Bond Convexity Explained: Why Duration Alone Is Not Enough

In the fixed income market, the concept of “duration” is found to be the cornerstone for measuring the sensitivity of the prices of the bonds to any changes that may occur due to fluctuations in interest rates. However, there is a hidden risk that is embedded in the concept of “duration,” which is the inability of the linear measure of “duration” to effectively measure the nonlinear relationship between the prices and the yield levels of the bonds.

Bond Convexity addresses this shortfall. It is defined as the measure of how the value of the duration changes due to the changes in the yield levels of the bonds. This is the reason why “duration” is not enough to assess the risks of the bonds.

What Is Bond Convexity?

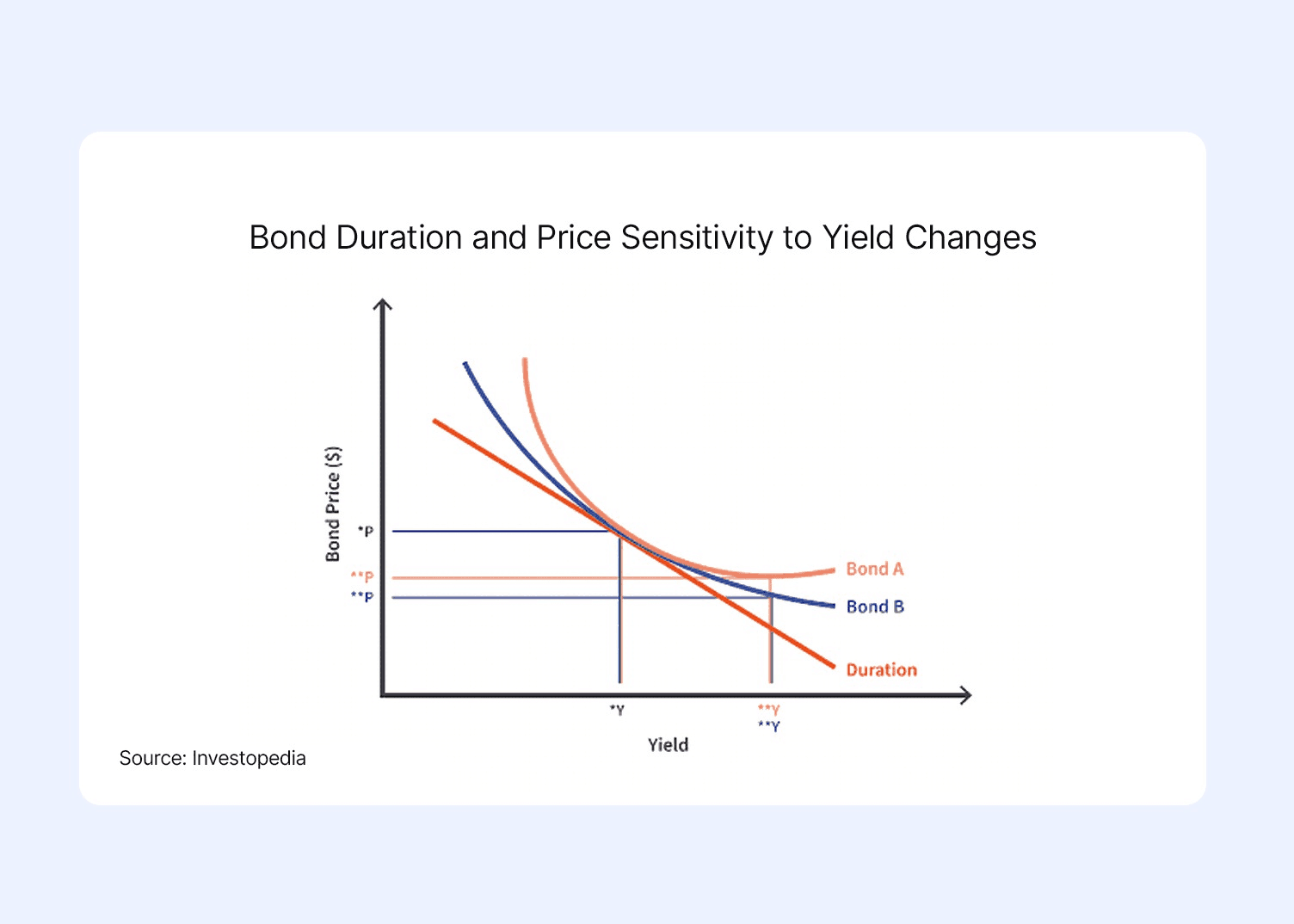

Bond convexity is the measure of the curvature of the relationship between the price of a bond and its yield, which can be viewed as the second derivative of the price with respect to changes in the yield. While duration measures the linear approximation of the relationship between price and yield, convexity measures the non-linear acceleration or deceleration of this relationship.

Mathematically, convexity is a refinement of the forecasts made by duration. To be specific, when yields fall, duration understates the possibility of a rise in price, and when yields increase, duration overstates the possibility of a fall in price. Investors are attracted to bonds with high convexity because they provide more desirable return properties in a world where rate uncertainty prevails.

How Convexity Affects Bond Prices?

Bond convexity explains the behavior of bond price curvature, demonstrating why it is necessary to simultaneously analyze both duration and convexity when managing interest rate risk measures. The convexity-driven pricing trend benefits bonds during times of market turbulence.

The major implications of convexity are as follows:

- Increased benefits from yield decreases: A 1% decrease in yield causes prices to increase more than proportionally, as measured by duration, because of increasing sensitivity.

