of the view that a slight rise should be made for its federal funds rate target, from 3% to 3.25%.

- This was the US central bank's first move to shrink the money supply since 1989. Over the rest of 1994, the Fed had come up with not just one but several other contractionary moves. The US central bank increased its target by 25 basis points in March and April, 50 points in May and August, and 75 points in November. By its last meeting of the year, the rate stood at 5.5%.

- The Fed's first announcement of the year, combined with an array of other factors within and outside the US, prompted investors to do a mass sell-off of bonds and debt funds worldwide, and not just in the US.

- Starting in March 1994, as the bond market's newfound turbulence became more settled in investors' minds worldwide, homeowners were discouraged from refinancing their properties further due to the rise in long-term rates. As a result of the crash, bonds had lost a massive market value of about $1.5 trillion globally, with nearly $1 trillion of the losses applicable to US debts.

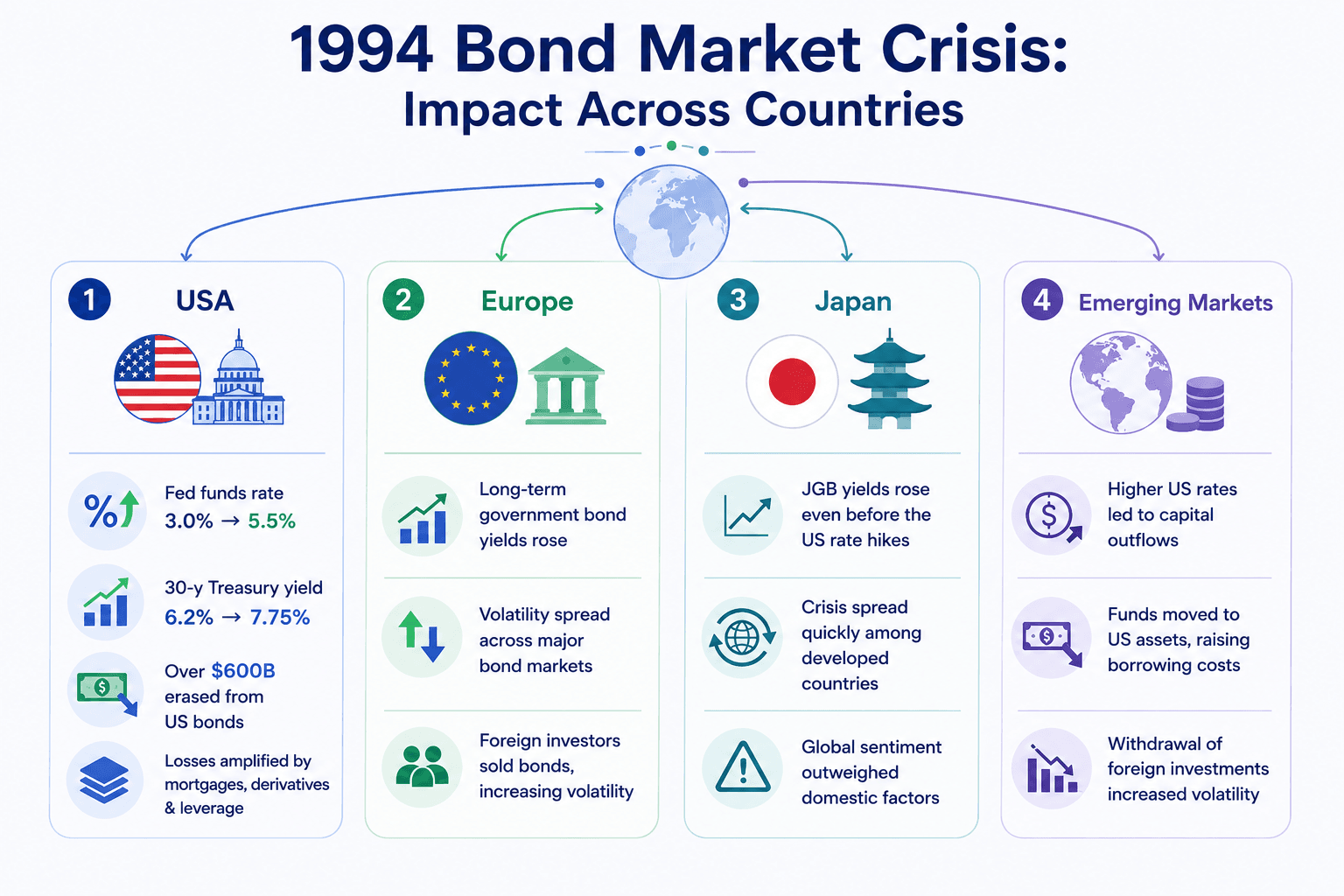

How The 1994 Bond Market Crisis Impacted Various Countries

The 1994 bond market crisis soon spread beyond the US. This pushed bond yields higher across major economies, showing how closely global bond markets were linked to each other.

