Best Small Cap Mutual Funds In India 2026: Top Picks, Returns And How To Choose

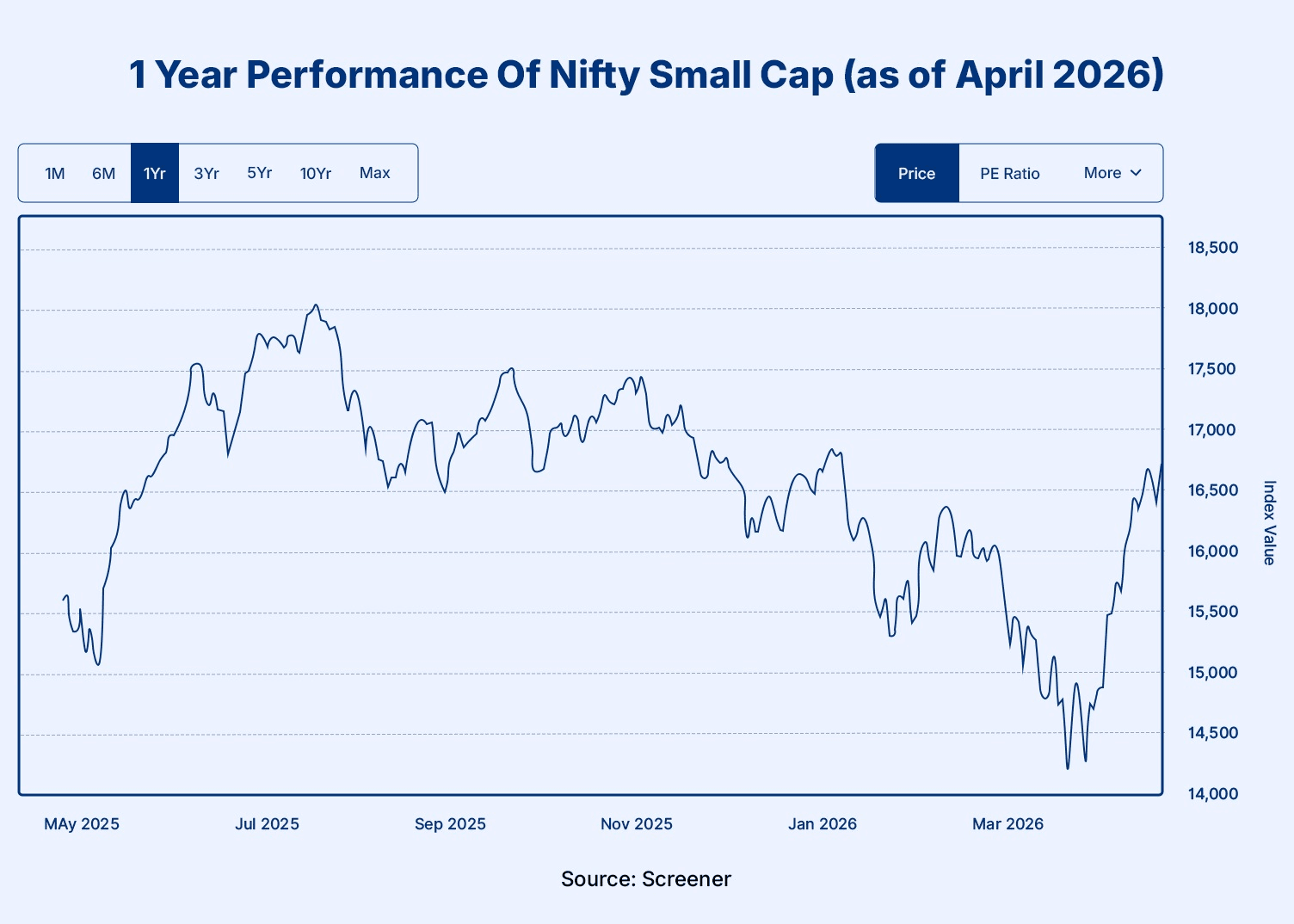

The performance of small-cap mutual funds does not taper down softly; rather, it is a harsh correction. The average decline witnessed in 2025 was 11.7%, while a few funds were down by as much as 18%. Investors were caught off guard, given that the previous period had been one of consistent growth for them.

However, this kind of behaviour is characteristic of small-cap mutual funds. Small-cap stocks have an inherently volatile nature due to their growth potential. Despite the volatility, small-cap mutual funds are worth the risk because they invest in young companies that may grow into dominant players in their industries in the future.

In this blog post, we shall discuss the best small-cap mutual funds for 2026 and how you can choose between different investment opportunities for a growth-based investment portfolio.

