Best Mutual Funds For Child Education: Planning Smartly For Future Costs

Planning for your child’s higher education is one of the most common goals in personal financial management. It is critical to understand the importance of choosing the right asset classes for your investments to ensure you have enough savings when the time comes.

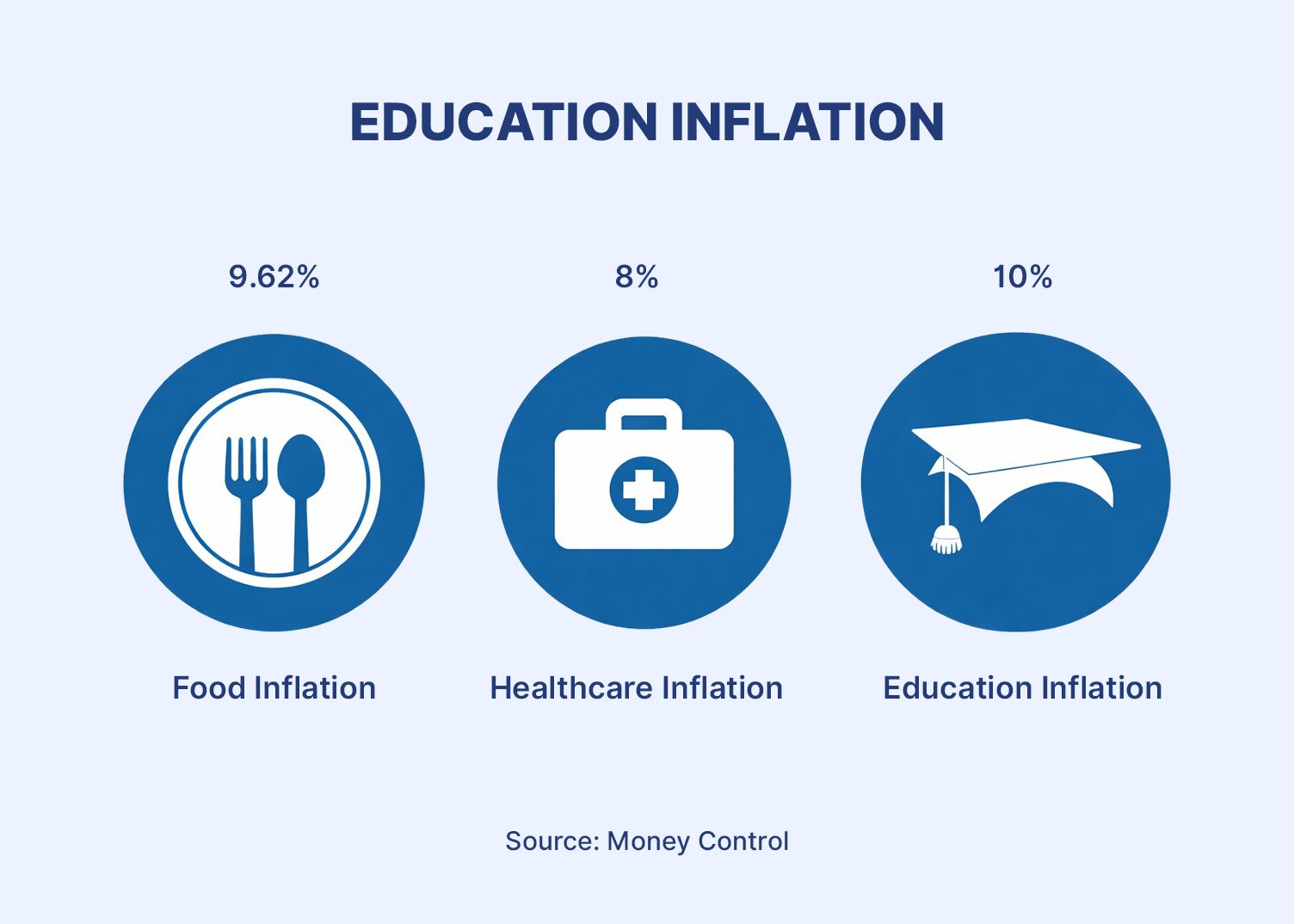

Investing in your child’s higher education is critical, given the high inflation in India's higher education sector. According to some estimates, the inflation rate is between 10% and 12%1.

A few other estimates underline that education inflation can be as high as 15% in India2. This implies that a degree costing INR 10 lakhs now is expected to cost upwards of INR 30 lakhs in the next 15 years.

One of the best ways to plan for your child's education is to start investing in the best mutual fund for child education.

It will establish a disciplined approach to investing and help you avoid financial strain when it is time to pay for your child's education in future.

Why Mutual Funds For Child Education

The best mutual fund for child education can generate long-term wealth and is therefore considered the most popular investment strategy.