1. USA:

The federal funds rate was up from 3.0% to 5.5% between February and November 1994. This significantly lifted Treasury yields.

It was also estimated that rising 30-year Treasury yields, from 6.2% to 7.75%, erased over USD 600 billion in value from US bonds within months.

The losses were further amplified by the growth of mortgage securities, derivatives and leveraged bond strategies that had flourished during years of low interest rates.

2. Europe:

The European bond markets followed what happened in the United States. While the economic situation and inflation were not the same.

Long-term government bond yields increased significantly in Europe as investors repriced interest-rate expectations.

The volatility spread across major bond markets. This reflected that global markets had become closely connected.

Many foreign investors also started selling their bond holdings, which increased market volatility and helped the crisis spread across countries faster.

3. Japan:

Japanese government bond yields started rising even before the US Federal Reserve raised interest rates. This made Japan one of the first countries to feel the impact of the global bond sell-off.

The crisis quickly spread between developed countries, with Japan both affecting and being affected by global bond market movements.

The crisis showed that global investor sentiment can sometimes have a bigger impact than the economic conditions of a country, especially during periods of heavy market selling.

4. Emerging markets:

Higher US interest rates resulted in many investors pulling money out of emerging markets. This made it harder and more expensive for these countries to raise funds.

Investors moved their money into US assets by reducing investments in emerging markets that raised their borrowing costs.

The withdrawal of foreign investments was one of the main reasons market volatility increased during 1994.

The Two Big Collapses

The 1994 bond market crisis exposed the dangers of leverage, causing some of the biggest institutional investment failures of the decade.

1. Orange County Investment Pool Collapse

The treasurer and tax collector of Orange County, Robert Citron, used reverse repurchase agreements and invested in derivatives to earn higher returns while interest rates were low.

His strategy involved buying securities, using them as collateral to borrow more money, and then investing the borrowed money in derivatives. The strategy worked only as long as interest rates stayed low.

When the Federal interest rates were raised in 1994, the investments started losing value. And by November 1994, it was found that his investments had resulted in a USD 1.64 billion loss.

On 6 December 1994, Orange County went bankrupt, which is the largest municipal bankruptcy in US history.

2. Steinhardt Partners’ Hedge Fund Blow-up

Steinhardt Partners built a USD 30 billion position in Eurobonds by using heavy leverage because it expected bond prices to stay strong.

The fund lost about USD 4 million every time European interest rates increased by one basis point or 0.01%.

By May 1994, the fund had lost around one-third of the USD 4.6 billion it managed as bond prices continued to fall.

After delivering more than 60% annual returns in each of the previous three years, the fund was still down more than 30% at the beginning of September 1994.

What Changed After The Crisis: Regulatory Reforms And Risk Management Shifts

The 1994 bond market crash exposed major weaknesses in how financial institutions measured and managed market risk. The sharp losses showed that traditional risk models were not fully prepared for sudden and widespread market sell-offs. As a result, regulators, accounting bodies and financial institutions introduced several changes to improve risk management and transparency.

1. Shifts in Value-at-Risk (VaR) Framework:

The crisis reflected that the traditional VaR models were built on short-term data. They were underestimating the correlated sell-offs across global markets.

After 1994, institutions started using stress testing, scenario analysis, and back-testing alongside VaR to better measure extreme market risks.

Many firms also shifted from relative VaR, which measures risk against a benchmark, to absolute VaR, which focuses on limiting total portfolio losses.

2. FASB Disclosure Requirements:

The losses from derivatives during the 1994 bond market crisis made people want companies to be more open about their financial dealings. The Financial Accounting Standards Board, or FASB, introduced and strengthened accounting standards to help investors understand how much risk companies that deal with derivatives and market changes are taking.

Some of the key changes included:

- FAS 119, 1994: This requires companies to disclose the amount and terms of their derivative instruments.