- Reduced losses from yield increases: The same 1% increase in yield causes prices to decrease less than proportionally, as measured by duration, because of decreasing duration sensitivity with higher yields.

- Greater importance for large yield changes: Convexity matters more in times of market turbulence, where 2-3% yield changes expose the shortcomings of duration.

- Favoring high-convexity bonds: Longer-term or lower-coupon bonds are generally more desirable, offering better protection and benefits.

Positive Vs Negative Convexity

Bonds typically exhibit positive convexity, meaning that as yields change by a given amount, the magnitude of price increases exceeds that of price decreases due to the upward-sloping relationship between price and yield. Negative convexity works in reverse, where prices increase by a smaller amount as yields decline and by a larger amount as yields rise, offering less protection to investors.

This occurs in bonds with embedded options, such as callable bonds or mortgage-backed securities (MBS), where the issuer can only act in the best interest of the holder when it is favorable to them.

1. Callable Bonds

Callable bonds allow issuers to call, or redeem, bonds early, usually when interest rates are declining. This limits potential gains because, as yields decline, the likelihood of being called rises, resulting in a flat price curve and negative convexity. Additionally, investors are exposed to reinvestment risk at lower interest rates, making these bonds less desirable in a declining interest rate environment.

2. Mortgage-Backed Securities

Mortgage-backed securities combine multiple home loans into one security. When interest rates decline, homeowners refinance their mortgages, which is equivalent to a call option. Prepayments accelerate, shortening the life of the bond and causing negative convexity, where prices stagnate despite declining yields. On the other hand, in a rising interest rate environment, prepayment slows, lengthening the life of the bond and increasing losses due to extension risk.

Bond Convexity Vs Duration

Duration provides a straightforward, straight-line approach to approximating what might happen to a bond’s price when interest rates change. It’s a quick method for rudimentary risk analysis. Convexity builds upon that concept by examining the curve in that relationship: the non-linear aspect of how changes in duration itself relate to yields. Thus, while duration assumes a straight line, convexity illustrates the asymmetry: greater returns for a given decline in rates, smaller losses for a given increase.

| Aspect | Duration | Convexity |

| Measure | It is the first derivative of price with respect to yield changes. | It is the second derivative, showing how duration changes with yields. |

| Assumption | It assumes a straight-line relationship between price and yield. | It captures the non-linear, curved shape of the price-yield curve. |

| Strength | It provides quick, easy calculations for minor rate moves. | It improves precision for larger rate changes and asymmetry. |

| Usage | It works well for basic immunisation and screening. | It enhances portfolio hedging in uncertain markets. |

How Investors Can Use Convexity In Bond Selection?

Investors rely on bond convexity to identify bonds that provide better protection against interest rate risk than what a duration versus convexity analysis can offer. They focus on bonds with high convexity to maximize gains during periods of declining yields and minimize losses during periods of rising yields. This convexity is particularly valuable when evaluating portfolios for robustness.

1. Long Term Bonds

Bonds with longer maturities are likely to have higher convexity because of their longer cash flow exposure, making them ideal for maximizing gains from convexity. These bonds provide extraordinary gains during periods of declining yields and minimize losses during periods of rising yields, making them attractive to investors with longer investment horizons who can afford to take moderate duration risk.

2. Government vs. Corporate Bonds

Government bonds are likely to have cleaner positive convexity without call features, providing a pure convexity impact. Corporate bonds, on the other hand, are likely to have lower convexity because of embedded options but can provide higher returns.

Conclusion

Mastering bond convexity reveals why duration alone falls short; it uncovers the bond price curvature that protects against volatile interest rate risk measures. By favouring high-convexity bonds like long-term options, investors secure amplified gains and reduced losses, building resilient portfolios amid uncertainty.

If you are ready to apply these insights, explore superior fixed-income choices on Grip Invest. Start selecting convexity-smart bonds today for smarter returns.

FAQs On Bond Convexity

1. What is Bond Convexity in Simple Terms?

Bond convexity’s meaning is the measure of the curvature of bond prices in response to interest rate changes. While duration measures the straight-line approximation, convexity measures the curvature, which helps us better estimate the actual price behavior in the real world.

2. Why is Convexity Important for Bonds?

Convexity is a good risk management tool as it takes into account the non-linear behavior of bonds in a volatile market. It has a magnifying effect on the return when yields fall and reduces the pain when yields rise, making it a desirable feature in bonds.

3. Do All Bonds Have Positive Convexity?

No, while it is a general practice for conventional bonds to have positive convexity, callable bonds and mortgage-backed securities have negative convexity, where the borrower takes advantage of low yields to refinance.

4. How Is Bond Convexity Different From Duration?

Duration estimates bond price changes using a straight-line assumption. Convexity adjusts this estimate by accounting for the curve in the price–yield relationship, making predictions more accurate, especially when interest rates move sharply.

5. Is Higher Convexity Always Better for Investors?

Not always. While higher convexity offers better protection during volatile interest rate movements, bonds with high convexity often come with lower yields or higher prices. Investors must balance convexity benefits with return expectations and investment horizons.

6. Does Convexity Matter in Stable Interest Rate Environments?

Convexity matters less when interest rates move only slightly. However, it becomes crucial during uncertain or volatile periods, where large yield changes can lead to significant pricing errors if investors rely only on duration.

References:

1. Investopedia, accessed from: https://www.investopedia.com/terms/c/convexity.asp

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001