Top 5 Small-Cap Mutual Funds In 2026

Following is a tabular description of the most effective small-cap mutual funds operating in India, which provides a thorough analysis of their performance and other relevant criteria, including expenses, exit charges, and the risk involved.

Fund Name | AUM (INR Cr) | 3Y CAGR | 5Y CAGR | Expense Ratio | Risk Rating |

| Quant Small Cap Fund - Direct Plan - Growth | 29,463 | 28.6% | 35.72% | 0.64% | Very High |

| Nippon India Small Cap Fund - Direct Plan - Growth | 65,922 | 26.9% | 32.11% | 0.78% | Very High |

| Bandhan Small Cap Fund - Direct Plan - Growth | 14,062 | 25.7% | 31.52% | 0.69% | Very High |

| Tata Small Cap Fund - Direct Plan - Growth | 11,576 | 24.3% | 30.76% | 0.71% | Very High |

| HSBC Small Cap Fund - Direct Plan - Growth | 16,536 | 23.8% | 30.16% | 0.72% | Very High |

Source: Data has been taken from Moneycontrol (As of 25 April 20262.

NOTE: Please note that the historical performance of a mutual fund does not guarantee future performance. It is one way of analysing the performance of a mutual fund. Investors are advised to check all the offer-related documents carefully before selecting any mutual fund. These top 5 small-cap mutual funds are selected on the basis of above mentioned criteria; however, the top 5 funds can be different for different individuals if they change their criteria. For example, an individual may not want to omit the funds having an AUM less than INR 10,000 crores, or he/she may also want to consider the expense ratio and fund age too.

The Benchmark For Small-Cap Mutual Funds In 2026

The Nifty Small Cap 250 and S&P BSE 250 SmallCap Index are excellent yardsticks for comparing small-cap mutual fund performances. As seen in 2025, these two benchmarks had short-term negative performances of about 9%. However, their impressive long-term results, attributed to their high growth rates within several years, illustrate the hidden strengths of the small-cap industry.

It should be noted that short-term losses coupled with high growth in the long run are typical of small-cap investments. Even though the market correction may be dramatic, it does not detract from the overall positive trend.

Why Choose Small-Cap Mutual Funds ?

Small-cap mutual funds offer some of the most compelling opportunities in equity investing. A number of emerging growth companies are under the radar that can still offer high returns. Here is why these funds are worth a place in a growth-oriented portfolio:

1. Early-Stage Companies With Growth Potential

These funds typically invest in companies ranked below the top 250 by market capitalisation, often uncovering lesser-known firms with significant growth potential. These businesses are in their early stages, and their business fields have high growth potential. Funds like the Nippon India small-cap fund target such companies and have shown strong returns over time.

2. Long-Term Capital Appreciation

Small-cap mutual funds allow you to invest in businesses within the growth period. Most of these firms may become medium-cap or large-cap leaders over time. Top-performing small-cap funds have rewarded early investors with substantial long-term returns.

Small-cap funds have been demonstrated to be able to beat the overall markets on a longer-term basis. Some well-managed small-cap schemes have achieved over 25-30% annualised returns over ten years, which shows their potential to create wealth in the long run.

3. SIPs Help Average Entry Cost

Small-cap investments are well-known in terms of volatility. Systematic Investment Plans (SIPs) help smooth out investment volatility by averaging purchase prices over time. SIPs average the cost of purchase into a line and reduce the probability of buying at the high point while removing the stress of timing the market to invest in small-cap stocks safely.

How To Select A Small-Cap Fund ?

Choosing an excellent mutual fund in the small-cap category involves more than just analysing the performance of the fund. Although there is value in measuring a mutual fund in terms of 1-year CAGR or 5-year CAGR, the measures do not completely factor in other considerations such as consistency, risks, and fund management.

Some important factors in choosing an appropriate small-cap fund include:

1. Rolling Returns

While point-to-point returns only give the return earned between two specific points in time, rolling returns offer a better understanding of a fund's historical performance. They reflect the returns for a period within another time frame, such as 3-year rolling returns over the past 5 years. Consistency in rolling returns makes a fund more dependable than one with volatile results.

2. Downside Capture Ratio

This is a measure of how much the investment portfolio declines compared to the market. The upside capture ratio below 100% shows that the mutual fund is underperforming the benchmark in terms of decline during bear markets. The downside capture ratio is relevant for small-cap mutual funds due to their inherent volatility.

3. Sharpe Ratio

A Sharpe ratio assesses the performance of investments after considering the amount of risk involved. This ratio calculates the extra gains made on a given investment as compared to a risk-free investment. The higher the Sharpe ratio, the more gains the fund makes relative to the risks involved.

