Bullet Bonds Explained: Meaning, Benefits, And Risks For Investors

India’s corporate debt market runs on scale. In FY 2024–25, private placements of corporate debt listed on BSE and NSE totalled 1659 issues worth INR 9.87 lakh crore1. That is a reminder that bonds are not just a conservative corner of finance. They are one of the main ways companies raise serious money in India.

But when a company borrows through bonds, one question matters as much as the coupon. How will the money be repaid? Some bonds return principal in phases during the tenor. Others keep that repayment for the very end. That is where bond repayment structures start to matter.

Among these structures, bullet bonds stand out because they are simple in form but important in practice. The issuer pays interest through the life of the bond and returns the full principal on maturity, a format commonly seen in Indian debt issuances and redemption terms.

That is also why bullet bonds are so common in corporate debt markets. They ease near-term cash flow pressure for issuers, keep the structure straightforward, and push the main repayment obligation to maturity.

In this blog, let us see the bullet bond meaning, why they are widely used and understand what that means for investors.

What Are Bullet Bonds

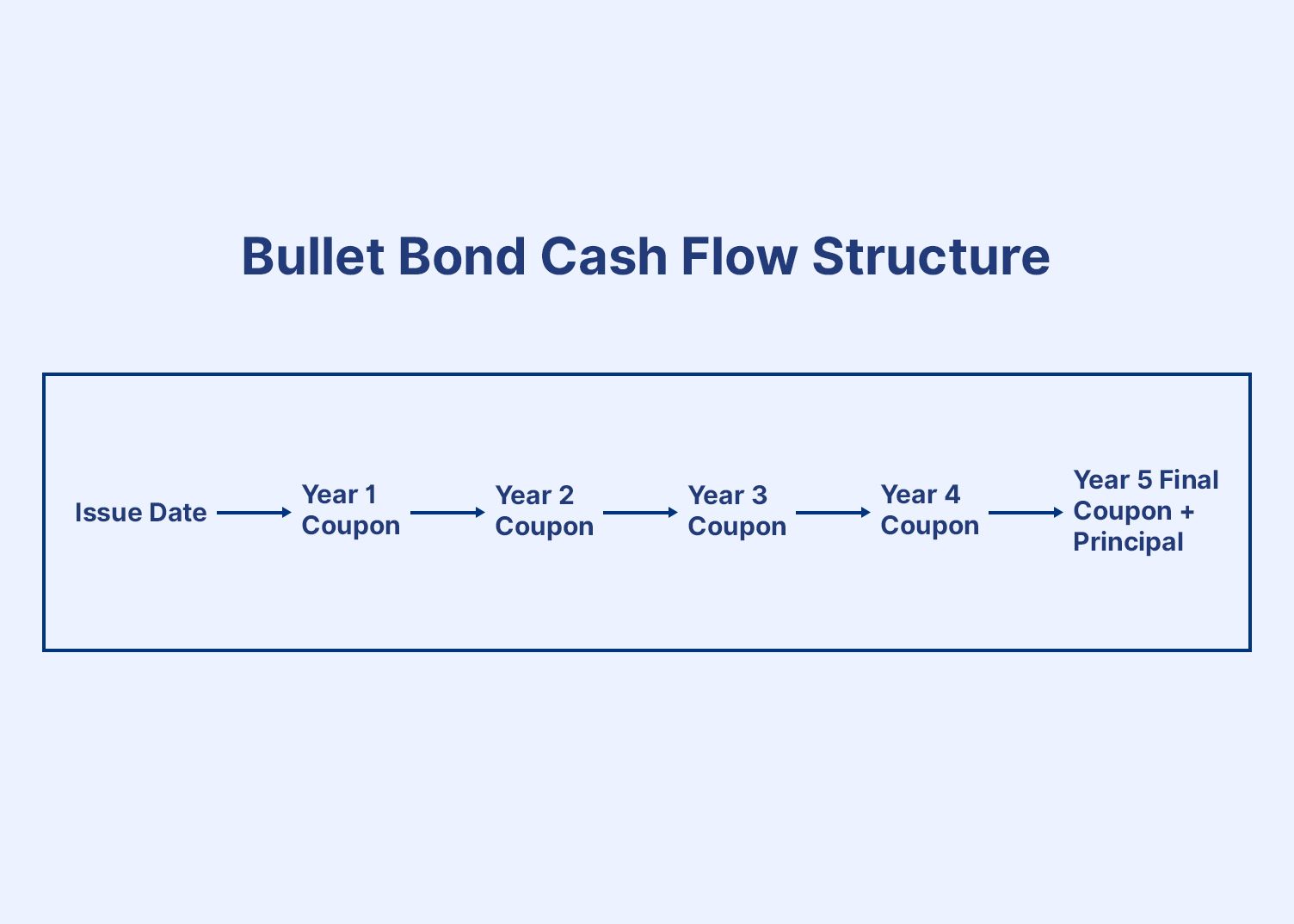

A bullet bond is a bond in which the entire principal is repaid in one lump sum on the maturity date. During the bond’s life, the issuer usually pays only the interest at fixed intervals, such as monthly, quarterly or annually. The original investment amount comes back only at the end.