1. Long-Term Growth Potential

Over the long term, equity mutual funds typically provide annual returns of 10–14%. However, equity mutual funds are subject to market risks and volatility.

If everything goes well, the expected return is enough to protect against inflation while generating growth in your investment.

Investment in child education investment plan India can save you from educational uncertainty.

2. SIP Flexibility

Child education can be funded using SIPs. You can use smaller amounts each month towards funding a SIP for child education.

You do not have to provide a large lump sum up-front, thereby ensuring a smooth investment process.

3. Power of Compounding

The golden rule is to start as early as possible. With a longer tenure, the power of compounding helps in creating a snowball effect with your investment and appreciation increasing at an exponential rate.

Types Of Funds To Consider

Choosing the best SIP for your child education India depends on both your investment horizon and the level of risk you are willing to accept.

1. Equity Funds

Equity funds are suited for long-term investment portfolios, particularly when the investment tenure exceeds 10 years. These funds invest mainly in stocks and have the potential to generate returns of 10-14%.

Parents of young children should invest in an equity SIP for child education, as their children can withstand short-term market fluctuations.

However, even in the long term, these funds are subject to market volatility.

2. Hybrid Funds

Investing in hybrid funds can be one of the best education planning investment options. It includes both equity and debt instruments and offers moderate risk, with returns of 8-10%.

Hybrid funds are best for mid-term investors or those who prefer a shorter investment tenure than equity funds.

3. Child Specific Funds

Child-specific funds are long-term investment portfolios and can be included in a structured child future investment plan India.

These funds offer a lock-in period, a significant advantage for disciplined investing.

However, they may not offer the same level of flexibility as regular mutual funds.

How To Choose The Right Fund

Selecting the best SIP for child education India requires a detailed personal financial assessment. Calculating risk and calculating return after a desired time period is crucial for parents.

Here are some points that need to be discussed before signing on to any SIP for child education:

Risk Profile

It is vital to understand your risk profile before investing in any fund. If you are comfortable with market volatility, you can invest in equity-based funds.

If your risk profile is moderate, you can invest in hybrid funds. If your risk profile is conservative, then it is better to invest in debt-based funds.

Time Horizon

Your investment strategy should match your child’s age and the time available for education. If your child is younger, you can invest in more equity-based funds.

If your child is closer to completing their education, it is better to invest in safer assets and education planning investment options to protect your accumulated corpus from market volatility.

Fund Performance

It is vital to assess the fund's performance before investing. It is not wise to focus on short-term performance. Instead, look at the fund's performance over 5-10 years.

It is vital to assess the fund manager's performance before investing in any fund.

Investment Strategy

Having a proper investment strategy will help transform your child’s dream of an education into a specific, realistic goal. Rather than investing randomly, a proper investment strategy will enable you to invest regularly and systematically, and help you build a strong education fund.

SIP Approach

The SIP approach will enable you to invest a fixed sum of money regularly, making wealth creation a hassle-free, simple process.

1. Step-Up SIP

The step-up SIP will take your investment strategy to the next level, allowing you to invest more as your income grows.

This will enable you to beat inflation and achieve your child’s educational goals with greater confidence.

2. Goal-Based Investing

Goal based investing for education will give every rupee you invest a sense of purpose.

By having a clear educational goal, you will stay focused and motivated, making your investment goal-oriented and helping you meet your child’s future aspirations.

Additional Tips For Smart Planning

- Get started as early as possible, so monthly payments won’t be too hefty.

- Have multiple sources of investment funds (2-3).

- Check your portfolio annually.

- Diversify your portfolio with fixed income securities such as corporate bonds, which not only provide stability of returns but also reduce overall market exposure.

Conclusion

Planning for your child’s education is no longer optional, it is a financial necessity in today’s rising cost environment. Mutual funds, especially when combined with disciplined SIP strategies, offer a practical way to build a long-term corpus that can keep pace with education inflation.

However, relying solely on equity-based investments may expose your portfolio to market volatility, especially as your goal approaches.

A well-rounded approach involves aligning your investments with your time horizon, risk profile, and financial goals. Gradually shifting towards more stable instruments as you near your target can help preserve the corpus you have built over the years.

Additionally, combining mutual funds with fixed income options can provide better balance, predictability, and risk management.

To make your child’s education plan more resilient, consider complementing mutual fund investments with curated fixed-income opportunities on Grip Invest, helping you build a more stable and goal-aligned portfolio.

FAQs On Best Mutual Funds For Child Education

References:

1. Kotak MF, accessed from: https://www.kotakmf.com/Information/blogs/education-inflation-india-rising-costs_

2. India Macro Indicators, accessed from: https://indiamacroindicators.co.in/resources/blogs/can-families-outrun-education-inflation-in-india

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001