4. Duration of Fund Manager

The expertise and the reputation of the fund manager are very important when considering investments in small caps. The longer a fund is run by the same person or group (for at least 3-5 years), the more confidence one gets about the consistency of the investment approach.

Small-Cap Fund Performance During Market Crashes

Small-cap mutual funds are known to be more volatile during economic crises when compared to large-cap and mid-cap mutual funds. For instance, in the COVID-19 crash of 2020, small-cap funds experienced drastic drops in value because many individuals preferred moving their investments to safer securities. However, small-cap mutual funds also experienced significant recoveries in subsequent years.

Another example where small-cap funds experienced a drop in value is the 2022 economic correction, which was caused by increasing interest rates and global risks. This shows that while small-cap funds experience significant falls in value during crises, they can potentially perform excellently after a period of time.

Investors must prepare themselves for the volatility in order to benefit from these funds in the future.

Key Considerations Before Investing In Small-Cap Funds

Investing in the best small-cap mutual funds can be rewarding for those who choose wisely. Assess the following critical factors before investing:

1. Fund Manager Expertise

Small-caps are characterised by more volatile stocks than large- or mid-caps. It demands financial transparency and professional decision-making to find the available potential opportunities.

A good fund manager will be able to identify underpriced companies with good growth potential and be able to enter and exit the market in a more intelligent way. It is important to consider the track record of the fund manager in the small-cap space. The past performance can tell you if they have consistently added value through multiple market phases.

2. Volatility Tolerance

Small-cap mutual fund returns in 2025 have displayed considerably higher price volatility compared to the large-cap funds. Small-cap schemes have been known to have volatility (standard deviation) often well beyond the norms in their category. It can match or exceed the preferred range, as seen in some of the leading funds.

3. Investment Horizon Of 5+ Years

The small-cap funds normally require a holding period of 5 to 7 years to establish a smooth volatility and benefit from compounding. Shorter time frames subject you to market signals as opposed to market fundamentals.

Long-term duration (ideally 7+ years) can increase the probability of taking an entrepreneurial business cycle. Moreover, you can generate a significant capital appreciation even after an interim correction.

4. Financial Goals

Small-cap funds are best for long-term capital appreciation and should be considered for goals like a child's education or retirement planning, not for short-term needs such as vacation planning.

5. Portfolio Diversification

Allocate a portion of your investment to small-cap funds to diversify your existing portfolio across different market capitalisations, which can help balance overall risk and enhance returns. Putting all your money in just small-cap funds or even in only equity funds can be very risky. Thus, you should further diversify your portfolio with fixed-income investments like corporate bonds. These debt instruments offer stability when the market is in times of stress.

How To Invest In Small Cap Mutual Funds In 2026 ?

Making investments in small-cap mutual funds requires a systematic procedure. The following steps may help you begin your journey into the world of mutual funds:

- Decide between the direct fund and the regular fund

Direct funds provide a platform where investors can invest directly without any involvement from middlemen and generally offer a lower expense ratio, thereby giving higher returns in the long run.

- SIP to the Rescue

A Systematic Investment Plan will assist you in investing a specified amount regularly, thereby ensuring that the volatility in the markets does not affect the investment plan too much. As small-cap mutual funds may have high volatility, using an SIP ensures that costs are averaged out over time.

- Diversify your investments

Despite being high on growth prospects, it is advisable not to place all your eggs in one basket. This means do not concentrate on small-cap mutual funds alone; diversification is essential.

Though there is scope for capital appreciation with small-cap mutual funds, the addition of investment vehicles that are fairly stable, such as corporate bonds through investment platforms such as Grip Invest, will ensure balanced investing.

Conclusion

Small-cap mutual funds offer high-growth opportunities that are associated with inherent volatility. Combine small-cap funds with fixed-income or stable investments such as bonds or securitised debt instruments to manage risk more effectively. Balancing with other asset classes helps mitigate short-term volatility while supporting long-term wealth creation. Diversification is not only a matter of returns but also a matter of resilience. To learn more about investments and portfolio diversification, log in to Grip Invest today.

FAQs On Small-Cap Mutual Funds

References

- Economic Times, accessed from: https://economictimes.indiatimes.com/mf/analysis/are-smallcap-mutual-funds-losing-shine-returns-dip-sharply-up-to-18-in-2025/articleshow/120953206.cms

- Money Control, accessed from: https://www.moneycontrol.com/mutual-funds/

- Screener, accessed from: https://www.screener.in/company/SMALLCA250/

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001