For example, if you buy a 5-year bullet bond with a face value of INR 10,000, you receive the interest/coupon payment during those 5 years and the full INR 10000 is repaid on maturity.

Here are bullet bond features:

- Full principal is repaid only on the maturity date

- Interest is usually paid periodically during the tenure

- There is no staggered or instalment-based principal repayment

- The issuer faces a larger repayment obligation at maturity, which can raise refinancing risk

- The terms may still separately include or exclude call or put options, depending on the issue document

Since corporate bullet bonds follow a non-amortising structure, how are they different from amortising bonds?

Bullet Bonds vs Amortizing Bonds

Both are debt instruments, but the repayment pattern is different. As noted earlier, a bullet bond repays the entire principal in one go at maturity. While amortising bonds spreads it across the life of the instrument.

| Basis of comparison | Bullet bonds | Amortising bonds |

| Principal repayment | The full principal is repaid in one lump sum on maturity | The principal is repaid in parts over the bond’s tenure |

| Interest payment | Interest is usually paid periodically on the full outstanding principal until maturity | Interest is paid along with principal instalments, so the interest amount may reduce over time |

| Outstanding principal | Stays unchanged until the maturity date | Falls gradually as repayments are made |

| Issuer cash flow | Lower repayment pressure during the bond term, but a large payment is due at the end | Repayment burden is spread across the tenure |

| Investor cash flow | The investor gets the principal back only at maturity | The investor receives portions of the principal throughout the bond term |

| Refinancing risk | Higher, because the issuer must arrange the full principal at maturity | Lower, because the debt reduces steadily |

| Common use | Often seen in corporate debt markets and many plain vanilla bonds | Common in loans, mortgage-backed securities, and some structured debt instruments |

| Example | A company issues a 5-year bond of INR 1 lakh with 8% annual interest. The investor gets INR 8000 each year, and the full INR 1 lakh is repaid in the fifth year | A company issues a 5-year bond of INR 1 lakh and repays INR 20000 principal each year along with interest on the reducing balance |