- FAS 133, 1998: This requires all derivatives to be reported on the balance sheet at fair value. This also required changes in their fair value to be recognised in earnings unless they qualified for specific hedge accounting treatment.

- FAS 157, 2006: It introduced a definition of fair value and created the three-level fair value hierarchy: Level 1, Level 2 and Level 3. This was to improve consistency and transparency in asset valuations.

3. GASB Disclosure Requirements:

The 1994 crisis also affected state and local governments in the United States. Following these events, the Governmental Accounting Standards Board, or GASB, introduced reporting requirements for government investment portfolios.

Key reforms included:

- GASB Technical Bulletin 1994-1: This requires governments to disclose the nature, notional amounts, fair values and risks of derivative investments.

- GASB Statement 40 2004: This required detailed disclosures relating to investment risks, including interest rate, credit and foreign currency risk.

- GASB Statement 53 2008: This established comprehensive accounting and reporting standards for derivative instruments. This requires them to be measured at fair value and set clear rules for hedge accounting.

What Lessons Investors Can Learn From 1994’s Bond Market Crisis

The 1994 bond market crisis highlighted the risks of sharp interest rate movements and the importance of anticipating how bond prices are impacted by such changes. Here are the big lessons investors can learn from it:

1. The crisis reminds us that interest rates & bond prices are inversely related

One of the biggest lessons, or rather a reminder, that the 1994 bond market crisis gave us, is the strong inverse relationship between interest rates and bond prices. When interest rates are on rise, bond prices tend to fall. As we saw in that crisis, the US central bank’s unexpected tightening in 1994 led to a sharp increase in bond yields, which thus caused bond prices to drop drastically.

But who suffered the most? Well, investors with long-duration bonds (i.e., bonds with longer maturities) were hit the hardest, because the price of long-term bonds is more sensitive to changes in interest rates than shorter-term bonds.

2. The crisis proved that the central bank’s surprise actions can catch the market off guard

The US central bank (Federal Reserve) raised short-term interest rates aggressively from February 1994 to November 1994, in an attempt to curb inflationary pressures. But the market wasn’t expecting this, which is why it was caught off guard. This reminds us of the importance of closely monitoring central bank actions and communications. A surprise policy shift, like the one that happened in this case, can cause significant volatility in financial markets.

Such unexpected changes/announcements demonstrated the vulnerability of bond investors to liquidity risks. So, those who had borrowed heavily to invest in bonds were forced to sell assets at a loss when prices fell, thus aggravating the market decline.

3. The crisis showed how emerging markets feel the ripple effects of global interest rates

As we discussed earlier in this article, India was among the emerging markets that had issued dollar-denominated debt or were dependent on capital inflows, and thus got hit by the 1994 bond market crisis. The rise in U.S. interest rates made dollar-denominated debt more expensive to service, and many emerging market currencies, including India’s Rupee, depreciated as a result.

That is why, this 1994 crisis showed that monetary tightening in developed economies (like the US) does have significant spillover effects on global markets, especially for emerging markets in India, with high levels of foreign-denominated debt.

4. The crisis served as a reminder to always diversify your portfolio

Another big reminder, and also a lesson, that the bond market crisis gave us, was to always diversify your portfolio. The bond selloff affected many sectors, but the damage was particularly severe for certain asset classes, such as high-duration, long-term Treasury bonds and certain high-yield debt. That is where diversification

across asset classes, maturities, and geographies can help mitigate the impact of unexpected market shocks like the one seen in the 1994 crisis.

Conclusion

Now that you have read this long but hopefully not boring article till the end, we all can agree that the 1994 bond market crisis was a wake-up call for investors. It serves as a crucial lesson by highlighting the importance of understanding the dynamics between interest rates and bond prices. It also underscores the need for vigilance regarding central bank policies, as unexpected actions can lead to significant market volatility and at worst, a repeat of such a crisis. To learn more about investments and portfolio diversification, sign up on Grip Invest.

FAQs On 1994 Market Crisis

References:

1. Fasb, accessed from: https://www.fasb.org/page/PageContent?pageId=/reference-library/superseded-standards/summary-of-statement-no-119.html&bcpath=tff

2. Fasb, accessed from: https://storage.fasb.org/fas133.pdf

3. US Money Reserve, accessed from: https://www.usmoneyreserve.com/news/executive-insights/the-great-bond-m-lessons-of-1994/

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001