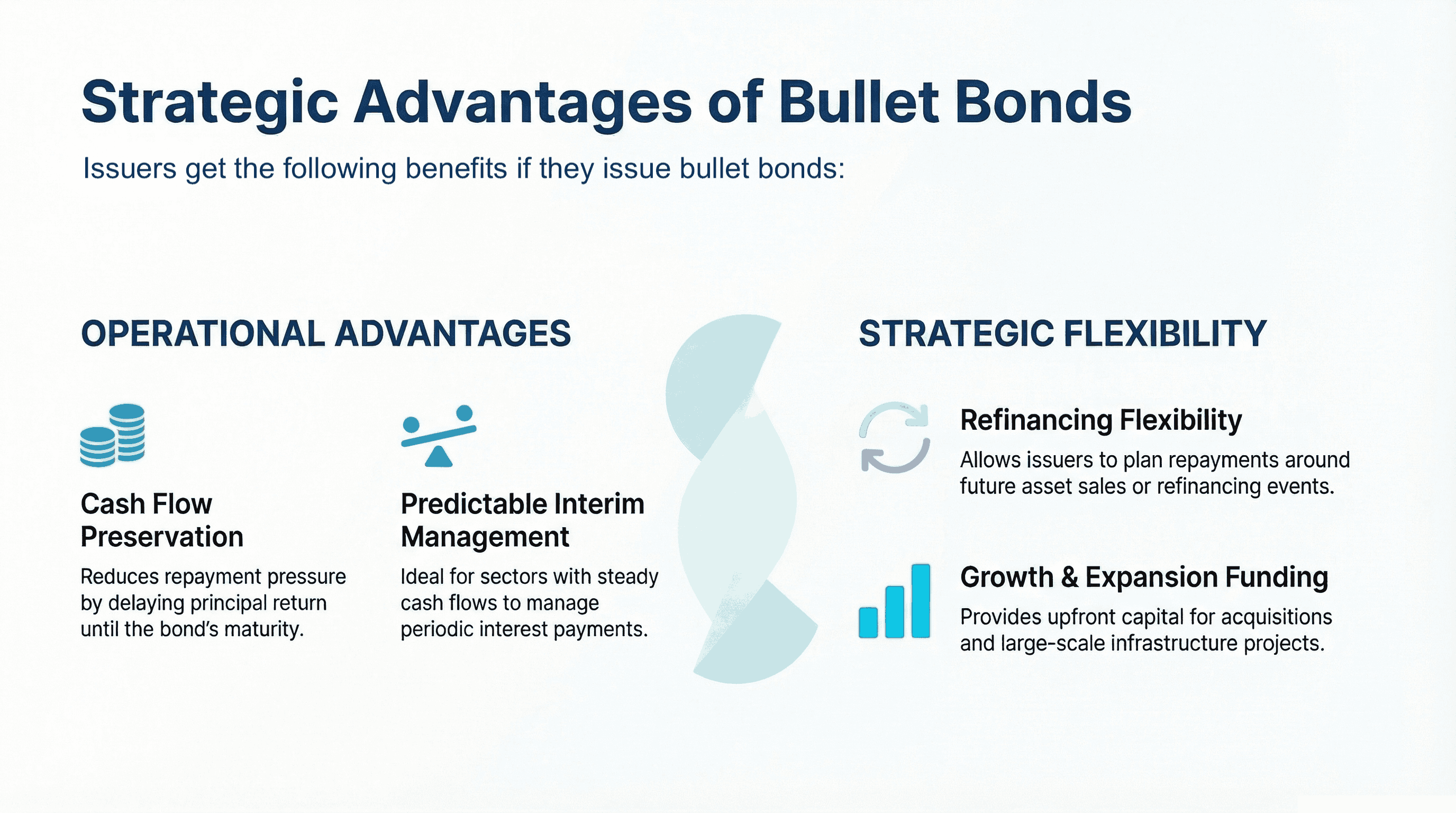

Why Companies Issue Bullet Bonds

Companies issue bullet repayment bonds mainly because the structure keeps principal repayment for the end of the tenor. In practice, that means the issuer services the coupon during the life of the bond and deals with the full repayment only at maturity.

1. Cash flow preservation: A bullet structure reduces repayment pressure during the bond’s life because the company does not have to return principal in stages. That can be useful when funds are being raised for expansion, acquisitions, or refinancing.

2. Refinancing flexibility: Many issuers use bullet bonds when they expect to refinance the liability later, sell assets, upstream cash from subsidiaries, or meet repayment through maturing business cash flows.

3. Businesses with predictable interim cash inflows: For companies with predictable operating cash flows, paying periodic interest may be manageable, while principal can be planned around a later refinancing, asset sale, or maturity event. That makes bullet bonds especially relevant in sectors such as infrastructure, real estate, and platform-style businesses that often raise larger sums upfront.

Who Should Invest In Bullet Bonds

Bullet bonds in India may suit investors who want a simple bond structure and are comfortable waiting until maturity to receive the full principal. Since the face value is repaid in one lump sum at the end, these bonds are often better suited to those who do not need regular return of capital during the tenure.

- Long-term investors: These bonds can work for investors who want steady interest income during the tenure and are willing to wait until maturity to receive the full principal. They may suit those investing for medium- to long-term goals.

- Institutional investors: Bullet bonds are often preferred by institutional investors such as mutual funds, insurers, pension funds, and corporate treasuries. These investors usually have larger pools of capital, defined investment horizons, and the ability to assess credit and maturity risk more closely.

Conclusion

Bullet bonds may look simple on paper, but they play a meaningful role in how companies raise and manage capital. By pushing the principal repayment to maturity, they give issuers breathing room during the bond’s life while placing a clear, time-bound obligation at the end. For investors, that same structure translates into predictable interest income through the tenure, with the principal returning in one go.

Like most debt instruments, the appeal of bullet bonds lies in how well they fit your needs. If you are comfortable with holding till maturity and understand the credit and refinancing risks involved, they can be a straightforward addition to a fixed income portfolio.

If you are exploring such opportunities, platforms like Grip Investcan help you access curated fixed income investments with transparency, making it easier to evaluate and invest with clarity.

FAQs

1. What is a bullet bond?

This debt instrument usually returns the full principal only on the maturity date. Interest is generally paid during the tenure, based on the coupon terms.

2. Are bullet bonds risky?

They can carry a fair amount of risk. The main concern is that the full principal is repaid only at maturity, so the investor depends heavily on the issuer’s ability to meet that final obligation.

3. How are bullet bonds different from amortizing bonds?

A bullet bond repays the full principal in one lump sum at maturity. An amortising bond repays the principal gradually over the life of the bond, usually in scheduled instalments.

Reference:

1. SEBI, accessed from: https://www.sebi.gov.in/sebi_data/commondocs/may-2025/SEBI%20Bulletin%20May%202025_AnnexureTables_p.pdf

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001